Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

That rejection email from the bank always lands with a thud. After pouring your heart and soul into building your business, getting a "no" for something as fundamental as a bank account feels like a personal slight, a major roadblock thrown in your path.

But here’s the truth: it’s almost never personal.

Most of the time, that rejection comes down to a simple mismatch. Your application, as you presented it, didn't perfectly align with the bank's incredibly strict risk and compliance rules. Think of it less as a final verdict and more as a signal that the bank’s compliance team needs a clearer, more compelling story about your business.

Why Your Bank Account Application Was Rejected

Let’s be honest, that formal email lands in your inbox and your heart sinks. You’ve done all the heavy lifting to set up your company, and now this hurdle stands between you and actually getting paid. It’s a deeply frustrating moment, but it’s one that countless entrepreneurs have faced and successfully navigated. The key is to understand what’s really happening behind the curtain.

A huge number of rejections boil down to failing to meet the basic compliance requirements for business. Banks aren't just vaults for your money; they're the gatekeepers of the financial system. They are legally mandated to perform exhaustive checks to prevent money laundering, terrorist financing, and other illegal activities. Your application isn't just a stack of papers—it's Exhibit A in their internal risk assessment.

Shifting from Frustration to a Plan

Let’s imagine a startup founder, we'll call her Chloe. She's just launched a promising e-commerce business based out of Hong Kong. She applies for a business account, feeling confident, only to receive a vague rejection email a week later. Her first reaction is pure panic. Did she fill out a form wrong? Is her entire business model flawed before it even begins?

It’s a completely natural reaction. But Chloe’s story doesn't end there. Instead of giving up, she reframes the situation. The rejection isn't a dead end; it's a signal that the bank’s risk team needs more information to get comfortable. She's just missing a few pieces of the puzzle.

Often, those missing pieces are surprisingly common:

- Incomplete or inconsistent paperwork: A tiny mistake, a missing document, or a name that doesn't match perfectly across forms is one of the fastest routes to a denial.

- A "high-risk" business model: If you're in an industry like cryptocurrency, international consulting, or even jewelry, you can expect the bank to put your application under a much stronger microscope.

- Issues with director residency: A director's nationality or a lack of tangible ties to Hong Kong can raise immediate red flags for compliance teams.

“A bank rejection is just feedback. It’s telling you that the story your application tells isn’t clear or compelling enough for the bank’s risk department. Your job is to revise that story with better evidence.”

Understanding the world from the bank’s perspective is the first step. They need a clear, verifiable, and low-risk picture of who you are and what you do. Our own guide, https://lionbusinessco.com/the-bank-onboarding-risk-playbook-2025/, goes into a lot more detail on how banks actually think about these factors.

But for now, here’s a quick summary of the most common reasons you might have run into trouble.

Common Rejection Reasons at a Glance

This table gives you a quick overview of the top reasons for rejection and a solid first step you can take for each one.

| Rejection Reason | What It Means for the Bank | Your First Step |

|---|---|---|

| Incomplete/Inconsistent Info | The application has missing documents or conflicting details, creating uncertainty. | Double-check every single document for accuracy and consistency before reapplying. |

| High-Risk Industry | Your business type (e.g., crypto, consulting) is known for higher financial crime risk. | Prepare a detailed business plan that clearly explains your operations and risk mitigation. |

| Director Residency Issues | Key directors lack a strong, verifiable connection to Hong Kong, raising a red flag. | Strengthen your application with proof of local ties, like a residential address or local clients. |

| Unclear Source of Funds | The bank can't verify where your initial capital or ongoing revenue will come from. | Provide clear, documented evidence of your funding sources (e.g., investor agreements, personal bank statements). |

Think of this table as your initial diagnostic tool. In the next sections, we’ll break down each of these issues in more detail and give you a clear, actionable path to get your next application over the line.

Solving the Incomplete Documentation Puzzle

Of all the reasons why your bank account application was rejected, missing or messy paperwork is easily the most common. The good news? It's also the most preventable. Don't think of it as just filling out forms; you're actually building a case for your business's legitimacy. You're the lawyer, and your documents are the evidence.

When a bank's compliance officer picks up your file, they're looking for a story that's clear, consistent, and easy to verify. A missing proof of address or a slightly different name on a director's ID creates a plot hole. It introduces doubt, and for a bank, doubt almost always leads to the safest choice: saying no.

Building Your Case with the Right Paperwork

To get past this hurdle, you need to hand them a file so complete that there's nothing left to question. In Hong Kong, banks are incredibly thorough, thanks to strict Know Your Customer (KYC) and Anti-Money Laundering (AML) rules. This means you need to bring more than just the bare minimum.

At its core, your submission must include:

- Business Registration Certificate: The official document that proves your company legally exists.

- Articles of Association: This shows the bank how your company is run, confirming its formal structure.

- Proof of Business Address: A recent utility bill or tenancy agreement is essential. It proves you have a physical base of operations.

- Director and Shareholder Identification: Crystal-clear copies of passports and proof of residential address for every key person involved.

This isn't just a simple checklist. It's the foundation of your business's story. Every single document has to be up-to-date, legible, and perfectly match the details on your application form. Even a tiny mismatch can raise a red flag.

Proving Your Business Is Real and Operational

Beyond the basics, the real challenge is demonstrating that your business is more than just a name on a piece of paper. This is where a surprising number of applications fail. According to industry insiders, a major reason for rejection in Hong Kong is the inability to show real proof of business activity, a particular challenge for new companies or owners living abroad. You can explore more about these common pitfalls and get a clearer picture of what banks are really looking for.

“Think of it like this: your Business Registration proves you exist, but invoices and contracts prove you operate. Without the latter, the bank sees a shell, not a living business.”

To make your case compelling, you need to show tangible proof of commercial activity. This is your opportunity to prove to the bank that your business is a genuine, operating entity.

Start gathering documents like:

- Signed Contracts or Agreements: These show you have real clients and genuine commercial commitments.

- Recent Invoices: Both sent to customers and received from suppliers, as this demonstrates active trade.

- Supplier Agreements: This provides evidence of your supply chain and operational setup.

- Website or Marketing Materials: Proof that you are actively in the market and promoting your business.

By carefully organising this evidence, your application transforms from a stack of forms into a convincing story about a legitimate business. Taking this proactive approach is the single best way to solve the documentation puzzle and secure that account approval.

Navigating High-Risk and Sensitive Industries

When you're trying to open a business bank account, it's crucial to realise that banks don't see all businesses in the same light. If your company operates in what's considered a 'high-risk' or sensitive industry, you're not just filling out forms; you're stepping onto a different playing field where the rules are much stricter. A big part of understanding why your bank account application was rejected is learning to see your business through the eyes of a bank's risk department.

Think of it like an insurer assessing a new client. A corner bakery has a predictable, straightforward business model—it’s a low-risk proposition. But a business dealing in cryptocurrency, international consulting, or precious jewels? That's a whole different story. The money trail can be complex and harder to follow, which immediately sets off alarm bells for a bank's compliance team, who are always on guard against potential money laundering.

Why Certain Industries Raise Red Flags

In Hong Kong, certain types of businesses are automatically flagged for a much deeper level of scrutiny. A primary reason for rejection is simply operating in a sector where the transactions are inherently difficult to verify. According to Hongda Service, a firm that helps businesses navigate Hong Kong's corporate banking maze, financial institutions are especially wary of companies involved in virtual assets, mining, jewellery, and even service-based sectors like consulting.

This isn't personal; it's purely a matter of risk management based on a few common factors:

- Difficulty Tracing Funds: Think about it. When a consultant receives a large payment, it’s for an intangible service. It's much harder to prove a legitimate transaction took place compared to, say, selling a shipping container full of widgets with a clear paper trail.

- Price Volatility: In industries like jewellery or crypto, asset values can swing dramatically. This makes it tough for compliance teams to properly assess and validate the value of transactions.

- Cash Intensity: Any business that deals heavily in physical cash is an instant red flag. The source of cash is notoriously difficult to trace, making it a classic vehicle for money laundering.

Turning a High-Risk Label into an Asset

Just because you’re in a sensitive industry doesn’t mean a bank account is impossible to get. Not at all. It just means you need to do your homework and show up exceptionally well-prepared. Your job is to get ahead of the bank’s concerns and prove that your business is not only legitimate but also run with an airtight, professional approach to compliance.

The best way to do this is with a rock-solid business plan. And I don't just mean a document that talks about your mission and vision. It needs to spell out your internal compliance controls in painstaking detail.

A business in a high-risk industry without a documented compliance plan is just a liability to a bank. But a business that can demonstrate robust anti-money laundering checks and transparent transaction processes becomes a much more attractive, low-risk client.

I know of a jewellery trader whose application was initially rejected. They went back to the drawing board and returned to the bank with a detailed operational plan. It wasn't just fluff; it included mandatory third-party appraisals for all high-value items and a strict policy of using traceable digital payments instead of cash. By anticipating the bank's fears and presenting a solution, they turned a major obstacle into a powerful demonstration of their professionalism and got the account.

How Director Nationality and Residency Affect Your Application

It’s easy to think banks are just vetting your business, but they’re digging much deeper—they're scrutinising the people behind it. This is a crucial point that catches so many entrepreneurs off guard. If your application was turned down, it might have less to do with your business plan and more to do with who your directors and shareholders are, and where they come from.

Think of it from the bank's perspective. A compliance officer has a global risk map on their screen, and certain countries are glowing red. These are places flagged for international sanctions, political instability, or a history of financial crime. If a director or a major shareholder has strong ties to one of these zones, it’s an immediate red flag. It's nothing personal; it’s just a non-negotiable part of their duty to combat illegal money flows.

The Geography of Risk

One of the biggest hurdles in Hong Kong is the nationality or residency of a company’s directors. Banks are incredibly cautious about individuals from high-risk jurisdictions. As the corporate services provider BBCIncorp points out, applications from business owners with links to restricted countries are almost always put under a microscope or rejected outright. You can discover more insights on why banks reject applications for these very reasons.

This creates a real headache for global entrepreneurs. Your business could be perfectly legitimate, but if your personal geography trips a compliance wire, your application is in trouble before you even start.

“A bank’s first question is always, ‘Can we trust the people behind this business?’ If a director’s background links to a high-risk jurisdiction, the answer starts leaning towards ‘no’ unless you provide overwhelming evidence to the contrary.”

Proactive Solutions to Geographical Hurdles

So, what’s the fix if this is why your bank account application was rejected? Don’t throw in the towel. The key is to get ahead of the bank’s concerns and build a much more convincing case.

Here are two strategies that actually work:

- Appoint a Hong Kong Resident Director: This is a powerful move. Bringing someone on board who has solid local ties can dramatically lower the perceived risk. It shows you’re serious about local governance and gives the bank a resident point of contact they can trust.

- Provide Extensive Background Documentation: Don't wait for them to come asking. Be proactive. Submit detailed documents that explain exactly what your business does and directly address any potential risks they might associate with your nationality.

Getting a handle on the specific Hong Kong bank account requirements for non-residents is your first and most important step. It might also be helpful to review some guidance on opening a non-resident bank account in Dubai to see how other major financial hubs handle this exact issue. By seeing the world through the bank's eyes, you can put together an application that puts their biggest fears to rest.

Your Action Plan for Getting Approved Next Time

Getting a rejection letter from a bank is frustrating, but it’s not the end of the road. Far from it. Think of it as valuable, if blunt, feedback—the bank is showing you exactly where they see a risk in your application. Your job now is to figure out that risk and address it head-on.

The first step isn't to immediately fire off another application to a different bank. Pause and be strategic. It's worth making a polite, professional call or sending an email to the bank that rejected you. While strict privacy policies mean they won't give you a play-by-play, you might get a general hint about why your bank account application was rejected. Sometimes, a small clue is all you need.

Strengthening Your Reapplication Strategy

Armed with some insight (or even just a good guess), it's time to build a much stronger case. This isn't about just tidying up the same documents; it's about a complete upgrade to your application package.

- Beef Up Your Documentation: If weak paperwork was the culprit, go overboard. Dig up recently signed client contracts, fresh invoices, or new supplier agreements. The goal is to provide undeniable proof of active, legitimate business operations.

- Clarify Your Business Model: If you’re in what’s considered a "high-risk" industry, you need to tackle that perception directly. Revise your business plan to spell out your compliance protocols, especially your anti-money laundering (AML) controls. Show them you’re not just aware of the risks—you're actively managing them.

- Address Director-Related Concerns: Was a director's nationality or residency the issue? You might need to demonstrate a stronger connection to Hong Kong. Proactively providing extra documentation that explains any links to high-risk countries can also help neutralise this as a red flag.

Sometimes, a rejection points to a fundamental mismatch between your company’s structure and the bank's expectations. For a deep dive into what banks are looking for, our Hong Kong banking checklist helps SMEs avoid freezes and rejections, ensuring your setup is solid from the get-go.

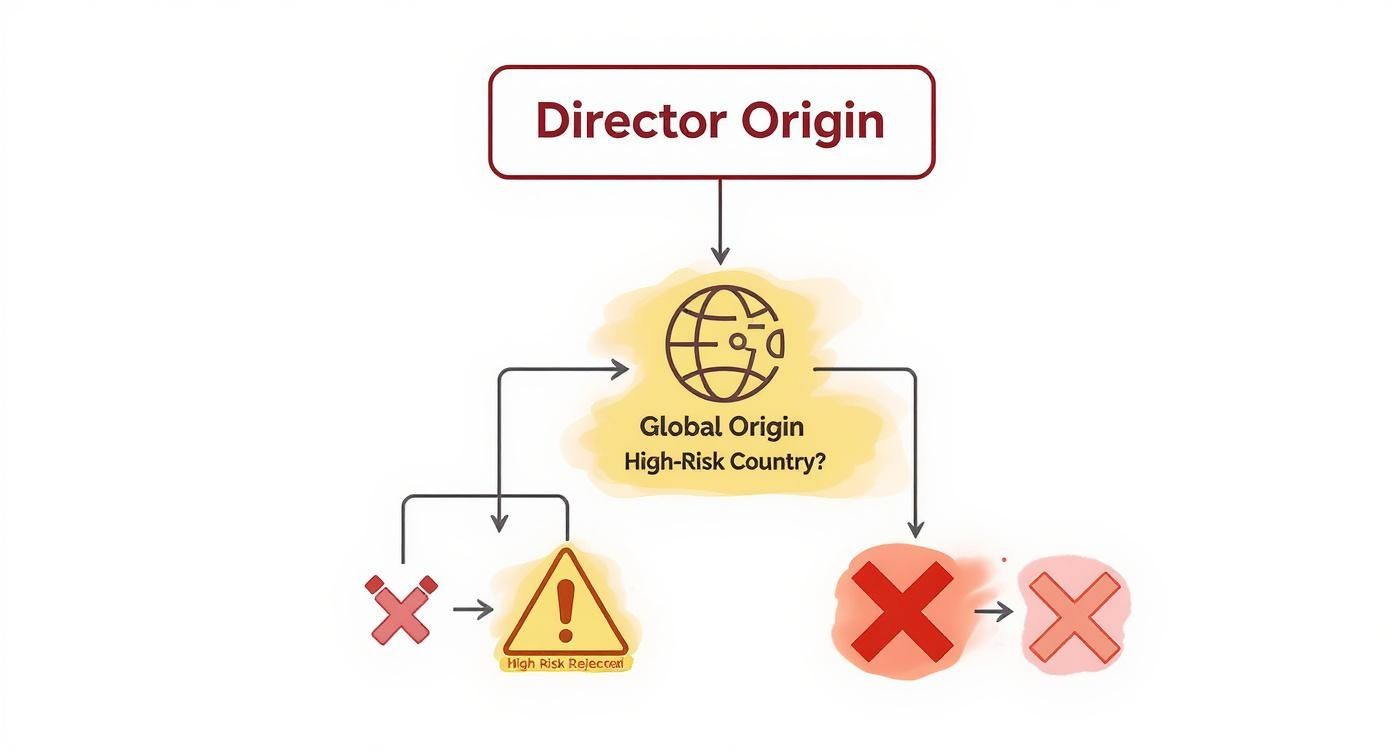

This decision tree shows just how quickly a single factor, like a director's country of origin, can trigger a rejection within a bank's automated risk assessment.

It’s a stark reminder of how black-and-white these internal risk models can be, often filtering out perfectly good businesses based on a few predefined rules.

Exploring Powerful Alternatives

What if reapplying to the same type of traditional bank feels like banging your head against a wall? It's probably time to look beyond the usual suspects. The financial world today is much bigger than just the household names on every street corner.

A rejection from a traditional bank doesn't mean your business is unbankable. It often just means your business doesn't fit their decades-old risk profile. Modern alternatives were built for exactly this reason.

Many modern financial service providers have built their entire business model on serving the clients that traditional banks turn away. This is where you should look next.

After a rejection, choosing between a familiar high-street bank and a newer digital player can be a crucial decision. This table breaks down the key differences to help you find the right home for your business finances.

Table: Traditional Banks vs Digital Alternatives

| Feature | Traditional Banks (HSBC, Standard Chartered) | Digital Banks & Fintech Platforms |

|---|---|---|

| Onboarding Process | Often requires in-person visits and extensive paperwork. Slower approval times. | Fully online, often faster and more streamlined. Less paper-intensive. |

| Risk Appetite | Generally conservative. Wary of non-resident directors, complex structures, and certain industries. | More flexible and tech-driven risk assessment. Often more welcoming to international and online businesses. |

| Service Model | Branch-based services, relationship managers, and established but sometimes clunky online portals. | App-based, digital-first experience. Customer support is typically online (chat, email). |

| Best For | Established, locally-rooted businesses with straightforward ownership and trading patterns. | Start-ups, international SMEs, e-commerce businesses, and companies with non-resident directors. |

Ultimately, the best choice depends on why you were rejected in the first place. If it was a simple documentation issue, a traditional bank might still work. But if it was a fundamental mismatch with their risk profile, a digital platform is almost certainly your better bet.

Your Top Questions About Bank Rejections Answered

Getting turned down by a bank can feel like hitting a brick wall. It’s frustrating, and it leaves you with a lot of questions. Let's tackle some of the most common concerns entrepreneurs have and get you on the right path.

How Long Should I Wait Before Reapplying to the Same Bank?

While there’s no official countdown timer, a good rule of thumb is to wait at least three to six months.

Simply trying again a week later with the same paperwork is a fast track to another rejection. You need to give yourself time to genuinely improve your application. Think of the first rejection as a test run where the bank gave you some unspoken feedback.

Use those months productively. If your documentation was a bit thin, get more client contracts signed or build up a stronger invoicing history. If your business model seemed vague, refine your plan to directly address the bank’s likely concerns. Reapplying with a much stronger, more detailed application shows you’re serious and have fixed the initial problems, which massively boosts your odds of success.

Will a Rejection from One Bank Hurt My Chances with Another?

This is a big worry for many, but the answer isn't a simple yes or no. Banks in Hong Kong don't share a secret blacklist of rejected applicants. However, they all play by the same rulebook when it comes to anti-money laundering (AML) and compliance regulations.

This means the core issue that got you a "no" from Bank A will almost certainly raise a red flag at Bank B, C, and D. The rejection itself doesn't tarnish your name, but the reason for it absolutely follows you. Just hopping to another bank without fixing the problem is like trying to use a broken key on a different door—the result will be the same.

Treat that first rejection as a free diagnostic report. It’s a huge clue that tells you exactly where your application is weak. Your top priority should be to find that weakness and fix it before you even think about approaching another bank.

Can a Professional Service Help with My Bank Application?

Absolutely. For international founders, this is often the single most effective step you can take. A good corporate service provider in Hong Kong lives and breathes the local banking system. They understand the specific requirements—and often the unwritten rules—of different banks.

Here’s how they can make a difference:

- Polishing Your Application: They know precisely what documents are needed and how to present your business in the clearest, most professional light.

- Spotting Trouble Early: They can identify potential red flags in your profile, like a director’s residency or a high-risk business activity, and help you proactively address them before the bank even asks.

- Strategic Matchmaking: They have working relationships with banks and know which ones are more open to a business like yours, saving you months of wasted effort on applications that were never going to fly.

It’s an investment, but it often pays for itself by helping you avoid costly delays and lost opportunities.

Should I Just Use a Personal Account for My Business Instead?

This question usually comes from a place of pure frustration, but the answer is a hard and fast no. Using your personal account for business is a critical error with serious consequences.

For starters, it's a clear violation of the bank's terms and conditions. It’s not a matter of if they find out, but when. And when they do, they can freeze or shut down your account without any warning, trapping your funds and bringing your business to a sudden halt.

Beyond that, mixing personal and business funds is a legal and accounting disaster. It makes bookkeeping a nightmare, destroys the liability protection your company structure is supposed to offer, and looks incredibly unprofessional to clients, suppliers, and partners. To build a secure and legitimate business, a proper business account is non-negotiable.

Conclusion

Navigating the world of international banking can be complex, but you don't have to do it alone. At Lion Business Consultancy Limited, we act as your private financial manager, crafting secure banking setups that protect your business and support your global growth. If you’re ready for a strategic partner who can guarantee results, explore our private advisory services.