Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

Opening a bank account in a top-tier financial centre like Hong Kong comes down to three things: proving who you are, verifying your business is legitimate, and showing the bank exactly why you need the account. Think of it as telling a clear, compelling story with documents. This usually means gathering your passport, proof of address, and a full suite of business documents, like your certificate of incorporation and a solid business plan. Getting it right from the start is crucial, as banks here have very strict compliance standards.

Why Hong Kong Is a Top Choice for International Banking

When entrepreneurs and small business owners start thinking globally, the conversation inevitably lands on banking. It’s not just a question of how to open an account as a non-resident, but where. For decades, Hong Kong has been a go-to answer, and for good reason. It’s not just a city of dazzling skyscrapers; it’s a financial stronghold built on stability, security, and a savvy understanding of international trade.

Imagine Hong Kong’s banking system as the ideal command centre for a global business. It sits perfectly at the crossroads of East and West, making it a natural hub for companies working with suppliers in mainland China or serving clients across Asia. This strategic location is powered by a truly world-class financial infrastructure.

The Bedrock of Stability and Security

One of the biggest draws for entrepreneurs is Hong Kong's rock-solid stability. The Hong Kong Dollar (HKD) is pegged to the US Dollar, creating a predictable currency environment. For international SMEs, this is a massive relief, as it shields your business from the wild swings in exchange rates that can eat into profits.

This isn’t just on paper, either. Hong Kong's banking sector is incredibly resilient, backed by tough regulatory oversight. Its banks maintain liquidity buffers that are well above global standards. In the first quarter of 2025, the Liquidity Coverage Ratio (LCR) for major banks hit a near-record high of 182.5 percent, proving they can easily handle their short-term obligations. This strong framework makes Hong Kong a safe harbour for your company’s funds.

Sophisticated Tools for Global Trade

Beyond just being safe, Hong Kong banks offer a suite of sophisticated tools built for international business. If you're running an e-commerce company sourcing products from several Asian countries, this is where it gets really interesting.

Here’s what that means in the real world:

- True Multi-Currency Accounts: These are more than just accounts that can hold foreign cash. They’re dynamic platforms where you can get paid in USD, pay your suppliers in RMB, and keep profits in EUR—all from one place. It cuts down on conversion fees and simplifies your bookkeeping.

- Advanced Trade Finance Solutions: Need a letter of credit for a new supplier in Vietnam? Hong Kong banks have dedicated departments to handle these complex trade instruments, boosting your credibility and securing your supply chain.

- Seamless International Transfers: With direct access to global payment networks, you can send money across borders quickly and reliably. This means your partners and staff get paid on time, every time.

These aren't just nice-to-haves; they are real strategic advantages that can make your operations smoother and more profitable. We’ve covered many of these in our guide on the benefits of a Hong Kong bank account for international businesses.

To help you get a clearer picture, I've put together a quick summary of the essential requirements. Think of this as your initial checklist before you even approach a bank.

Quick Overview of Key Requirements for Non-Residents

| Requirement | Description | Why It's Important |

|---|---|---|

| Valid Passport | A certified copy of the passport for all directors, shareholders, and signatories. | The bank's first step in verifying your identity (KYC – Know Your Customer). |

| Proof of Address | A recent utility bill or bank statement (within the last 3 months) for all key individuals. | Confirms your residential address and is another critical part of KYC compliance. |

| Business Registration | The Certificate of Incorporation and Business Registration Certificate for your company. | Proves your company is a legally registered entity. |

| Detailed Business Plan | A comprehensive plan outlining your business model, target markets, and financial projections. | Shows the bank you have a viable business and helps them understand your transaction patterns. |

| Proof of Business | Supporting documents like contracts, invoices, or supplier agreements. | Provides concrete evidence of your business activities and adds credibility to your application. |

Getting these documents in order is the most important part of the process. A well-prepared application shows the bank you're serious and makes their decision much easier.

For any international entrepreneur, the goal is to reduce friction. A Hong Kong bank account does just that. It removes the operational hurdles of cross-border payments, currency management, and trade finance, letting you focus on what you do best—growing your business.

At the end of the day, choosing Hong Kong is about setting your business up for the future. It gives you a stable, secure, and incredibly efficient banking foundation that not only supports your current goals but also paves the way for future expansion. The upfront work of getting your documents together is a small price to pay for the operational freedom and peace of mind you get in return.

Selecting the Right Bank for Your Business Needs

Choosing a bank as a non-resident isn't just about finding a place to park your cash. It's about finding a genuine partner who gets the unique hurdles of running an international business. It’s tempting to just go with the biggest names you recognise, but the best choice really boils down to your specific business model, how you move money, and where you plan to grow.

Think of it like choosing a vehicle for a cross-country road trip. A big, established bank like HSBC or Standard Chartered is like a heavy-duty lorry—incredibly reliable, powerful, and built for heavy lifting like complex trade finance. On the other hand, a nimble digital bank is more like a sleek electric car—fast, efficient for daily errands, and packed with modern tech, but maybe not what you’d use to haul industrial equipment. Your job is to pick the right vehicle for your journey.

Traditional Giants vs. Digital Challengers

The major international banks in Hong Kong have been handling non-resident clients for decades. They offer a huge menu of services, from multi-currency accounts to sophisticated lending and investment products. That established reputation can be a massive asset, especially when you're dealing with large, old-school suppliers or clients who are impressed by a well-known banking partner.

But that legacy often comes with a side of bureaucracy. Opening an account can be a slower, more paper-heavy process, and their online platforms can feel a bit dated. In contrast, digital banks and modern fintechs usually offer a much smoother user experience, faster onboarding, and lower fees for standard international transfers. The trade-off? They might lack the specialised trade finance tools or the dedicated relationship manager that a more complex business really needs.

A common mistake I see is entrepreneurs prioritizing a familiar brand name over a functional fit. The best bank for your business is the one whose strengths line up perfectly with your day-to-day needs, not just the one with the biggest logo.

A Real-World Example of Strategic Bank Selection

I once worked with a European e-commerce company that was sourcing artisanal goods from lots of small suppliers across Southeast Asia. They started out with a major bank but were getting crushed by high wire transfer fees and painfully slow processing times on dozens of small, regular payments. It was constantly holding up their supply chain.

We moved them to a smaller bank that specialised in SME trade. This new bank had a great online platform built for batch payments and offered much more competitive foreign exchange rates. The difference was night and day. They saved over £15,000 in fees in the first year, but the real win was that their payment processing time shrank from days to just hours. This simple switch made their suppliers happier and their whole operation run smoother.

Key Factors to Evaluate in a Bank

When you’re trying to figure out how to open a bank account as a non-resident, your checklist needs to go beyond the basics. Here’s what you should be focusing on:

- Experience with Non-Resident Clients: Don't be shy. Ask them directly how they support international businesses. Do they have dedicated teams? Do they understand the regulations in your home country? Hesitation is a red flag.

- International Transfer Fees and FX Rates: Look past the advertised transfer fee. The real cost is often hidden in the foreign exchange margins. Even a 0.5% difference in the exchange rate can cost you thousands on larger transactions.

- Online Banking Platform Usability: Your banking portal is your daily command centre. Is it actually easy to use? Does it support batch payments, multi-user access with different permissions, and clear reporting? A clunky interface will become a major headache.

- Account Maintenance and Minimum Balance Fees: Get a clear picture of what it costs to simply keep the account open. Many banks will waive monthly fees if you maintain a certain balance, but these requirements can be quite high, sometimes over HK$50,000.

For a detailed breakdown of your options, our regularly updated list of banks in Hong Kong is a fantastic place to start your research. It's also worth remembering that your banking choice is part of a bigger picture; for a comprehensive expat relocation guide, this is an excellent resource.

Ultimately, your bank should make your business run better, not hold it back. Take the time to interview potential banks, ask the tough questions, and choose the one that will truly help you grow internationally.

Getting Your Paperwork in Order: A Complete Checklist

The success of your bank account application hinges on your documents. Seriously. One missing piece of paper or a tiny mismatch isn't just a small snag—it can halt the entire process for weeks and send you right back to square one. Think of this checklist as your game plan for getting it right the first time.

This isn't just about collecting papers. It's about understanding why the bank is asking for them. Hong Kong banks are bound by strict Anti-Money Laundering (AML) and Know-Your-Customer (KYC) rules. Every document you hand over helps them piece together a clear picture of you and your business, proving that you’re legitimate and above board.

The Personal Identity Essentials

First things first, let's nail down the absolute must-haves for every director, shareholder, and account signatory. These documents confirm who you are, with no room for doubt.

You'll need to prepare:

- A Valid Passport: A certified true copy is required. This is the cornerstone of your personal identification.

- Proof of Residential Address: This is a classic stumbling block. Banks need a recent utility bill or a personal bank statement (from the last three months) that shows your full name and current home address, matching your application form exactly.

Even a small difference can derail everything. I once saw an entrepreneur get rejected because the address on his utility bill had his middle initial, but his application form didn't. The bank's compliance software flagged it instantly. We had to get a new document issued, which set him back nearly a month. It sounds trivial, but in the world of banking compliance, details are everything.

The Business Verification Documents

With your personal identities confirmed, the bank will shift its focus to your company. They need to see concrete proof that it's a legally registered and active entity.

Your core business document package must include:

- Certificate of Incorporation and Business Registration Certificate: These are the official papers that prove your company legally exists.

- Register of Directors and Shareholders: This lays out the ownership and management structure, which is a critical piece of the KYC puzzle for the bank.

- Memorandum and Articles of Association: This document defines the rules your company operates by.

The whole point of this paperwork is to create a crystal-clear trail from the individual owners to the legal business. Banks need to see an unbroken line of ownership and control to meet their regulatory duties. Any grey areas are an immediate red flag.

Proving Your Business Is Real and Active

This is perhaps the most critical part of your application, especially when you're figuring out how to open a bank account as a non-resident. The bank needs to see tangible proof that your business is a living, breathing operation, not just a name on a piece of paper. This is where you tell your business's story through documents.

You'll need to provide what the industry calls "proof of business activity." This can be a mix of documents, including things like:

- Existing Business Contracts: Signed agreements with your clients.

- Invoices: A few examples of invoices you've sent out or paid.

- Supplier Agreements: Contracts you have in place with key suppliers.

- A Detailed Business Plan: This needs to clearly outline your business model, who you sell to, how you make money, and your expected transaction volumes. Be very specific about why a Hong Kong bank account is necessary for your operations.

Putting all this together can feel like a lot of work, but every document you add gives your application more weight. For a complete rundown, our guide on Hong Kong bank account requirements for non-residents goes into even more detail. By organising this paperwork perfectly, you’re doing more than just filling out a form—you’re starting a new banking relationship built on trust and transparency from day one.

Diving into the Bank Account Application

Alright, you've got your documents sorted and perfectly organised. Now for the main event: the application itself. Think of this less as filling out forms and more as starting a crucial business relationship. Nailing this part is absolutely vital when you're trying to open a bank account as a non-resident.

The path from submitting your application to getting your account activated has a few distinct stages. It typically kicks off with securing an appointment, moves on to the all-important bank interview, and finishes with the waiting period. Each step demands a slightly different strategy, whether you're on the ground in Hong Kong or trying to manage things from afar.

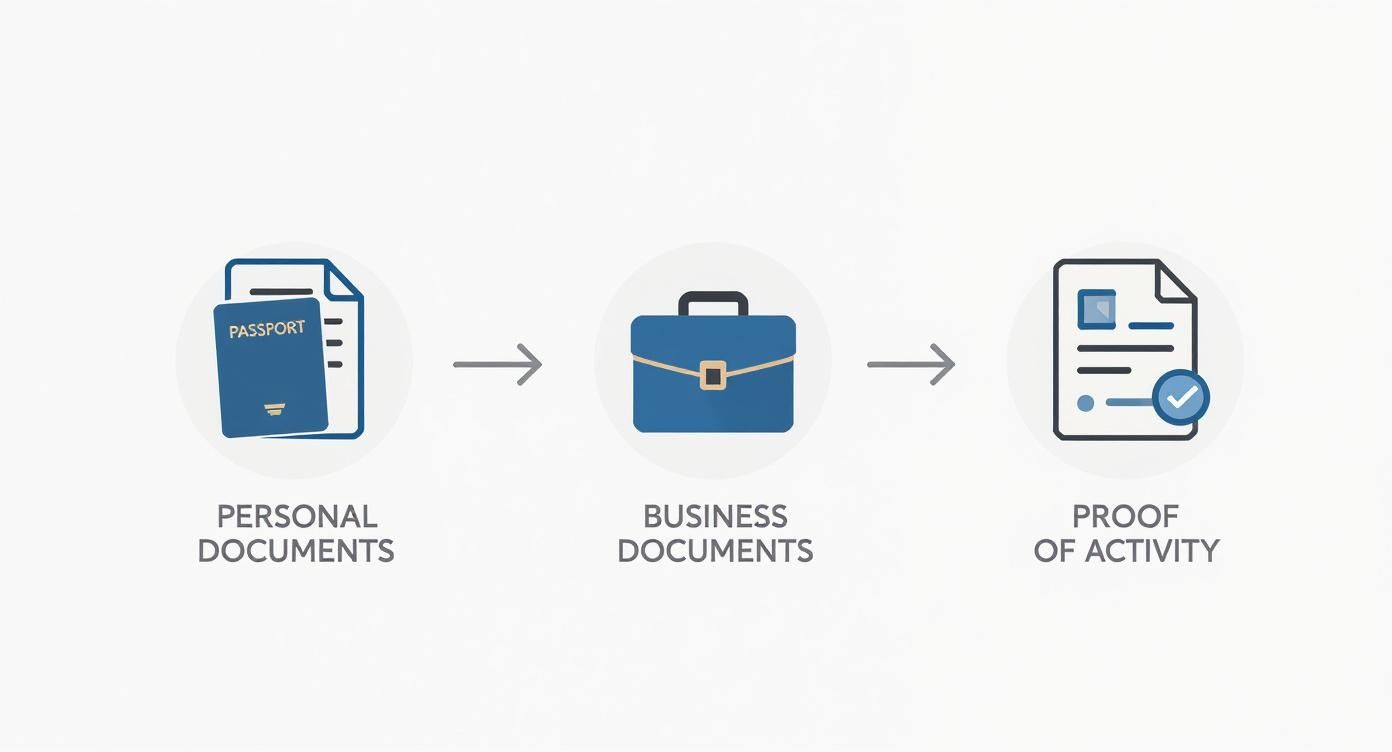

This visual breaks down how all your paperwork fits together, showing how your personal, business, and activity proofs create a complete picture for the bank.

As you can see, a solid application rests on these three pillars of proof. Each one is designed to verify a different, essential part of your business's legitimacy.

In-Person vs. Remote Applications

Let's get straight to the point: showing up in person is almost always the best move. In today's compliance-driven world, most big banks in Hong Kong don't just prefer a face-to-face meeting with at least one company director—they often insist on it. It’s the simplest way for them to meet their strict KYC (Know Your Customer) obligations.

But an in-person visit does more than just tick a box. It puts a human face to your application. You're no longer just a name on a form; you're a real entrepreneur. This is your chance to build a bit of rapport with the bank manager, explain the finer points of your business, and clear up any questions immediately. That personal connection can be the deciding factor.

While some digital-only banks might offer remote onboarding, the process is usually tougher and faces far more scrutiny. If your business has any complexity at all, booking a trip to Hong Kong will dramatically increase your odds of success.

Mastering the Bank Interview

The bank meeting isn't an interrogation; it's a conversation between professionals. The manager’s job is to understand your business and see if it fits within the bank's risk framework. They need to walk away feeling confident that your operations are legitimate, transparent, and predictable.

To get ready, be prepared to talk through the following with confidence:

- Your Business Model: Be crystal clear about what your company does, who your customers are, and how you generate revenue. Ditch the industry jargon and keep it simple.

- Transaction Volumes and Patterns: Provide realistic projections for your monthly turnover. Are you expecting a few large payments or lots of small ones? Critically, where is the money coming from and where is it going?

- Your Reason for Banking in Hong Kong: This is a huge one. You need a solid business reason. Maybe you need to pay suppliers in Asia, collect payments from regional clients, or use the city as a base for international trade.

I once worked with a client running a software development agency. Instead of just saying "we build software," he painted a clear picture for the manager: "We sign a contract with a client in Europe, get a 50% upfront payment, use that to pay our developers in Southeast Asia, and then collect the final payment when the project is delivered." This kind of specific, story-driven explanation gave the bank complete clarity and confidence.

Your goal in the interview is to tell a clear, consistent, and logical story about your company's financial life. If the bank manager can easily understand your business and explain it to their own compliance team, you're already halfway there.

Setting Realistic Timelines

Once you've had a successful meeting, the waiting game starts. Don't expect a decision on the spot. The application now goes to the bank's internal compliance and due diligence teams for a thorough review. For a straightforward case with flawless paperwork, you can often hear back within 2 to 4 weeks.

However, if your business is in a sector they consider higher-risk, or if they come back asking for more information, the process can easily stretch to 2-3 months. Patience is a virtue here. It's fine to follow up politely after a few weeks, but avoid calling them every day. A well-prepared application and a confident interview are your best bets for getting approved as quickly as possible so you can focus on what really matters—running your business.

Common Application Pitfalls and How to Sidestep Them

Even the most organised entrepreneurs can hit a snag during the bank application process. I’ve seen it time and time again—a vague business description, a slightly mismatched address, or an unclear reason for needing the account can grind everything to a halt or lead to an outright rejection.

Think of your application as your first conversation with the bank's compliance team. If your story is confusing or your documents create more questions than they answer, they’ll likely move on to the next file in the pile. Your goal is to make their decision to approve you an easy one.

The Vague Business Plan Trap

One of the most common mistakes I see is a business plan that’s either too generic or sounds wildly ambitious. Bankers are pragmatic people. They need to see a clear, grounded strategy, not a collection of buzzwords. A plan that just says you'll "engage in global e-commerce" is an instant red flag because it tells them nothing concrete about your cash flow.

Instead, get specific. Really specific. For instance, a strong application might detail: "We sell custom-printed apparel, which we source from a supplier in Shenzhen. We'll be receiving payments in USD from customers in North America and Europe through our online store, and we need a Hong Kong account to pay our supplier in RMB." This gives the bank a clear picture of your transaction patterns, which is exactly what they need for their risk assessment.

Just as important is tying this into why you need a Hong Kong account specifically. This justification needs to be a core part of your narrative.

- Weak Justification: "We need a Hong Kong account for international business."

- Strong Justification: "Our main supplier is based in Hong Kong. Having a local HKD account will cut our wire transfer fees by an estimated 15% and reduce payment settlement times from three days down to one."

Inconsistent Information Across Your Documents

This is a classic one that trips up so many people. The name on your passport, the address on your proof of address, and the details on the application form must be identical. A tiny variation, like using "St." on one document and "Street" on another, can get flagged by automated systems and stall your application indefinitely.

Before submitting a single page, lay all your documents out, side-by-side, and check them with a fine-toothed comb. Consistency demonstrates professionalism and attention to detail, building trust with the bank right from the start. It shows them you're an organised and reliable person to do business with.

The three pillars of a successful non-resident bank account application are clarity, consistency, and compliance. Your business plan must be crystal clear, your documents perfectly consistent, and your entire application needs to show you're serious about meeting the bank's standards.

The Myth of Easy Remote Account Opening

We’ve touched on this, but it’s worth repeating: the idea of opening an account with a major Hong Kong bank entirely from your home office is quickly becoming a thing of the past. With global regulations getting stricter, an in-person meeting has become standard procedure for most reputable banks.

Trying to find a workaround for a fully remote process often just leads to frustration and dead ends. It’s far better to embrace the need for a visit to Hong Kong. Doing so not only shows the bank you're serious but also gives you a fantastic opportunity to build some personal rapport with the bank manager. This proactive approach can make all the difference.

All this is happening within a remarkably stable financial environment. Hong Kong's economy continues to prove its resilience, recording 2.5% growth in 2024 and a surplus of HK$126.9 billion in its current account in early 2025. This economic strength offers a secure foundation for your funds, which is precisely why banks take their gatekeeping role so seriously. You can explore more data on Hong Kong's economic performance to understand its solid standing.

Your Top Questions Answered

Even with the best preparation, opening a bank account as a non-resident can feel like navigating a maze. It’s completely normal to have questions. I’ve put together answers to the most common queries I hear from entrepreneurs setting up shop in Hong Kong.

Can I Really Open a Hong Kong Bank Account from Overseas?

This is the million-dollar question, and the answer has definitely evolved. While a few newer digital banks and fintechs are making remote onboarding possible, the major players like HSBC, Standard Chartered, and Bank of China (Hong Kong) are pretty firm on one thing: they want to meet at least one company director in person.

Don't think of it as just a formality. This face-to-face meeting is a crucial part of their Anti-Money Laundering (AML) and Know-Your-Customer (KYC) compliance. For them, it's the gold standard for verifying who you are and understanding your business.

My advice? Treat it as a strategic business trip. Making the effort to fly in not only massively boosts your chances of approval but also lets you build a real relationship with your banker from the get-go.

What’s the Magic Number for an Initial Deposit?

There's no single answer here, as the required initial deposit can vary wildly between banks. For the big international banks, you should budget for something in the range of HK$10,000 to HK$50,000 for a new business account.

But don’t stop there. The critical follow-up questions are:

- What's the minimum monthly balance I need to maintain to avoid fees?

- Is the initial deposit negotiable if we use other bank services, like trade finance or FX?

On the flip side, many digital banks have much lower (or even zero) minimum deposit requirements. The trade-off, of course, is that they might not have the robust services—like complex trade financing or dedicated relationship managers—that you'd get from a traditional bank.

Your initial deposit isn’t just a box to tick. It’s the bank’s first real signal of your company's financial health. A solid deposit shows you’re serious and well-funded, which can make a big difference in their decision-making process.

How Long Will This Whole Process Take?

Be prepared to play the waiting game. The timeline can be unpredictable, so patience is a virtue. If you've got all your documents in perfect order and your business model is easy to understand, you can expect the approval to take about two to four weeks after your in-person meeting.

However, things can easily get bogged down. If the compliance department flags anything or wants more information—or if you're in an industry they view as higher risk (like crypto or international trading)—the process could drag on for two or even three months.

The single best thing you can do to speed it up? Be over-prepared. A polished business plan and immaculate documentation can slash the amount of back-and-forth and get you an answer much faster.

Thinking ahead is key. Many non-residents eventually look into purchasing property in their new base of operations, which is closely tied to local banking. For instance, if you were considering Australia, researching topics like buying a home as a temporary visa holder in Australia shows foresight that banks appreciate.

Conclusion

Navigating international banking doesn't have to be a solo journey. At Lion Business Consultancy Limited, we specialise in guiding entrepreneurs through every step, ensuring your banking setup is secure, compliant, and perfectly aligned with your global ambitions.

If you want an expert partner to guarantee a smooth account opening and protect your business from compliance risks, discover how our private advisory services can help you expand with confidence.