Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

When you're dealing with high-risk businesses in Hong Kong, your due diligence has to go far beyond a simple background check. Enhanced Due Diligence (EDD) isn't just more paperwork; it's a much deeper, more investigative approach to understanding your clients. Think of it as your company's proactive defense against financial crime, a crucial process mandated by the territory's tough anti-money laundering laws to ensure you really know who you’re in business with.

Why EDD is a Non-Negotiable for High-Risk Businesses

If you're an entrepreneur or running an SME in Hong Kong, the term 'Enhanced Due Diligence' might sound like another regulatory headache. But let's reframe it. Instead of a hoop to jump through, view it as a vital, in-depth conversation with your client. Standard Customer Due Diligence (CDD) is about confirming someone is who they say they are. EDD, on the other hand, is about asking the tougher questions necessary when the stakes are higher.

It’s about getting the complete picture—understanding the story behind the money, the true ownership structure, and the people pulling the strings. This isn't just about ticking boxes for the government; it's your primary defense against being used as a pawn in a money laundering or terrorist financing scheme.

These stringent rules stem directly from Hong Kong's Anti-Money Laundering and Counter-Terrorist Financing Ordinance (AMLO). The legislation puts the onus squarely on businesses like yours to identify and properly manage clients who present a greater risk.

Understanding the Regulatory Landscape

This focus on EDD isn't a mere suggestion; it's actively enforced. Regulators like the Hong Kong Customs and Excise Department (C&ED) are watching closely, and the penalties for getting it wrong can be severe.

Just look at the numbers. Between 2022 and 2023, financial institutions flagged over 3,500 suspicious transaction reports (STRs) tied to high-risk activities. That data reveals a clear trend towards more intense scrutiny. You can dig into these statistics yourself in the Hong Kong Financial Services and the Treasury Bureau's report.

What does this mean for your business? Simply put, a quick, surface-level check just won't cut it anymore for certain clients. You need a robust framework in place to protect your company.

What EDD Aims to Achieve

At its core, a strong EDD process provides clarity and confidence. It’s designed to help you:

- Verify the Source of Wealth: This means confirming where a client’s money actually came from, not just the last bank it passed through.

- Identify the Ultimate Beneficial Owner (UBO): You need to peel back the layers of complex corporate structures to find the real people who own or control the entity.

- Understand the Business Rationale: Get a clear picture of why a client is making a certain transaction or has structured their business in a particular way. Is there a legitimate, logical reason?

By building this deeper understanding, you’re not just following the law. You’re also safeguarding your company’s reputation and financial stability. It’s about shifting compliance from a painful task to a strategic tool for managing risk.

Does Your Business Fall into a High-Risk Category?

So, how do you know if regulators consider your business ‘high-risk’? It’s not always a straightforward label, and it isn't just for a handful of obvious industries. In Hong Kong, the approach is risk-based, meaning authorities look at the complete picture—not just your industry, but how you operate and who you do business with.

Think of it like setting up home security. A basic alarm might be fine for a quiet suburban street. But a mansion in a high-crime area full of priceless art? That needs a much more sophisticated, layered system. In the same way, the EDD requirements for high-risk businesses are far more stringent because the potential for financial crime is that much greater.

Your business could easily trip the wire for this higher level of scrutiny if it fits certain profiles.

The Obvious Red Flags

Some industries are automatically on the radar simply because of their nature. If your business operates in one of these sectors, you should expect EDD to be a routine part of your compliance obligations.

- Financial Services: This covers money remitters, currency exchanges, and certain types of investment firms.

- Dealers in Precious Metals and Stones: The high value and portable nature of these assets make them a classic vehicle for laundering money.

- Real Estate Agencies: Large-scale property deals can be an effective way to make illicit funds appear legitimate.

- Trust and Company Service Providers (TCSPs): These firms are in the business of creating and managing corporate structures, which, if misused, can completely obscure who really owns a company.

It’s not that these industries are inherently bad, but they present clear opportunities for criminals to exploit. As a result, regulators demand they have much stronger defenses.

Nuanced Factors That Elevate Risk

Beyond your industry, certain operational characteristics can quietly push your business into the high-risk bracket. These are the subtle weak points that regulators are trained to spot, and they demand a much closer look. To get this right, you need to apply some serious security risk assessment mastery.

Your risk profile isn’t static; it’s a living assessment shaped by your clients, your transactions, and the jurisdictions you touch. Proactive analysis is key to staying compliant.

Ask yourself if any of these situations sound familiar:

- Complex Ownership Structures: Is the ownership trail deliberately confusing? Using multiple layers of offshore shell companies or trusts is a classic way to hide the Ultimate Beneficial Owner (UBO), and it’s a massive red flag.

- Dealings with Politically Exposed Persons (PEPs): Individuals holding prominent public office, along with their families and close associates, present a higher risk for potential bribery and corruption.

- Transactions from High-Risk Countries: If you're doing business with clients or receiving funds from jurisdictions known for weak anti-money laundering controls or high levels of corruption, your risk level automatically shoots up.

- Non-Face-to-Face Business: When you can't meet your clients in person, properly verifying who they are becomes much more difficult. This gap creates an open invitation for fraud.

Getting a handle on these factors is about more than just ticking boxes. It’s about proactively managing your own risk profile before a regulator shows up and does it for you.

Breaking Down the EDD Investigation Process

When a client gets flagged as high-risk, a standard check simply won't cut it. You have to think of the Enhanced Due Diligence (EDD) process less like a bureaucratic task and more like a financial detective's case file. You're moving beyond simply verifying an identity to truly understanding the story behind the money and, more importantly, the people who control it. This deep dive is the only way to meet the EDD requirements for high-risk businesses and shield your own company from trouble.

At its heart, the entire process is built on a simple idea: ask better questions to get undeniable proof. It’s an active investigation, not a passive one. You have to be prepared to peel back layers of corporate complexity to get to the truth of a business relationship.

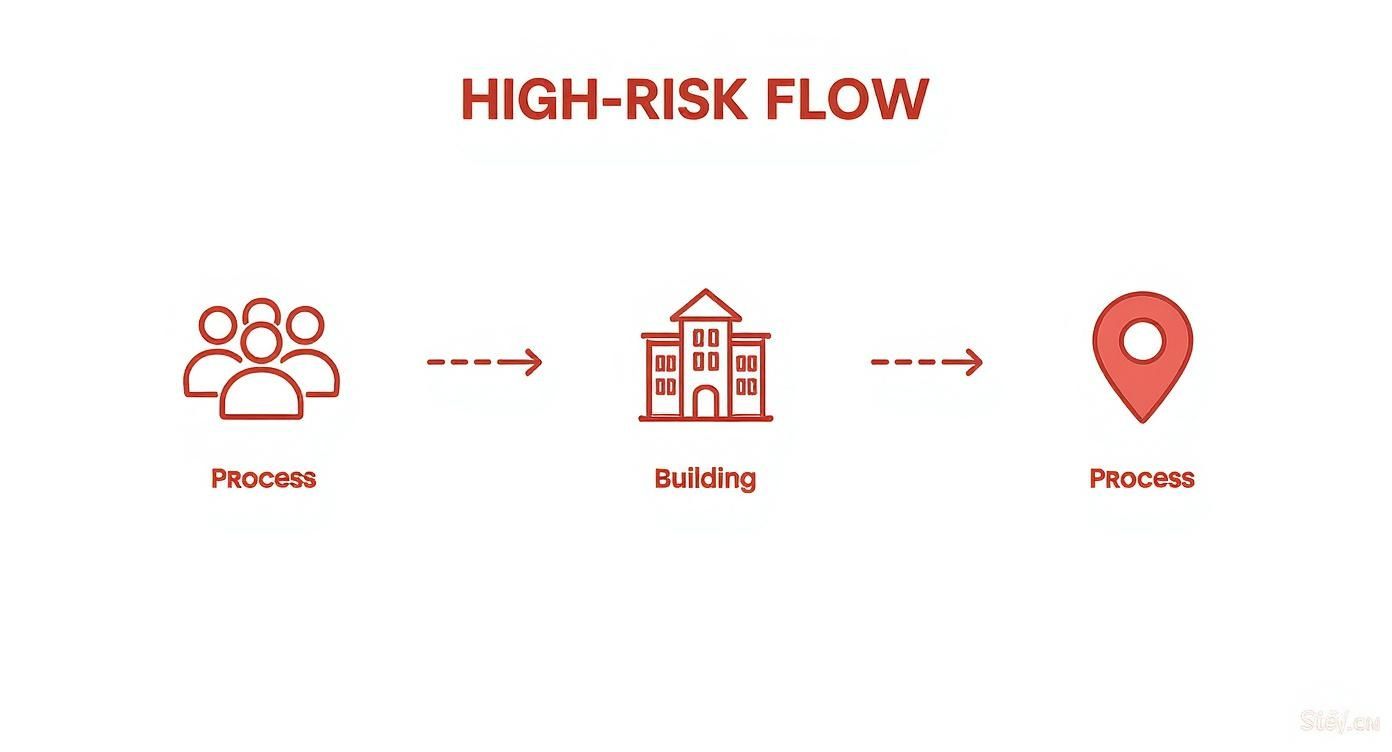

This infographic breaks down the key areas you'll need to focus on when a high-risk flag pops up.

As you can see, a proper EDD investigation means scrutinizing the people involved, digging into the complexity of their business structure, and weighing the risks tied to where they operate.

Identifying the True Ultimate Beneficial Owner

First things first: you absolutely must identify the Ultimate Beneficial Owner (UBO). This is the real person—the flesh and blood—who ultimately owns or controls the company. It's common for high-risk entities to use tangled webs of shell corporations or trusts spread across different jurisdictions, all designed to obscure the UBO’s identity. Your job is to cut right through that fog.

This means getting your hands on shareholder registers, articles of incorporation, and trust deeds—and then verifying them. You can't just take the client's word for it. You need to see the official paperwork that proves, without a doubt, who is really pulling the strings. We cover more strategies for these crucial early steps in our guide, https://lionbusinessco.com/the-bank-onboarding-risk-playbook-2025/.

Scrutinizing the Source of Wealth and Funds

Once you’re certain who the UBO is, the next critical step is to verify their Source of Wealth (SoW) and the Source of Funds (SoF) for the specific business you're doing with them. It’s easy to mix these two up, but they are distinct.

Source of Wealth is the big picture. It’s about a person's entire net worth—how did they build their fortune over a lifetime? Source of Funds, on the other hand, is transactional. It’s about the specific money being used in your business relationship—where did this particular payment originate?

For instance, if a client’s wealth came from selling a tech startup, you’ll need to see the sale agreement and the bank statements showing the proceeds landing in their account. But if the funds for your transaction are coming from a recent property sale, you’ll need to see evidence of that sale. This level of scrutiny is what ensures you aren’t inadvertently handling dirty money.

As part of this, using advanced techniques to gather publicly available information can be a game-changer. For a closer look at these methods, resources on Background Checking Using OSINT are invaluable. This kind of open-source intelligence often uncovers adverse media reports or other red flags that formal documents might never show, giving you a much more complete picture of the risk you're taking on.

Mastering Your Documentation and Audit Trail

In the world of regulatory compliance, there's a golden rule: if it isn't written down, it didn't happen. The strength of your Enhanced Due Diligence investigation comes down to the quality of the records you keep. This paper trail is your best defense, proving to regulators that you’ve done your job thoroughly and thoughtfully.

Think of each high-risk client file as telling a complete story. It needs to walk someone through the entire journey—from your initial risk assessment to the final sign-off and all the monitoring in between. This audit trail is exactly what regulators will pick apart, so it needs to be bulletproof.

The goal here is simple: build a rock-solid, organized record that leaves no questions about your process.

Building a Rock-Solid Client File

A well-organized client file tells a clear story. It should be structured so that anyone, whether it's an internal colleague or an external auditor, can immediately grasp the client's risk profile and understand the exact steps you took to mitigate it.

This file becomes the single source of truth for every piece of evidence you've gathered and every decision you've made along the way.

A strong audit trail is more than just a collection of documents; it's a clear demonstration of your company's commitment to a robust compliance culture. It proves you not only follow the rules but also understand the principles behind them.

To meet the demanding EDD requirements for high-risk businesses, your file needs to contain specific, verified documents. This isn't just about ticking boxes; it's about building a comprehensive locker of evidence.

Key Documents for Your EDD Audit Trail

While every client's situation is different, a standard high-risk file should always contain a core set of documents. Vague notes or missing paperwork are the fastest way to create a hole in your compliance armor.

Here's a checklist of the essentials you need to gather and maintain:

- Identity Verification: Get certified copies of government-issued IDs, passports, and recent proof of address for all Ultimate Beneficial Owners (UBOs) and key directors.

- Corporate Structure Documents: You'll need official copies of the certificate of incorporation, articles of association, and shareholder registers. These help you map out the entire ownership chain, leaving no stone unturned.

- Source of Wealth (SoW) and Funds (SoF) Evidence: This is the big one. You need tangible proof—think audited financial statements, tax returns, signed sale agreements for major assets, or bank statements that clearly trace the origin of the client's money.

- Risk Assessment Records: Keep detailed, dated notes from your internal risk assessment. Crucially, this must explain why you flagged the client as high-risk and list the specific factors that led to that decision.

- Communication Logs: Document every significant conversation with the client. This means saving important emails and writing up detailed summaries of any phone calls or meetings where compliance was discussed.

For companies with complex offshore structures, the paperwork can get even more intense. You can find out more about tackling these specific hurdles in our guide on how to pass KYC for offshore companies. Getting this documentation right isn't just about staying compliant—it's about protecting your business from the ground up.

Keeping a Watchful Eye: Continuous Monitoring for High-Risk Clients

Enhanced Due Diligence isn’t something you do once and then file away. It’s an ongoing commitment. A client’s risk profile isn’t set in stone; it can change, sometimes overnight and without any warning. This is why a solid, continuous monitoring system is a cornerstone of the EDD requirements for high-risk businesses.

Think of it like a smoke detector for your client base. A single check when you first bring them on board is a good start, but it won’t catch a fire that breaks out six months later. Continuous monitoring is the system that keeps watch, ready to sound the alarm at the first whiff of smoke.

This proactive approach is what real compliance is all about. It means building a living framework that reacts to new information, making sure you’re always a step ahead of any new risks that pop up.

Knowing When to Take a Closer Look: Setting Review Triggers

Effective monitoring really comes down to knowing what to look for. You need to set up clear, pre-defined triggers that automatically kick off a fresh EDD review for a high-risk client. If you don't have these in place, it’s far too easy for dangerous changes to slip through the cracks.

Your system should be calibrated to flag specific events, such as:

- Unusual Transaction Patterns: A client who usually deals in small amounts suddenly tries to send a large, out-of-character wire transfer.

- Negative News Alerts: The client’s name starts appearing in news reports linked to financial crime, sanctions, or other shady activities.

- Changes in Company Structure: An unexpected switch in the Ultimate Beneficial Owner (UBO) or the appointment of new directors, particularly if they’re based in high-risk jurisdictions.

- Appearance on a Sanctions List: An alert that the client, or someone newly connected to them, has been added to an official government sanctions list.

These triggers are your early warning system. They give you the chance to reassess the relationship before a manageable risk spirals into a major compliance disaster.

Ongoing monitoring transforms your EDD process from a snapshot into a live feed. It's the difference between looking at a single photo and watching a continuous video of your client's activities.

This constant vigilance is especially important in a complex economy. For instance, Hong Kong’s shifting labour market can increase the risk of financial crimes like payroll fraud or schemes involving fictitious employees. Rigorous monitoring is essential to ensure high-risk employment practices don’t become a backdoor for illicit funds. This works in tandem with agencies like the Labour Department, which carries out over 2,000 inspections each year. For a deeper dive, the State of Labour in Hong Kong report offers more context.

Today, many firms lean on automated monitoring tools to act as a digital partner in this process. These platforms can scan global watchlists, monitor transactions as they happen, and screen for adverse media 24/7. They're designed to catch suspicious patterns that a manual check would almost certainly miss, creating a powerful and adaptive defense when combined with human expertise.

Common EDD Mistakes and How to Avoid Them

Learning from the missteps of others is one of the smartest ways to stay on top of the EDD requirements for high-risk businesses. Even with the best intentions, companies often stumble into the same predictable traps. Getting to know these common pitfalls is the first step in building a compliance framework that actually works.

One of the biggest blunders we see is teams treating EDD like a simple checklist. They go through the motions, gathering documents without ever stopping to think critically or understand why each step matters. This approach creates a dangerous illusion of security, leaving behind massive gaps that regulators can drive a truck through.

Another classic error is failing to document the logic behind your decisions. It’s not enough to just have a folder stuffed with paperwork; you have to record why you decided a red flag was acceptable or why a certain document was sufficient proof of wealth. Without that narrative, your audit trail is telling only half the story.

Inadequate Training and Neglecting Monitoring

Putting staff on the front line with insufficient training is another recipe for disaster. If your team doesn't grasp the specific financial crime risks relevant to Hong Kong, they simply won't know what to look for. An untrained employee isn't just a weak link; they're a significant liability.

Finally, so many businesses treat EDD as a one-and-done event. They’ll perform a deep dive during onboarding and then file the client away, assuming their risk profile is set in stone.

In reality, a client's risk can change overnight. Neglecting continuous monitoring is like installing a state-of-the-art alarm system but never turning it on after the first day.

To sidestep these common stumbles, you need to build a culture of proactive compliance. Here are a few practical ways to keep your EDD program robust and effective:

-

Think Beyond the Checklist: Train your team to approach each case like an investigator. Encourage them to ask tough questions and see how different pieces of information connect, rather than just ticking boxes.

-

Document Everything: For every major decision made during the EDD process, create a detailed note explaining your reasoning. This context is just as crucial as the evidence you've collected.

-

Invest in Ongoing Training: Make sure your staff are regularly updated on the latest money laundering trends, regulatory shifts in Hong Kong, and new investigative techniques.

-

Systemize Your Monitoring: Put a system in place with clear triggers for both periodic and event-driven reviews. Technology can be a huge help here, automatically flagging unusual activity and ensuring nothing important slips through the cracks.

Common Questions About EDD Answered

Getting your head around Enhanced Due Diligence can feel a bit overwhelming, especially when you're also trying to run a business. Let's break down some of the most frequent questions we hear from entrepreneurs and compliance officers grappling with EDD requirements for high-risk businesses in Hong Kong.

What Is the Real Difference Between CDD and EDD?

The easiest way to think about it is to compare it to building security.

Standard Customer Due Diligence (CDD) is like the security guard at the front desk. They check your ID, make sure your face matches the photo, and confirm you're on the visitor list. It’s a basic but essential check to answer the question, "Are you who you say you are?"

Enhanced Due Diligence (EDD), however, is the full-blown security detail you’d see for a visiting diplomat. It's a much deeper dive reserved for individuals who pose a higher risk. EDD digs into far more difficult questions, like, "Where did this person's money actually come from?" and "What is the true purpose of this business relationship?" This process requires more proof, more scrutiny, and constant check-ins.

How Often Should We Review Our High-Risk Customers?

There isn't a single, hard-and-fast rule written down by regulators, but the gold standard in the industry is to conduct a full EDD review at least once a year for any high-risk client. But don't just circle a date on the calendar and forget about it. That's a classic mistake.

The real key is conducting 'event-driven' reviews. These are reviews prompted by specific red flags that could change a client's risk level. For example:

- A sudden, large transaction that’s completely out of character for their usual business activity.

- Negative media coverage surfaces, linking the client to corruption or other financial crimes.

- They unexpectedly change their company’s ownership or legal structure without a clear explanation.

Staying alert and reacting to what’s happening in real-time is much more effective than blindly sticking to a schedule.

Can We Use Software to Handle EDD?

Absolutely, and frankly, you probably should. Modern Anti-Money Laundering (AML) software is an indispensable tool. It can automatically check names against global sanctions lists, screen for Politically Exposed Persons (PEPs), flag unusual transactions as they happen, and keep all your records organized for an audit.

But here’s the crucial part: technology is an expert assistant, not a substitute for human intelligence. Your compliance team still needs to look at the data, use their judgement, and make the final call on the risk. The software helps, but the responsibility is still yours.

Navigating these complex requirements is where expert guidance makes all the difference. At Lion Business Consultancy Limited, we act as your strategic partner, designing compliant frameworks that protect your business and support your global growth.