Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

Navigating offshore KYC often feels like solving a jigsaw puzzle under a tight deadline. I remember working with a startup in Kowloon—by front-loading certified IDs, clear proof of address, and well-organised substance documents, they slashed their bank approval time in half. This guide walks you, the entrepreneur or SME owner, through each critical milestone so you breeze through both bank and regulator checks without the usual headaches.

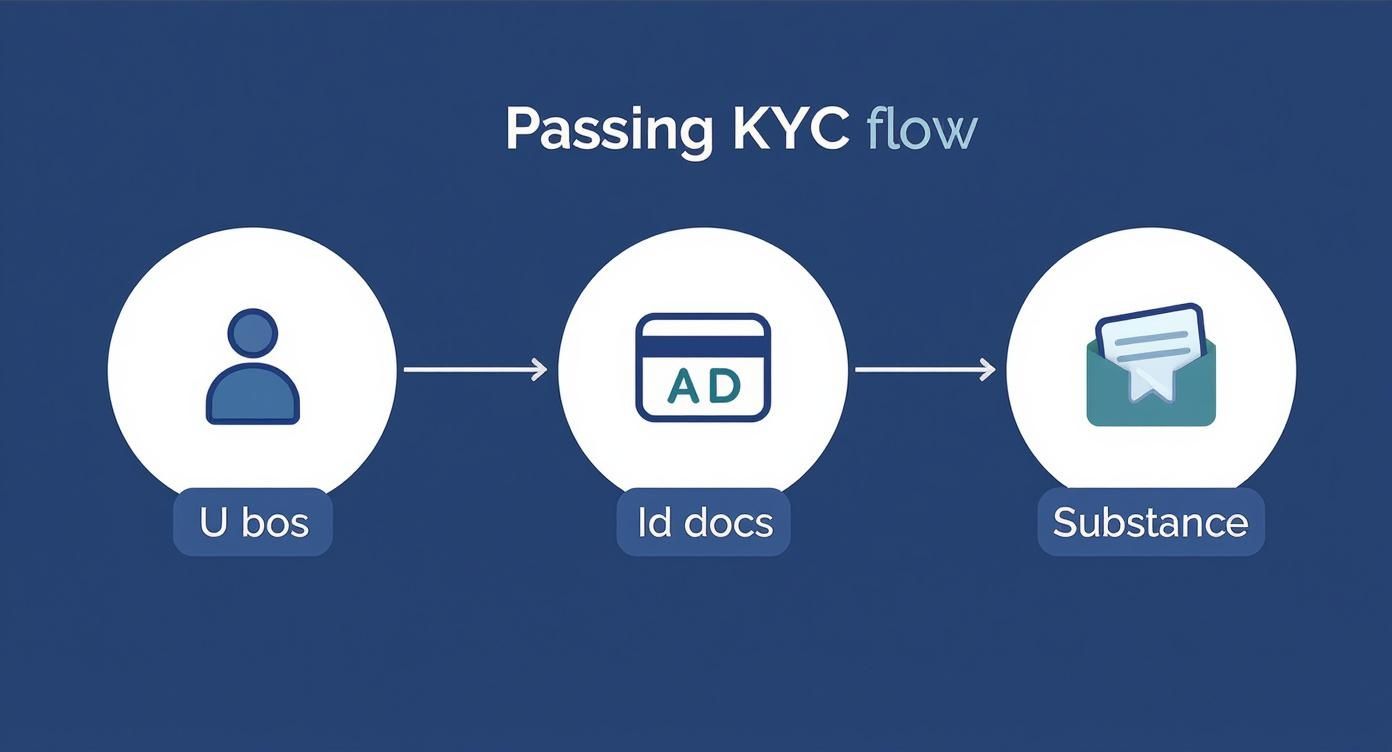

Key Steps To Pass KYC For Offshore Companies

Here’s a consultative breakdown of what really moves the needle for smooth approvals:

-

Clarify Ultimate Beneficial Ownership

Obtain high-resolution passport scans and current address proofs for every single UBO in your structure—no exceptions. -

Notarise Identity And Address Documents

Check each bank’s certification requirements in advance and stick to one format for IDs, utility bills or bank letters. -

Document Economic Substance

Collect office leases, payroll logs or board minutes that clearly show local operations—and label them by date. -

Plan Annual Refreshes

Set recurring calendar reminders for renewals so you’re always ahead of expiry dates, not scrambling at the last minute.

When every document arrives certified and consistently formatted, relationship managers can tick off your file in one go.

Key Steps To Pass KYC For Offshore Companies

Below is a high-level snapshot of each action, why it matters and the paperwork to keep at hand.

| Step | Objective | Required Documents |

|---|---|---|

| UBO Verification | Confirm the real owners | Passport copies, recent address proof |

| ID Documentation | Validate each individual | Notarised IDs, utility bills or bank letters |

| Substance Evidence | Prove genuine local activity | Office leases, payroll logs, board meeting minutes |

| Annual Refresh Cycles | Stay compliant year after year | Updated IDs, renewed proof of address |

Keep this checklist close—it flags any gaps before they become blockers.

Regulatory Highlights

By 2025, the Hong Kong Monetary Authority has ramped up AML and KYC requirements to a new level. Any transaction over HKD 100,000 (approx. USD 12,800) now demands explicit source-of-funds proof, plus annual updates aligned with CRS and FATCA standards. Learn more about these requirements on YBCase.

Having your UBO list and substance proof ready from day one can speed up your bank approval by weeks.

Need extra tactics? Dive into our guide on opening offshore company bank accounts for a deeper playbook. Start early, partner with experienced advisors, and you’ll sail through compliance.

Understanding Hong Kong KYC Evolution

Hong Kong’s compliance landscape has transformed dramatically. Back before 2015, a passport copy and company registration certificate often sufficed. Fast-forward to today, and economic substance, digital KYC tools, and detailed ownership registers are non-negotiable.

You can trace the evolution through these milestones:

- Pre-2015 Checks: Passport copies and incorporation certificates

- FATCA Impact: US tax reporting kicks in from 2010

- CRS Adoption: Global tax data exchange starts in 2014

- 2020 Substance Rules: Offices, staff and board minutes mandated

- VASP Regime June 2023: Crypto providers face mandatory KYC

Modern Compliance Drivers

When CRS arrived in 2014 and FATCA preceded it in 2010, Hong Kong banks overhauled their due diligence playbooks. By 2023, roughly 35% of new offshore accounts were rejected due to incomplete or inconsistent papers. A logistics startup I advised lost six weeks dealing with a virtual-office address mismatch alone.

Here’s a pro tip: draft an entity-relationship diagram before submission. One SME cut its KYC review time by 40% after sharing a clear ownership chart with bankers.

Examples that typically smooth the path:

- Trade Finance: Invoices that trace money flows

- Real Estate Vehicles: Property deeds plus lease schedules

- Crypto Ventures: Verified wallet addresses and exchange records

- Investment Funds: Audited NAV statements and subscription agreements

Sector Specific Scrutiny

Financial tech companies should be ready to show transaction-monitoring logs. Commodity traders may need supplier contracts and shipping manifests. Anticipate these sector calls to avoid last-minute document hunts.

Deepen your understanding of offshore privacy trends for 2025 on Offshore Company Reg

Comparison Of KYC Stages

| Period | Focus | Key Requirements |

|---|---|---|

| Pre-2015 | Identity Verification | Passport copies, incorporation documents |

| 2015-19 | Reporting And Transparency | FATCA filings, CRS data exchange |

| 2020+ | Substance And Digital KYC | Office leases, payroll logs, biometric scans |

Emerging Digital Tools

Banks now offer secure portals with biometric facial recognition and AI-driven sanction screening. Upload certified docs, track your status in real time, and say goodbye to endless email threads. Yet, a wrong file format or missing metadata can still trip you up.

“Digital identity verification cut onboarding time by half for one Hong Kong fintech client.”

Key Takeaways

- Show genuine economic substance—beyond a simple letterhead

- Keep up-to-date beneficial-ownership details with fixed annual refreshes

- Embrace biometric and AI tools early in the process

- Map regulator checkpoints and lock in internal deadlines

Armed with this history, you’re set to assemble your offshore KYC and substance evidence pack. Let’s dig into the details next.

Preparing Documentation And Substance Evidence

A well-structured document set is your best defence against delays. Start by sourcing certified true-copy passports, corporate registration certificates and audited financial statements from HKICPA-registered auditors.

Organise files under clear headings, include certified translations, and use a consistent naming system. This guides compliance officers through your submission and minimizes clarifications.

Essential Identity And Registration Documents

-

Certified True Copy Passport

Signed, valid and notarised to bank standards. -

Corporate Registration Certificate

Displays legal name, registration number and incorporation date. -

Memorandum And Articles Of Association

Outlines governance structure and business scope. -

Certificate Of Good Standing

Issued within three months to confirm regulatory compliance.

Maintain both digital and original certified hard copies. A thorough legal document review catches formatting issues before you submit.

Demonstrating Economic Substance

Virtual offices no longer pass muster. Banks want proof of active operations:

-

Office Lease Agreement

Shows lease term, address and landlord contact. -

Local Staff Payroll Logs

Records employee names, salaries and roles. -

Board Meeting Minutes

Documents meeting dates, Hong Kong venues and resolutions.

Pair these with audited financials from HKICPA-registered auditors. According to 2024–2025 industry data, 70% of offshore bank applications stall because firms can’t prove substance. Discover more insights here.

For additional context, see our guide on opening an offshore company.

| Document Type | Purpose |

|---|---|

| Passport Copy | Confirms identity of beneficial owners |

| Registration Certificate | Verifies legal formation |

| Lease Agreement | Proves physical office presence |

| Audited Financial Statements | Validates actual revenue and substance |

Properly structured documentation convinces compliance officers of your readiness and reliability.

Common Packaging Mistakes

-

Overloaded Files

Too many docs in one PDF slow down quick scans. -

Missing Cover Pages

Reviewers rely on a clear index to navigate. -

Inconsistent Certification

Varying notary stamps or absent dates trigger red flags.

Avoid these simple errors to keep your application on track.

Translation And Certification Tips

Non-English documents need certified translations plus a translator’s affidavit, verifying credentials in Hong Kong. The Hong Kong Translation Society offers accredited experts.

Adopt a naming convention like:

- UBO01_Passport.pdf

- CompanyCert_2025.pdf

- Lease_HQ_2024.pdf

Finish with a master index sheet that matches file names to titles. This one-page summary accelerates both internal checks and bank reviews.

Implementing Due Diligence Best Practices

Solid KYC goes beyond forms—it’s about clear presentation, timely refreshes and systems that flag expiry dates. Email threads often mean missing attachments and slow responses. Migrating to a secure digital portal transforms the experience.

One SME I coached reported a 60% drop in missing-document queries after switching platforms.

Harness Secure Digital Onboarding

A centralized portal offers version control, timestamps and comment histories. Everyone—your team and the bank’s compliance officers—sees exactly what’s uploaded and when.

- Central dashboard displays pending, approved and rejected files

- Automatic reminders at 30-day and 7-day intervals

- Encrypted channels that align with HKMA guidelines

This approach cuts hours of email back-and-forth.

Optimise File Organisation

| Approach | Time Saved | Pain Points |

|---|---|---|

| Manual | 0% | Email clutter |

| Portal | 50% | Setup overhead |

| Hybrid | 30% | Sync issues |

Investing in a secure portal quickly pays for itself in saved hours.

Align your internal milestones with the bank’s review cycles:

- Kick-off meeting to assign roles and responsibilities

- Midpoint audit with your relationship manager (around three weeks in)

- Final check two weeks before submission to reconcile all files

Visual calendars keep everyone accountable.

Proactive timelines trimmed approval delays by 35% for one client.

Choose the Right Scheduling Tools

Run a small pilot batch through your project management app before full rollout:

- Trello for checklist tracking

- Asana for automatic reminder tasks

- Google Calendar invites to lock in deadlines

Pick the tool that suits your team’s size and complexity.

Use Third-Party Verification Early

Bringing in a specialist three weeks before final submission pays dividends. These services catch registry errors, expired certificates and name mismatches ahead of time.

Analyse Verification Reports Quickly

Review third-party findings within 24 hours and resolve issues before submission. Keep your relationship manager in the loop with concise audit trails and clear ownership charts:

- Audit Trails record every document change

- Ownership Charts map UBO structures visually

- Proactive Updates deliver monthly status reports via the portal

Build Trust With Relationship Managers

Personal rapport is as valuable as flawless documents. A quick video walkthrough of complex ownership structures can halve follow-up queries. Send meeting summaries within 24 hours, including:

- Highlighted action items and owners

- Deadlines and next steps

- Attached reference documents

Maintain Ongoing Communication

| Task | Owner | Deadline |

|---|---|---|

| Verify UBO documents | Legal Officer | Day 1 of cycle |

| Confirm office lease status | Admin Manager | Day 5 of cycle |

| Validate translation quality | Compliance Advisor | Day 10 of cycle |

| Submit to bank portal | Project Lead | Day 15 of cycle |

Well-structured checklists reduce surprises and keep due diligence on point.

For deeper risk insights and detailed timelines, explore the Bank Onboarding Risk Playbook 2025.

“Organising KYC materials like this saved our finance team 20 hours per application,” says a fintech founder.

Standardising these practices across offshore entities means fewer bottlenecks and faster approvals.

Take Proactive Control

Start applying these best practices today to streamline your KYC journey and secure your international operations.

Contact Lion Business Co. for private advisory that keeps your compliance calendar on track.

Avoiding Common Pitfalls And Resolving Issues

Even the most meticulous teams can hit snags. Spotting roadblocks early saves time and frustration. Here are three frequent triggers and tested fixes from real audits.

Mismatched Beneficiary Records

Minor discrepancies in UBO info—like an extra space or a percentage point off—can freeze your application.

- Cross-check UBO data against official filings, matching names and share allocations to the decimal.

- Use a centralized spreadsheet with validation rules to flag typos.

- Engage an external reviewer for a blind audit; fresh eyes often catch hidden errors.

An auto-sync share registry platform can eliminate manual entry mistakes and free your compliance team for higher-impact tasks.

“Aligning our cap table with bank records eliminated a week of back-and-forth,” recalls a fintech CFO.

| Action | Purpose |

|---|---|

| Consolidate UBO data | Spot mismatches before submission |

| Verify with registry | Confirm details against official records |

| Share updated file | Proactively address queries |

Flagged Virtual Office Addresses

Banks view virtual offices as high-risk mailboxes. Show real workspace activity to pass scrutiny.

- Secure a serviced office lease naming your company

- Provide utility bills (electricity or water) in the company’s name

- Include photos of signage, reception and a brief office-tour video

- Attach a recent supplier invoice to match the lease address

These elements prove you have an operational HQ, not just a P.O. box.

Unexplained Dormant Accounts

An inactive account looks like a shell. Even minimal cash flow shows genuine intent.

- Schedule monthly transfers under HKD 5,000 for admin costs

- Keep a transaction log with dates and purposes

- Respond within 24 hours if you receive a dormancy notice:

Dear Compliance Team,

Please find attached our account activity schedule for the past six months. We have conducted monthly transfers under HKD 5,000 for administrative expenses. All entries align with our planned cash flow. Let us know if any further clarification is needed.

Quick Case Study

A Kowloon logistics SME faced six weeks of KYC rejections. A preventive compliance audit tackled every issue:

- Cleaned up UBO records with registry confirmation

- Secured a full-time serviced office lease plus utility proofs

- Launched monthly transaction drills for small vendor payments

Result: application delays fell from six weeks to three—a 50% reduction in hold time.

Play-By-Play Template For Bank Queries

Speed and clarity win when banks come back with questions. Adapt this structured reply:

| Step | Content | Purpose |

|---|---|---|

| 1 | Query ID and subject line | Ensures fast routing |

| 2 | Issue summary | Clarifies the question |

| 3 | Attached documents | Provides evidence immediately |

| 4 | Brief explanation (≤100 words) | Keeps compliance teams focused |

| 5 | Next steps and timeline | Sets expectations effectively |

| 6 | Polite closing and sign-off | Builds rapport |

Strengthening Credibility Through Hiccups

Every compliance hiccup is a chance to reinforce trust. Keep a one-page summary of each fix, archive original queries, and plan a mini-audit six months post-approval. This disciplined approach not only speeds future KYC cycles but also cements your reputation with banks and service providers.

Contact Lion Business Consultancy for a private audit that nips KYC issues in the bud and keeps your offshore structure bankable.

Book your free consultation today to safeguard your business against KYC setbacks.

Visit our website for detailed support.

Questions - How to Pass KYC for Offshore Companies Successfully

Getting through Hong Kong KYC isn’t just box-ticking. Each bank has its own quirks, so understanding common questions makes the journey far less daunting.

What Banks Accept Offshore Company Accounts

Several global players and local favourites welcome offshore structures—each with its own risk appetite and fee structure.

• HSBC favours larger corporations but requires heftier deposits.

• Standard Chartered and Citibank maintain transparent KYC processes.

• Regional banks often approve faster, though they’ll want detailed substance proof.

One fintech founder I worked with landed an HSBC account in just three weeks by submitting a crystal-clear UBO chart alongside substance documents in a single batch.

How Long Does KYC Processing Take

Processing times range from a couple of weeks to two months, depending on complexity and paperwork quality:

• Digital ID–based setups clear in 2–3 weeks.

• Applications needing audit reports or ownership breakdowns take 4–6 weeks.

• Complex, multi-layered structures can stretch to 6–8 weeks.

A trading firm I advised cut nearly a month off their timeline, securing sign-off in 18 days by uploading certified IDs and detailed diagrams from the start. Stay in close touch with your relationship manager to head off surprises.

What To Do When Documents Are Rejected

Rejections happen—they’re a chance to refine your submission. Follow these steps:

• Review the rejection notice to identify missing or incorrect fields.

• Gather the required documents—this might mean fresh board minutes or notarised translations.

• Resubmit via the bank’s secure portal, attaching a concise cover note referencing your application ID.

If doubts persist, loop in your compliance advisor. They’ll help you address issues head-on.

Quick Tip: A polite, concise cover note outlining changes can cut back-and-forth by over 35%.

Do I Need Local Directors And Staff

Hong Kong’s economic substance rules expect genuine onshore decision-making. You don’t need a large team, but you do need proof of real activity.

| Requirement | Minimum Expectation |

|---|---|

| Resident Director | One Hong Kong–based director |

| Local Staff | At least one employee on payroll |

| Board Meeting Minutes | Records showing meetings held in HK |

Clients often share service agreements featuring their office address, keep detailed minutes with agendas, and note director availability for bank interviews. Even a single payroll slip can go a long way toward compliance.

Ready to streamline your offshore KYC journey with expert support? Reach out to Lion Business Consultancy Limited and let’s get your application over the line.