Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

Let’s get straight to it. When people talk about the company tax rate Hong Kong businesses pay, they’re often missing the most important detail: it’s not just one flat number.

Imagine you’re a startup or a growing business. For you, the first HK$2 million in profit is taxed at a remarkably low 8.25%. It’s only the profit above that threshold that gets hit with the standard 16.5% rate. This isn’t just a small detail; it’s a game-changer designed to fuel your growth.

Understanding Hong Kong’s Two-Tier Tax System

If you’re running a business here, you’ve undoubtedly heard about Hong Kong’s famously simple and low-tax environment. But what does that actually look like on your balance sheet? The secret sauce is the Two-Tier Profits Tax System, a policy specifically crafted to give growing businesses a powerful leg up.

Think of it as a welcome discount on your success. Your first major milestone—that initial HK$2 million in assessable profits—is taxed at half the standard rate. This is a deliberate strategy, not a gimmick. It’s designed to ease the cash flow burden on startups and SMEs right when they need that capital the most.

A Closer Look at the Rates

This system means your tax burden is intentionally lighter when you’re building momentum. It’s a fundamental part of Hong Kong’s pro-business reputation, sending a clear signal: the city wants its smaller enterprises to thrive.

Here’s a quick reference to see how it works.

Hong Kong Profits Tax Rates at a Glance

| Assessable Profits Bracket | Applicable Tax Rate |

|---|---|

| First HK$2,000,000 | 8.25% |

| Profit above HK$2,000,000 | 16.5% |

This structure, in place since the 2018/19 assessment year, provides targeted relief exactly where it’s needed. As the Hong Kong government’s tax portal outlines, this creates a blended effective rate that scales with your success. A company earning HK$3 million, for example, isn’t paying a flat 16.5%—their total tax bill would be far lower.

“The beauty of Hong Kong’s tax system isn’t just the low headline rate; it’s the intelligent structure. The two-tier system is a powerful incentive, effectively telling entrepreneurs, ‘We support your initial journey to profitability.'”

Why This Matters for Your Business

Getting your head around this two-rate system is absolutely crucial for sound financial planning. It’s not about one number but how the two blend together to shape your final tax liability. This is the reality of the company tax rate Hong Kong businesses face.

Here’s the practical impact:

- More Cash for Growth: A lower tax bill on early profits means more money stays in your pocket. You can reinvest it into marketing, hiring that key person, or developing your next product.

- A Real Competitive Edge: This tax advantage helps smaller companies go toe-to-toe with bigger, more established competitors.

- Refreshingly Simple Compliance: Even with two tiers, the system is far more straightforward than the labyrinthine tax codes you’ll find elsewhere.

Now that you have the big picture, we’ll get into the nitty-gritty of who qualifies and how to calculate your profits correctly. For a more comprehensive look at the mechanics, our guide on Hong Kong profits tax is a great next step.

How the Two-Tier Profits Tax System Really Works

So, we know the headline figures: 8.25% on the first HK$2 million and 16.5% on everything after that. But there’s a story behind these numbers. The two-tier system isn’t just a random discount; it’s a deliberate strategy to give startups and small to medium-sized businesses (SMEs) a serious launchpad.

Think of it as a financial tailwind. The Hong Kong government understands that the early days of a business are often the toughest. By slashing the tax rate on your initial profits, the system creates vital breathing room. This allows you to reinvest back into the business, hire key people, and build momentum right when you need it most. It’s a cornerstone of the low company tax rate Hong Kong is famous for.

Who Qualifies for the Lower Rate?

This tax break is generous, but it’s not a free-for-all. The Inland Revenue Department (IRD) put rules in place to ensure the benefits land exactly where they’re intended: with genuine SMEs and startups, not large corporations looking to game the system.

For most new, standalone businesses, qualifying is a breeze. If your company is a single entity without a web of subsidiaries, you can almost certainly apply the lower 8.25% rate to your first HK$2 million in assessable profits.

Things get a bit more complex, however, if you own or control more than one company. This is where the ‘connected entity’ rule becomes incredibly important.

Understanding the Connected Entity Rule

Let’s imagine a large group with ten subsidiary companies. Without any rules, they could simply spread their profits across all ten, claiming the 8.25% rate on the first HK$2 million for each one. This would let them dodge the standard 16.5% rate and unfairly slash their tax bill.

To prevent this, the government introduced the connected entity rule.

Simply put, if you have a group of connected companies—where one company controls another, or they all fall under the control of the same person or entity—only one company in that group can choose to use the two-tier rates in a given tax year.

All the other companies in that group will be taxed at the flat 16.5% rate on all their profits. This keeps the playing field level and ensures the tax relief is properly targeted.

- What does ‘control’ mean? It typically means owning more than 50% of the shares, voting rights, or entitlement to the profits of another company.

- Who picks the company? The group gets to nominate which entity will use the two-tier rates for the year. This decision isn’t set in stone; you can change it each year, which opens the door for some smart tax planning.

- Why does this matter for entrepreneurs? If you plan on launching multiple ventures in Hong Kong, getting your head around this rule is non-negotiable. How you structure your companies will directly determine which one gets the benefit of the lower tax rate.

This isn’t just a bit of administrative red tape; it’s a fundamental mechanism that maintains the integrity of Hong Kong’s tax system. By understanding the connected entity rule, you can design your business structure to be both compliant and efficient, making sure you take full advantage of the competitive company tax rate Hong Kong offers without accidentally falling foul of the rules.

Calculating Your Company’s Taxable Profits

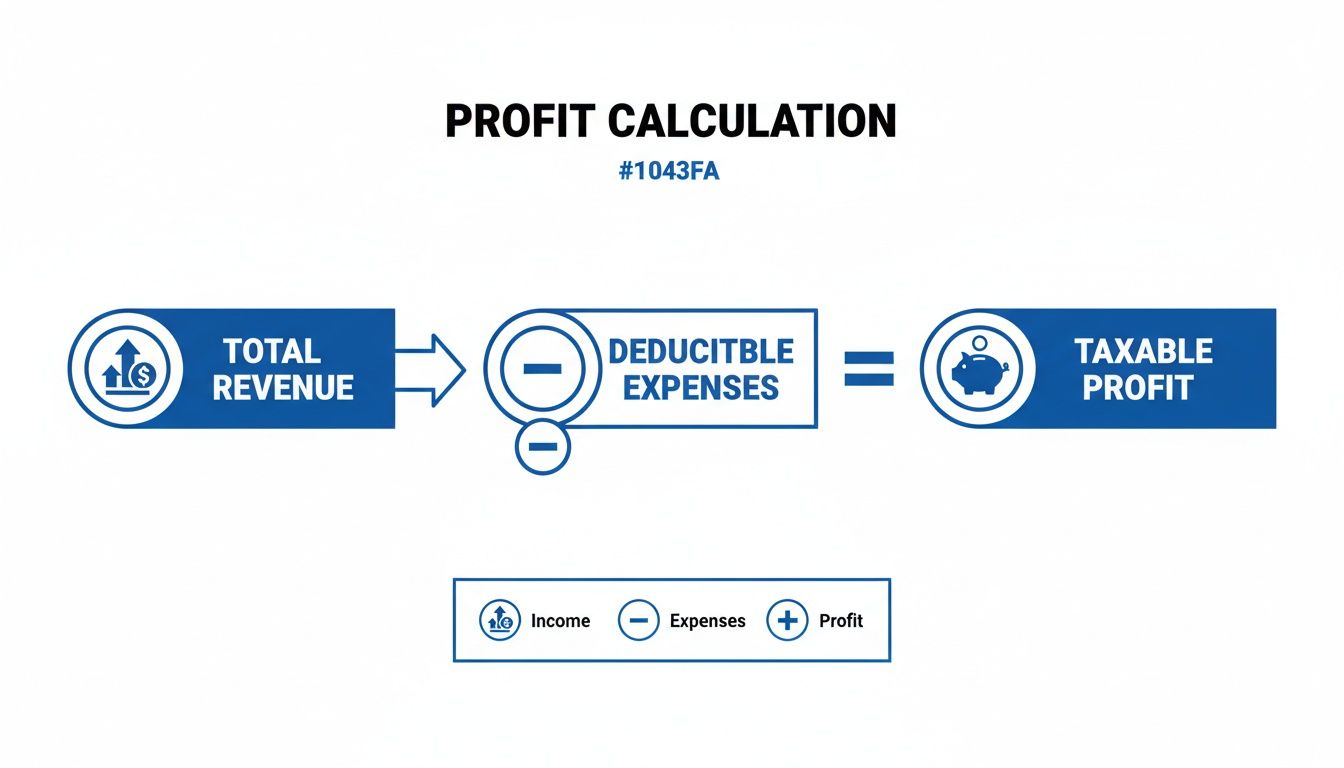

The tax rates are just numbers on a page. The real question for any founder is: how do they actually apply to my business? This is where theory hits your bank account, and it all starts with a concept called assessable profits.

Think of it like this: your total revenue for the year is the starting line. Your assessable profit is the finish line you’re taxed on. Every legitimate business expense you incur along the way helps you shorten that distance, directly reducing your final tax bill.

Getting from Total Revenue to Taxable Profit

Figuring out your taxable profit isn’t some dark art; it’s a straightforward process of subtraction. You simply take all the money your business brought in (total revenue) and subtract all the allowable expenses it took to earn that money.

The number you’re left with is your assessable profit. This is the figure that the Inland Revenue Department (IRD) really cares about, and it’s the amount that the 8.25% and 16.5% rates will be applied to.

Let’s Meet “Artisan Threads,” Our E-commerce Startup Example

To make this crystal clear, let’s walk through the story of a fictional Hong Kong e-commerce startup, “Artisan Threads.” They’re in the business of selling handcrafted leather goods online to customers all over the world.

Last year was a good one for them, bringing in a total sales revenue of HK$1,800,000. That’s a solid start, but thankfully, it’s not the number they’ll be paying tax on. First, we need to account for everything they spent to make those sales happen.

What Can You Actually Deduct?

For an expense to be considered deductible, it has to pass a simple test: was it spent “in the production of chargeable profits”? In plain English, did you spend this money to help your business make money? If the answer is yes, it’s very likely deductible.

Here are some of the most common things a business like Artisan Threads can deduct:

- Cost of Goods Sold (COGS): The raw leather, buckles, and thread for their bags, plus the wages for the artisans who make them.

- Staff Salaries & MPF Contributions: The salary paid to their marketing assistant and even their own director’s salary.

- Rent for Office/Workshop: The monthly cost of their small workshop space in Kwun Tong.

- Marketing & Advertising: Their entire budget for social media ads, influencer collaborations, and Google Ads campaigns.

- Utilities & Internet: The electricity needed to run the workshop and their business broadband connection.

- Professional Fees: What they pay their accountant for bookkeeping and handling their tax filing.

- Software Subscriptions: All those recurring costs for their e-commerce platform, accounting software, and design tools.

These are the nuts and bolts of running the business. Each one is a cost that directly contributed to generating their sales, so each one can be subtracted from their total revenue.

It’s also crucial to remember that this whole process hinges on which profits were actually sourced in Hong Kong. If you’re dealing with international clients, it’s well worth looking into our guide on understanding Hong Kong’s offshore profits exemption claim to see if some of your income might not even be taxable here at all.

What Expenses Are a Definite No-Go?

Just as important is knowing what you can’t deduct. The IRD has clear rules on this, and getting it wrong is a common slip-up that can lead to headaches later. In short, personal expenses and certain major purchases (capital expenditures) are off-limits.

The golden rule is that an expense must be for the business, not for your personal life. Trying to claim a family holiday or your personal Octopus card top-ups is a classic compliance mistake.

For Artisan Threads, this means they absolutely cannot deduct:

- Private Expenses: The rent for the owner’s personal apartment or dinner out with the family.

- Capital Expenditure: The big, one-time purchase of a heavy-duty leather stitching machine. While they can’t deduct the full cost upfront, they can claim depreciation allowances on it over several years.

- Taxes Paid: The profits tax itself cannot be claimed as a business expense against profit.

- Domestic Travel: The owner’s MTR fares for their daily commute from home to the workshop are considered a private expense.

By keeping a clean line between business and personal spending, Artisan Threads ensures their books are clean and they only claim what they’re entitled to.

After adding up all their legitimate expenses—rent, salaries, marketing, materials, and so on—they land on a total of HK$1,100,000 in deductible expenses for the year.

Now for the simple part:

- Total Revenue: HK$1,800,000

- Deductible Expenses: HK$1,100,000

- Assessable Profit: HK$700,000

This HK$700,000 is the magic number. It’s their final, taxable profit that will be subject to Hong Kong’s tax rates. In the next section, we’ll plug this number into the two-tier system to see exactly what their final tax bill looks like.

Worked Examples of Hong Kong’s Two-Tier Tax System in Action

Okay, let’s move past the theory. The best way to truly grasp Hong Kong’s tax system is to see how the numbers play out in the real world. We’ll use a couple of common business scenarios to see exactly how the two-tier profits tax regime affects the final tax bill for SMEs.

But first, a quick reminder of the fundamental calculation. Your tax isn’t based on your total sales; it’s calculated on your assessable profits.

It’s a crucial distinction. Only after you’ve deducted all your legitimate, tax-deductible business expenses do you arrive at the figure the Inland Revenue Department (IRD) is interested in.

A Startup’s First Profitable Year

Let’s imagine a brand new tech startup, “Innovate AI.” They’ve had a fantastic first year and managed to generate an assessable profit of HK$1,500,000.

Since their profit is comfortably under the HK$2 million threshold, the calculation is wonderfully straightforward. The entire amount is taxed at the lower 8.25% rate.

- Tax Calculation: HK$1,500,000 x 8.25%

- Total Tax Payable: HK$123,750

For Innovate AI, their effective tax rate is a flat 8.25%. This is a perfect example of how the two-tier system gives new businesses a significant leg up, leaving them with more cash to reinvest into growth.

A Growing Consultancy Firm

Now, let’s consider “Apex Strategy,” a consulting firm that’s been around for a few years. They’re more established, and this year their assessable profit hit HK$3,000,000. This is where the two-tier calculation really comes alive.

Here’s how their profit is broken down for tax purposes:

- The first HK$2,000,000 is taxed at the concessionary rate of 8.25%.

- The remaining HK$1,000,000 (the amount over HK$2M) is taxed at the standard rate of 16.5%.

This is a key point that often trips people up. The higher rate doesn’t apply to your entire profit once you cross the threshold. You still get the benefit of the lower rate on that first HK$2 million.

To illustrate, let’s break down the maths for Apex Strategy in a simple table.

Worked Example of a Hong Kong Tax Calculation

| Calculation Step | Amount (HK$) | Tax Calculation |

|---|---|---|

| Assessable Profits | 3,000,000 | |

| Tax on First HK$2M | 2,000,000 | 2,000,000 x 8.25% = 165,000 |

| Tax on Remaining Profit | 1,000,000 | 1,000,000 x 16.5% = 165,000 |

| Total Tax Payable | 165,000 + 165,000 = 330,000 |

The firm’s final tax bill is HK$330,000.

If you calculate their effective tax rate (HK$330,000 ÷ HK$3,000,000), it comes out to just 11%. That’s a huge difference from the headline 16.5% rate and clearly shows the powerful “blended rate” effect of the system.

Getting these calculations spot-on is critical, which is why many growing businesses choose to work with professional accounting services in Hong Kong to ensure they’re not just compliant, but also tax-efficient.

Why Is Hong Kong Still a Go-To for Global Entrepreneurs?

Let’s zoom out for a moment. Beyond the numbers and calculations, what’s the big picture? Why do founders from every corner of the world still set their sights on Hong Kong? The attractive company tax rate Hong Kong offers is a huge draw, but it’s not the whole story. The city’s reputation as a world-class business hub is built on a foundation of simplicity, stability, and one absolute game-changing rule.

That rule is the territorial source principle. It’s a beautifully straightforward concept with massive implications for anyone doing business internationally.

Imagine your company has two main income streams. One comes from local clients right here in Hong Kong, and the other is from a big project you just wrapped up for a customer in London. Under Hong Kong’s territorial system, the Inland Revenue Department (IRD) only really cares about the profits you made from your Hong Kong activities. The profit from that London project? It’s considered ‘offshore sourced’. As long as you’ve set things up correctly, it generally isn’t touched by Hong Kong profits tax.

This isn’t some clever loophole; it’s the fundamental design of the tax system. Hong Kong taxes you on where your profits are generated, not just where your company is based. This is the secret sauce that makes the city a true hub for international trade, not just another low-tax jurisdiction.

The Unspoken Advantage: Stability and Predictability

For any business owner, surprises are rarely a good thing—especially when they come from the taxman. This is where Hong Kong truly shines. Its tax laws are famously consistent and transparent, giving you a level of predictability that’s hard to come by in other major financial centres.

You can see this stability in the headline tax rate. The standard profits tax rate for corporations has been a rock-solid 16.5% since the 2008/09 financial year. This isn’t just a local claim; it’s a fact confirmed by global data trackers. It makes long-term financial planning much easier when you know the goalposts aren’t constantly shifting. For those who love data, you can see Hong Kong’s tax rate history on TradingView for yourself.

How Hong Kong Stacks Up Globally

When you place Hong Kong’s system next to other popular business hubs, the benefits really come into focus.

- Versus the UK: While London is a financial titan, its corporate tax system is a different beast entirely. It’s far more complex, subject to frequent political shifts, and its worldwide taxation model can create a serious compliance headache for international businesses.

- Versus Singapore: Singapore is another highly competitive, low-tax option. However, its system has more intricate rules around bringing foreign-sourced income into the country and a Goods and Services Tax (GST) that adds another layer of admin.

- Versus the UAE: Jurisdictions like the UAE are also major players in the low-tax world. To get a full picture of international tax strategy, it’s worth looking into options like UAE offshore company formation for tax benefits to see how different structures can serve global entrepreneurs.

Hong Kong’s approach cuts through a lot of that noise. There’s no capital gains tax. No tax on dividends paid out by local companies. No VAT or sales tax. This simplicity doesn’t just mean a lower tax bill; it slashes your administrative burden, freeing you up to focus on what you’re actually good at—building your business. This powerful mix of a low company tax rate Hong Kong and a clear, predictable system is what cements its status as a premier global destination.

Frequently Asked Questions on Hong Kong Company Tax

After covering the rates, calculations, and the big-picture strategy, you’re bound to have some practical questions. Let’s tackle some of the most common queries we get from entrepreneurs on the ground.

Think of this as the final check-in before you dive in, making sure you’re not just informed but truly confident about your next moves.

What Is a Year of Assessment in Hong Kong?

You’ll see “year of assessment” mentioned all over your tax paperwork. It’s simply the government’s official tax year, which runs from 1 April to 31 March. So, when the IRD refers to the 2024/25 year of assessment, they mean the period from 1 April 2024 to 31 March 2025.

But here’s the key thing: your company’s own financial year-end doesn’t have to match this. You’re free to choose a date that makes sense for your business, like 31 December. The IRD is flexible; they’ll simply assess the profits from your company’s accounting period that falls within that specific year of assessment.

Do I Need to Hire an Auditor?

For pretty much any limited company in Hong Kong, the answer is a resounding yes. When you file your Profits Tax Return (Form BIR51), you are legally required to submit it with a full set of audited financial statements signed off by a Hong Kong-registered Certified Public Accountant (CPA).

This isn’t just a box-ticking exercise. An audit lends serious credibility to your financials, which is gold when you’re talking to banks, investors, or potential partners.

Don’t just see auditing as a mandatory cost. Think of it as a professional health check for your business. It verifies your records and can often uncover financial leaks or inefficiencies you’d otherwise miss.

When Is My First Tax Return Due?

This is a big point of anxiety for new founders, but the timeline is actually quite logical. The IRD won’t send you a tax return the day after you incorporate. Instead, you can expect to receive your first Profits Tax Return about 18 months after your incorporation date.

Why the long runway? It gives you plenty of time to get through your first full business cycle, prepare your financial statements, and have them properly audited. This 18-month window is designed to ensure you’re fully prepared for your first filing. After that, you’ll fall into a standard annual filing rhythm.

What Happens If My Company Makes a Loss?

Let’s be realistic—not every year is a banner year, especially when you’re just starting out. The good news is that Hong Kong’s tax system accounts for this reality. If your company takes a loss, you can carry that loss forward indefinitely to offset profits in future years.

For instance, say you post a loss of HK$100,000 in year one but make a profit of HK$300,000 in year two. You can use that earlier loss to shrink your taxable profit in the second year down to HK$200,000. It’s a powerful feature that supports businesses through the lean times, significantly easing the pressure during those critical growth stages.

Can I Claim the Two-Tier Rates Every Year?

Yes, absolutely—as long as you continue to qualify. The two-tier profits tax regime, with its lower 8.25% rate on the first HK$2 million of profit, isn’t a one-time welcome bonus. It’s a permanent feature of the tax system that a qualifying company can take advantage of every single year.

The one major rule to keep in mind is the ‘connected entity’ clause we discussed earlier. If you have a group of related companies, only one of them can be nominated to use the two-tier rates for any given tax year. This makes strategic planning essential if you run multiple businesses, as you’ll want to apply the benefit where it delivers the most impact.

Conclusion

Getting a handle on the company tax rate Hong Kong offers is just one piece of your global expansion puzzle. At Lion Business Consultancy Limited, we build the entire financial framework your business needs—from compliant low-tax structures to secure international banking. We act as your private financial manager, ensuring every move you make is secure, strategic, and set up for long-term success.