Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

Yes, you absolutely can open a Singapore bank account as a foreigner, and the process is probably more straightforward than you imagine. If you're over 18, have your passport, and hold a valid pass like an Employment Pass (EP) or Student Pass, you're already in a great position with Singapore's top banks.

Why Singapore is a Top Choice for Foreign Banking

When savvy entrepreneurs and professionals scan the globe for a solid banking hub in Asia, their eyes almost always land on Singapore. This isn't just a coincidence; it's a strategic move rooted in the city-state's unshakable reputation as a secure, efficient, and tech-forward financial powerhouse.

Let’s put this into a real-world context. Imagine you're an entrepreneur expanding your e-commerce business from Europe into Southeast Asia. You need a banking partner that speaks the language of international trade—one that handles multiple currencies without a fuss, provides a world-class digital platform, and offers a safe haven for your capital. This is precisely where Singaporean banks like DBS, OCBC, and UOB excel. They've built their services for a global clientele, so they inherently understand your needs.

This isn’t just a feeling; the numbers tell a story of a deeply ingrained banking culture. Back in 2020, the country had an incredible 2,405 bank accounts per 1,000 adults. This density sparks a competitive fire, which ultimately benefits you with superior service and constant innovation.

The Core Appeal for Entrepreneurs and Expats

So, what’s the secret sauce? What really makes Singapore’s banking system a magnet for global talent and international businesses? It boils down to a few powerful fundamentals.

- Political and Economic Stability: In a world of financial turbulence, Singapore is an anchor. Its stability provides a safe harbour for your funds, a massive draw for anyone operating in volatile global markets.

- A Genuinely Pro-Business Environment: The government doesn’t just talk the talk. The regulations are actively designed to support international trade and investment, creating a smooth runway for your business.

- Cutting-Edge Technology: Singapore's banks were pioneers in digital banking. You get sophisticated mobile apps, seamless online transfers, and innovative financial tools that make managing money from anywhere in the world simple and secure.

- True Global Connectivity: A Singapore bank account is more than a place to park cash; it's your gateway to the ASEAN region and the global economy, thanks to the nation's strategic location and powerful trade links.

It’s this powerful combination that transforms banking here from a simple necessity into a real strategic advantage. You’re not just ticking a box; you’re plugging into one of the world's most dynamic financial ecosystems.

Setting the Right Expectations

While the path is clear, you need to walk it prepared. Singaporean banks are incredibly diligent with their compliance checks to combat financial crime, so your paperwork has to be flawless. Treat it like a crucial business pitch—every detail counts.

For a foreigner, opening a bank account in Singapore is less about facing impossible hurdles and more about methodically checking the right boxes. The system is built to welcome legitimate foreign investors and professionals, but it has zero tolerance for ambiguity or incomplete information.

Here’s a quick overview of what you’ll generally need to get started.

Eligibility and Document Checklist at a Glance

This table provides a snapshot of the typical requirements. Remember, specifics can vary slightly between banks, so it's always smart to double-check with your chosen institution before you start.

| Requirement Category | Details and Key Documents |

|---|---|

| Personal Identification | A valid passport is non-negotiable. Some banks may also request a national ID card from your home country. |

| Proof of Residency/Status | You'll need a valid Singaporean pass, such as an Employment Pass (EP), S Pass, Student Pass, or Long-Term Visit Pass (LTVP). |

| Proof of Address | This can be a recent utility bill, a phone bill, or a tenancy agreement. The document must be in your name and show your Singaporean residential address. |

| Proof of Employment/Study | An official letter from your employer or educational institution in Singapore is often required. It should confirm your position or enrolment. |

| Initial Deposit | Most accounts require a minimum initial deposit, which can range from S$500 to S$3,000, depending on the bank and account type. |

Having these documents lined up before you begin the application will make the entire journey significantly smoother.

Of course, a bank account is just one piece of your financial setup. As a foreign resident, you'll also want to sort out health coverage. You can explore various Singapore Travel Health Insurance options to ensure you're fully protected.

Understanding why Singapore is such a powerhouse helps you tackle the how. In the next sections, we’ll dive into the nitty-gritty of the documents and the step-by-step process.

Getting Your Paperwork in Order

Let's be blunt: getting your documents right isn't just a box-ticking exercise. It is the single most critical step in the entire process. When you want to open a Singapore bank account for a foreigner, your success hinges on having every piece of paper perfectly in order.

Think of it this way: you're not just filling out a form; you're building a case. You need to prove who you are, why you're here, and that you have legitimate ties to Singapore. The good news? If you understand what the bank is looking for, you can make it incredibly easy for them to say yes.

Banks aren’t trying to make your life difficult. They are bound by strict local regulations like Know Your Customer (KYC) and Anti-Money Laundering (AML) rules. Your mission is to give them a file so clean and complete that approving it is the only logical next step.

The Core Essentials: Your Passport and Pass

These two documents are the bedrock of your application. They are non-negotiable, and they'll be the first things the bank scrutinizes. Get these wrong, and nothing else matters.

-

Your Passport: You'll need your original, valid international passport. A photocopy simply won't do for in-person verification. A pro tip: make sure it has at least six months of validity remaining. While not always an official rule, it's a common internal policy that prevents future headaches.

-

Your Singaporean Pass: This is your proof of status, the document that shows you have a legitimate reason to be in the country. This will be your Employment Pass (EP), S Pass, Student Pass, or perhaps a Dependant’s Pass. If you've just landed and are waiting for the physical card, your In-Principle Approval (IPA) letter is usually accepted as a temporary substitute.

One of the most common hiccups I see is a simple name mismatch. If your passport says "Jonathan Michael Smith" but your IPA letter just has "Jonathan Smith," that tiny difference can cause frustrating delays. Always ensure your full, legal name is identical across every single document.

Proof of Address: Where Most People Get Stuck

This is, without a doubt, the biggest hurdle for newcomers. The bank needs an official document tying you to a physical residential address in Singapore. This is for mailing important documents and, more crucially, for verifying your presence in the country.

So, you've just arrived on an EP and you're in a serviced apartment while you look for a permanent place. What can you possibly use? Here are the documents banks look for and how they view them:

- Tenancy Agreement: This is the gold standard. But remember, it must be officially stamped by the Inland Revenue Authority of Singapore (IRAS) to be considered valid.

- Utility or Telco Bill: A recent bill (less than three months old) from a provider like SP Group, Singtel, or StarHub is perfect proof.

- A Letter from Your Employer: This is a fantastic option if you're new in town. Many companies will happily provide a letter on official letterhead confirming your employment and stating your current residential address. This is a very common and widely accepted solution.

Insider Tip: Pay close attention to dates. Don’t try to submit a utility bill that’s a few days over the three-month mark. A bank’s compliance system is black and white—it’s either valid or it isn't. A bill that’s 95 days old will likely get your application flagged, forcing you to start over.

Matching Your Documents to Your Situation

The exact combination of documents you'll need depends on your story. The bank is trying to build a clear picture of you, so your paperwork needs to tell a consistent one.

Let's walk through a couple of real-world scenarios.

Scenario 1: The International Student

A student on a Student Pass will need their passport and the pass itself. For proof of address, a letter from their university’s housing office confirming their dorm room is usually sufficient. They will also need to bring their letter of admission from the school.

Scenario 2: The Dependant’s Pass Holder

Imagine a spouse on a Dependant’s Pass who isn't working. They'll need their passport and pass. For proof of address, they can often use a utility bill or tenancy agreement that's in their partner's name. The key is to also provide a copy of their partner's EP and their marriage certificate to link everything together.

The secret is to think one step ahead. Before you walk into the bank, look at your documents and ask, "Does this package of paperwork clearly and officially prove everything they need to know about me?" And if any of your documents aren't in English, you absolutely must have them translated by a certified professional. A DIY translation will be rejected on the spot.

Taking the time to prepare these documents with care is the single best investment you can make to ensure your application sails through without a hitch.

Navigating the Bank Account Opening Process

Okay, you’ve assembled your documents like a pro. Now for the exciting part: turning that neat stack of paperwork into an active Singapore bank account. This isn't just about filling out a form; it's about making smart choices that will simplify your financial life here.

Think of this as your on-the-ground guide. I’ll walk you through the key steps you'll face when you open a Singapore bank account for a foreigner, highlighting the practical details that truly matter. We'll cover everything from picking the right bank to what happens after you hit "submit."

Choosing Your Banking Partner

First things first, you need to decide which bank to partner with. Singapore offers a fantastic mix of local giants and global powerhouses, which gives you a real advantage.

The local "Big Three"—DBS, OCBC, and UOB—are ubiquitous. Their ATM networks are vast, and their digital banking platforms are tailor-made for life in Singapore. They truly get the local market.

Then you have the global players like HSBC, Standard Chartered, and Citibank. If you're constantly transferring money between, say, London and Singapore, their established international networks can often mean smoother, more affordable transfers.

The best bank for you really boils down to your unique needs.

- For local living: If you’re here on an Employment Pass and just need an account for your salary and daily expenses, a local bank is usually the most straightforward and convenient choice.

- For global business: An entrepreneur juggling invoices from clients in different currencies would likely find more value in a multi-currency account offered by an international bank.

This is a key decision, so take a moment to weigh your options. It will shape your entire banking experience in the country.

In-Person vs Online Applications

Once you’ve picked a bank, it’s time to apply. Thankfully, you have options. You can either go the traditional route and visit a branch or handle it all online.

Walking into a branch is still a solid choice. You get to sit down with a bank officer, hand over your original documents, and know immediately if everything is in order. That face-to-face reassurance can be a huge comfort, especially when you're new to the country.

But let's be honest, online applications are a game-changer. Most banks now have slick, user-friendly portals that let you open a Singapore bank account for a foreigner from your laptop. You can simply upload your documents and get on with your day. Our detailed guide on how to open a bank account online in Singapore dives deeper into this process.

A Practical Insight: Just a heads-up, even if you apply online, don't be surprised if the bank asks for a quick video call or a brief visit to a branch for final verification. It's a standard security check and a crucial part of their due diligence.

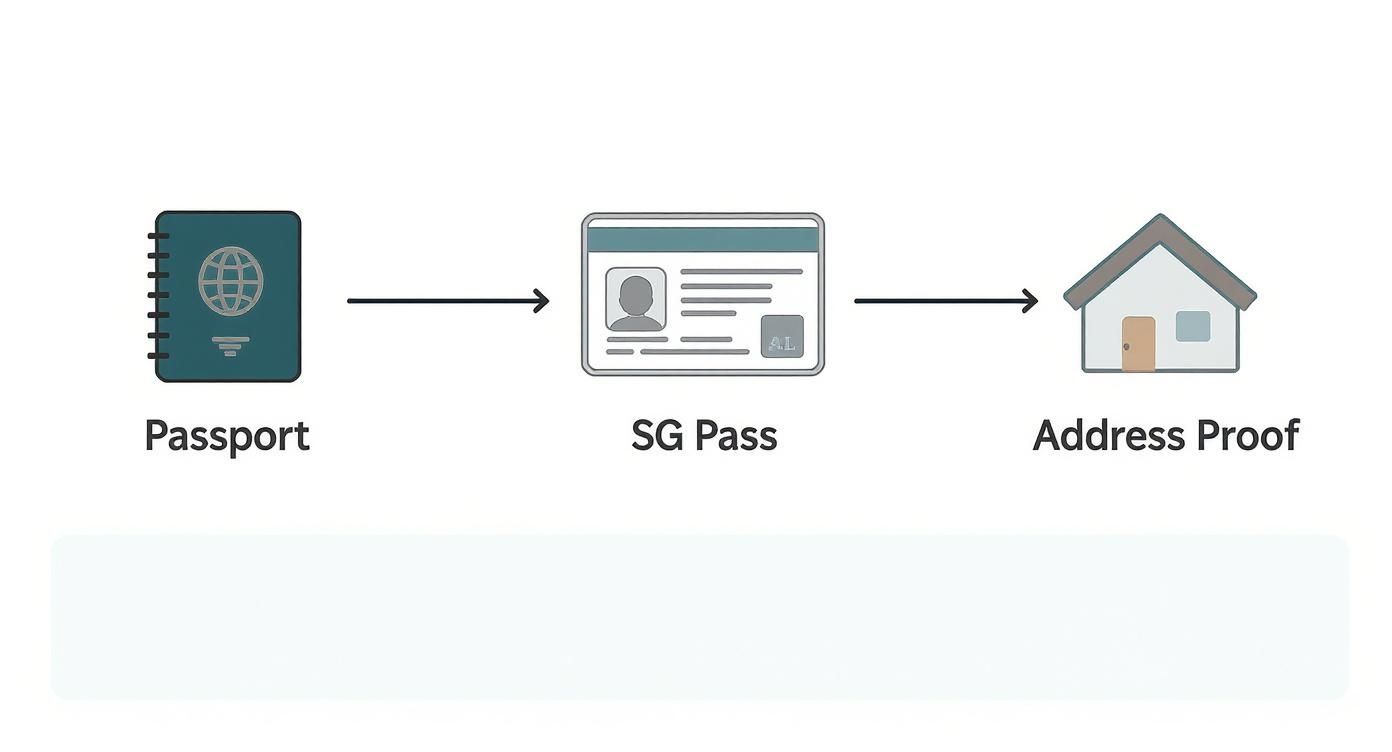

While requirements can vary slightly, all foreigners go through a similar verification process. For a quick visual breakdown, this infographic cuts through the noise and shows you the essential documents you’ll need.

As you can see, it really boils down to three non-negotiables: your passport, a valid Singaporean pass (like an EP or S Pass), and proof of where you live.

The Final Stretch: Approval and Activation

After you've submitted everything, it’s a bit of a waiting game. The bank’s compliance team needs to conduct their checks, which can take anywhere from a few business days to a couple of weeks. It all depends on their workload and the complexity of your application.

Once you get the green light, you'll receive a notification by email or SMS. The final step is getting the account up and running. Most banks don't charge an opening fee, but you will need to make an initial deposit to activate it. This amount varies but is often around S$1,000.

As soon as that deposit clears, you’ll get your account number, debit card, and instructions for setting up your online banking. And just like that, you’re all set. Your new Singapore bank account is officially live and ready for business.

Choosing the Right Bank and Account Type

Alright, your documents are in order. Now comes the strategic decision: which bank earns your business? This isn't just about picking a familiar logo. The bank you choose becomes your financial partner in Singapore, influencing everything from daily transaction fees to how easily you can send money back home.

Singapore’s banking landscape is neatly divided between local powerhouses and global giants. The "Big Three" local banks—DBS, OCBC, and UOB—are everywhere. They boast the most extensive ATM networks, and their apps are intuitively designed for life in the city-state, making them a fantastic, no-fuss choice for everyday banking.

On the other side, you have international players like HSBC, Citibank, and Standard Chartered. Their true strength is their global connectivity. If you're frequently moving funds between Singapore and your home country, their internal networks often translate to lower fees and a smoother experience. The key is to look beyond the brand and focus on the features that will genuinely make your life easier.

Local Titans Versus Global Players

So, local or international? The right choice really depends on your mission. If you're an employee on an Employment Pass getting paid in SGD, the sheer convenience of a local bank is hard to beat.

But if you're a consultant invoicing clients in both USD and EUR, an international bank's multi-currency features will be a game-changer.

Before you commit, ask yourself these practical questions:

- How much will it cost to send money home? International banks often offer better rates for transfers within their own network.

- Can I hold different currencies? For anyone earning foreign income, an account that lets you hold and transact in multiple currencies without forcing a conversion is a must-have.

- Is the mobile app actually good? A clunky, frustrating app can make managing your finances a real chore. Try to find a demo or reviews online.

- How easy is it for a foreigner to open an account? It's worth checking expat forums for recent feedback. Some banks are known for being more welcoming than others.

The great news is you're spoiled for choice. Singapore's banking sector is built to serve a global clientele. As of April 2025, the country hosts 30 foreign banks with full-service licences and 97 wholesale banks, creating a highly competitive market. This competition is why features like multi-currency accounts are now standard, not a luxury.

Comparing Top Singapore Banks for Foreigners

To give you a clearer picture, let's compare some of the most popular options side-by-side. This isn't an exhaustive list, but it covers the main players and what they're generally known for.

| Bank Name | Best For | Key Features for Foreigners | Typical Initial Deposit |

|---|---|---|---|

| DBS Bank | Everyday convenience & local integration | Huge ATM network, user-friendly mobile app (DBS digibank), often lower initial deposit requirements. | S$0 – S$3,000 |

| OCBC Bank | All-round personal banking & ASEAN connectivity | Strong digital banking, comprehensive services including investments, good for regional transfers. | S$1,000 |

| UOB Bank | Regional business & multi-currency options | Strong focus on Southeast Asia, excellent multi-currency accounts, good for business owners. | S$1,000 |

| Citibank | Global citizens & frequent travellers | Seamless international transfers (Citibank Global Transfer), multi-currency access, global support. | S$5,000 – S$15,000 |

| HSBC | Expats needing global banking connectivity | Premier and Advance accounts offer global benefits, easy transfers between HSBC accounts worldwide. | S$0 (with conditions) – S$15,000 |

| Standard Chartered | Digital banking & multi-currency flexibility | Bonus$aver account is popular, strong multi-currency features, often runs promotions for new clients. | S$0 – S$5,000 |

Ultimately, the "best" bank is subjective. A digital nomad's needs are vastly different from an executive's on a long-term assignment. Use this table as a starting point to narrow down your search.

Matching the Account to Your Mission

Choosing a bank is only half the battle; picking the right type of account is just as crucial. A mismatch here could leave you paying needless fees or struggling with limitations. Before you open a Singapore bank account for a foreigner, you need to understand the main options.

Let's break them down with some real-world context.

- Savings Account: This is your daily driver. It's where your salary lands, where you keep your rainy-day fund, and it earns a little bit of interest. Think of it as your financial home base.

- Current Account (Chequing): Designed for a higher volume of transactions, this is the go-to for business owners or anyone who needs to issue cheques and make frequent, large payments.

- Multi-Currency Account (MCA): For any global professional, this is the most valuable player. An MCA lets you hold different currencies—like SGD, USD, EUR, and GBP—in separate wallets under a single account.

Real-World Scenario: Imagine you're a freelance graphic designer in Singapore with clients in the US and Germany. With a multi-currency account, your American client pays in USD, and your German client pays in EUR. The money sits in its original currency wallet. You only convert it to SGD when you need to, or when the exchange rate is in your favour. Over a year, this simple strategy can save you a small fortune in conversion fees.

This strategic thinking is even more critical for businesses. Our guide on how to open a Singapore business bank account dives deeper into these specifics, helping you find a setup that truly supports your company's growth. By putting a little thought into both the bank and the account type now, you'll set yourself up for a much smoother financial life in Singapore.

Navigating Common Roadblocks: What to Do When You Hit a Snag

Even with flawless preparation, opening a bank account in Singapore as a foreigner can sometimes throw you a curveball. These aren't usually show-stoppers, but they can be frustrating bumps in the road. The trick is to anticipate these common issues and have a solution ready before they even appear.

Think of it like navigating a new city. You know your destination, but you might hit an unexpected road closure. Having a map with a few detours marked makes all the difference. This is your map, drawn from the real-world experiences of countless expats who've been through this exact process.

We'll walk through the most common challenges, from the classic "proof of address" dilemma to mysterious application delays, and give you practical advice to keep things moving.

The Proof of Address Predicament

This is, without a doubt, the number one hurdle for newcomers. You’ve just landed, you’re in temporary housing, and the bank wants a utility bill with your name on it. It’s a classic chicken-and-egg problem. So, what’s the workaround?

Fortunately, Singapore’s banks are familiar with this scenario and have a list of alternative documents they’ll accept. You just need to know what to offer.

- A Letter from Your Employer: This is your golden ticket. Ask your HR department for a formal letter on company letterhead. It should confirm your employment and, crucially, state your current residential address. This is widely accepted.

- Your In-Principle Approval (IPA) Letter: The IPA for your Employment Pass is another strong document. While it often lists your employer's address, some banks will accept it as a temporary measure, especially when presented alongside an employer's letter.

- A Stamped Tenancy Agreement: If you've already secured a long-term rental, this is perfect. The key word here is stamped. An unstamped rental agreement carries very little weight, so ensure it has been officially stamped by the Inland Revenue Authority of Singapore (IRAS).

Another small hiccup can occur during online applications if you don't have a local Singapore number yet for two-factor authentication. In these cases, using temporary SMS verification services can be a practical workaround to get through the initial setup hurdles.

Decoding Application Delays

So, you’ve submitted a perfect application package and then… silence. A week passes, maybe two. It's easy to get anxious, but a delay rarely signals rejection. More often than not, it’s just a sign of a backlog in the bank's compliance department or a minor query about one of your documents.

An Expert's Tip: Resist the urge to call the bank every day. Give them the full timeline they quoted you. If you still haven’t heard anything after that, send a single, polite follow-up email with your application reference number. A professional follow-up shows you’re organised, not anxious.

Often, the bottleneck is something as simple as a slight name variation between documents or a scanned passport page that isn't perfectly clear. By double-checking every detail before you submit, you drastically reduce the chance of your application getting stuck in the review queue.

Keeping an Eye on Fees and Minimums

Another area that can catch people by surprise is the web of account fees. Most standard savings accounts in Singapore require you to maintain a minimum average daily balance, typically between S$1,000 and S$3,000. If your balance dips below this threshold, you’ll be hit with a "fall-below fee" of around S$2 to S$5 per month.

It might not sound like much, but it’s an annoying charge that’s easy to avoid with a bit of proactive management.

- Read the Fine Print: Before you sign anything, ask for the specific minimum balance and the exact fall-below fee. Get the details in writing.

- Set Up Alerts: As soon as your mobile banking app is running, dive into the settings and turn on low-balance alerts. This tiny step can save you real money.

- Explore Digital Banks: The newer digital-only banks are shaking things up. Many offer accounts with no minimum balance requirements at all, making them a fantastic option when you're just getting started.

By anticipating these potential roadblocks and preparing your solutions ahead of time, you can turn a potentially stressful process into a simple, straightforward task.

Your Top Singapore Banking Questions, Answered

As you gear up to open your Singapore bank account, a few practical questions are bound to pop into your head. I've guided countless entrepreneurs and expats through this exact process, and I've found that the same key questions always come up just before they take the plunge.

Getting these details straight from the start will make the whole experience smoother and far less stressful. Let’s tackle the most common queries I hear.

Can I Open a Singapore Bank Account from Overseas?

This is the big one. The honest answer is: it’s very difficult for most people, but not entirely impossible for a select few. The vast majority of Singapore's banks require you to be physically present. This isn't just bureaucratic red tape; it's a core part of their strict "Know Your Customer" (KYC) regulations designed to verify your identity and prevent financial crime.

However, there are exceptions. If you're exploring premier or private banking services with global names like HSBC or Citibank, they can sometimes facilitate remote account opening for high-net-worth clients. If this applies to you, your best first step is to contact their international banking team in your home country.

For most professionals and business owners, though, the tried-and-true path is to handle the application once you’ve arrived in Singapore with your valid pass in hand.

Resident vs. Non-Resident Accounts: What’s the Difference?

Understanding this distinction is absolutely crucial. It impacts your eligibility, the features you receive, and even the fees you pay. It all comes down to your legal residency status in Singapore.

-

Resident Account: This is the standard account for anyone holding a long-term pass, such as an Employment Pass, S Pass, or Student Pass. For banking purposes, you are considered a resident, which unlocks the full range of banking services, typically on more favourable terms.

-

Non-Resident Account: This category is for individuals who do not live in Singapore but need banking facilities there, often for investment or international business purposes. Be prepared for a much higher bar. Banks are naturally more cautious due to anti-money laundering regulations, so expect higher minimum deposits, greater scrutiny, and potentially more fees.

Think of it this way: a resident account is for living and working in Singapore. A non-resident account is a specialised financial tool for managing assets from abroad, and banks treat it with a much higher level of diligence.

Do I Need to Keep a Minimum Balance?

Yes, in most cases, you do. The "minimum average daily balance" is a standard feature for most savings accounts in Singapore. You'll typically find this requirement set somewhere between S$1,000 and S$3,000.

What happens if your average balance for the month dips below that? The bank will charge a "fall-below fee." It's not a huge amount—usually around S$2 to S$7—but it's an unnecessary expense you can easily avoid.

My advice is to always read the fee schedule carefully when choosing an account. Some of the newer digital banks or special promotional accounts might waive this requirement, which is a fantastic perk when you're just getting your finances established. A little homework here can save you from those small, annoying fees that add up over time.

Conclusion

Navigating the complexities of international banking is about more than just opening an account; it's about building a secure and efficient financial foundation for your global ambitions. At Lion Business Consultancy Limited, we specialise in creating these frameworks for entrepreneurs and SMEs. If you're ready for a strategic partner who can guide you through every step, frm secure banking to tax-efficient corporate structures, we're here to help.