Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

Welcome to your guide for navigating the Securities and Futures Commission (SFC) licensing process in Hong Kong. Think of this as your practical SFC licensing handbook—a resource designed to translate complex regulatory requirements into clear, manageable steps for entrepreneurs like you.

Your Introduction to SFC Licensing in Hong Kong

For any business, especially international SMEs, looking to tap into Hong Kong’s dynamic financial market, understanding the SFC framework isn’t just about compliance. It’s the very foundation of your credibility and the key that unlocks real growth.

The SFC is Hong Kong’s independent financial regulator, tasked with a clear mission: to protect investors and uphold the integrity of the city’s markets. Obtaining an SFC licence is a powerful signal to clients, partners, and investors that your firm meets these high standards and is a serious, reputable player.

This guide is built to cut through the dense legal jargon and offer a straightforward, consultative perspective. Imagine your business is a skyscraper. The SFC licence is your non-negotiable building permit and structural blueprint. You simply can’t break ground without it. In the same way, your financial services firm cannot legally operate or scale in Hong Kong without the right licence.

Why This Handbook Matters To You

Securing a licence is far more than just paperwork. It demands a thorough understanding of your own business model and how it maps onto the SFC’s regulatory structure. We’ve organised this handbook to guide you through exactly that.

Here’s what you can expect to learn:

- Identify the Right Licence: We’ll break down the various licence types to help you pinpoint precisely which regulated activities your business conducts.

- Meet the ‘Fit and Proper’ Test: You’ll discover what the SFC looks for in applicants—from financial stability and competence to individual integrity.

- Prepare a Solid Application: We will walk you through the essential documents and critical preparations needed to ensure your application is robust and complete.

The SFC’s primary goal is to ensure that only qualified, competent, and reputable firms and individuals operate in its markets. Your greatest advantage is a well-prepared application that clearly demonstrates your firm’s commitment to these standards from day one.

Ultimately, this guide serves as your strategic partner. By building a strong knowledge base right from the start, you can approach the SFC licensing process with clarity and confidence, ready to seize the opportunities available in one of Asia’s most important financial centres.

Decoding the 10 Types of SFC Regulated Activities

Getting your SFC licence application right starts with one crucial step: identifying the correct category for your business. Think of it like this—you wouldn’t start building a skyscraper with the blueprints for a bungalow. A mismatch at this stage creates foundational problems that can derail your entire application, costing you both time and money.

The SFC framework is built around ten distinct Regulated Activities (RAs), each covering a specific slice of the financial markets. Your business model must slot neatly into one or more of these classifications. For instance, a wealth manager, a securities broker, and a corporate finance advisor all deal with financial products, but each needs a completely different licence to operate legally in Hong Kong. Getting this right from the outset is non-negotiable.

To help you quickly pinpoint where your business fits, here’s a quick-reference table outlining all ten RA types and their common applications.

Quick Reference Guide to SFC Regulated Activities (RA Types 1-10)

| RA Type | Activity Description | Common Business Application |

|---|---|---|

| Type 1 | Dealing in Securities | Securities brokerage, stock trading platforms, market makers. |

| Type 2 | Dealing in Futures Contracts | Futures and options brokerage. |

| Type 3 | Leveraged Foreign Exchange Trading | Retail forex trading platforms. |

| Type 4 | Advising on Securities | Investment research firms, financial advisors providing stock tips. |

| Type 5 | Advising on Futures Contracts | Advising clients on futures and options strategies. |

| Type 6 | Advising on Corporate Finance | IPO sponsors, M&A advisory, corporate restructuring advisors. |

| Type 7 | Providing Automated Trading Services | Operating dark pools or other automated trading platforms. |

| Type 8 | Securities Margin Financing | Providing margin loans to clients for stock purchases. |

| Type 10 | Providing Credit Rating Services | Agencies that issue credit ratings for companies or securities. |

This table serves as a starting point. Now, let’s dig into the most common licences that international SMEs and entrepreneurs typically require when they set up shop in Hong Kong.

A Closer Look at the Most Common Licence Types

While there are ten RAs, most new entrants to the Hong Kong market find their activities fall into one of four main categories. Here’s how they work in the real world:

- Type 1: Dealing in Securities: This is the bread and butter for any firm that executes buy or sell orders in securities for its clients. When looking at the various SFC regulated activities, firms providing brokerage services fall squarely under Type 1. A classic example is a stock brokerage helping retail investors trade on the exchange.

- Type 4: Advising on Securities: If your firm provides investment advice, recommendations, or research reports on specific securities, this is your category. Imagine a financial analyst firm that publishes “buy,” “sell,” or “hold” ratings on listed companies—that’s a Type 4 activity.

- Type 6: Advising on Corporate Finance: This licence is for firms that guide companies through major corporate actions like mergers, acquisitions, takeovers, or fundraising. A boutique advisory firm helping a startup navigate its IPO on the Hong Kong Stock Exchange is a perfect example of a Type 6 licence holder.

- Type 9: Asset Management: If you manage investment portfolios of securities or futures contracts for clients on a discretionary basis, you’ll need a Type 9 licence. This is the domain of fund management companies, from large hedge funds to firms managing private wealth portfolios.

Capital and Ongoing Obligations

Securing a licence is just the beginning. Each RA type comes with its own set of financial and compliance hurdles, all laid out in the official SFC licensing handbook. These aren’t just suggestions; they are strict rules.

For instance, capital requirements vary massively between licences. A Type 1 licence might require anywhere from HKD 500,000 to HKD 10 million in paid-up capital, depending on the scope of business. In contrast, a Type 9 licence for a firm that doesn’t hold client assets has a much lower bar, needing just HKD 100,000 in liquid capital plus a buffer.

Beyond the initial capital, licensed firms have ongoing responsibilities. You’ll need to submit audited financials, ensure your team completes continuous professional training, and adhere to a host of other compliance duties. These rules underscore Hong Kong’s commitment to maintaining a robust and trustworthy market.

Key Takeaway: Correctly identifying your Regulated Activity isn’t just a box-ticking exercise; it’s the single most important decision you’ll make at the start. A mistake here is an application-killer that will waste significant time and resources.

By carefully matching your business operations to the specific definitions of each RA, you lay a solid foundation for a smooth and successful licensing process. It’s about making a clear, informed, and strategic decision from day one.

Meeting the Crucial Fit and Proper Criteria

Getting the right SFC licence is only half the battle. Your firm, its directors, and key personnel must also pass the SFC’s fundamental gatekeeper test: the fit and proper criteria. This isn’t just about ticking boxes; it’s a thorough, in-depth assessment designed to ensure only competent, reputable, and financially stable firms operate in Hong Kong’s financial markets.

Think of it as the SFC performing its own deep-dive due diligence on you and your team. The entire evaluation, as detailed in the SFC licensing handbook, is built on three core pillars. Your application needs to clearly demonstrate strength in each area to get the green light. Any weakness can lead to long delays or even an outright rejection.

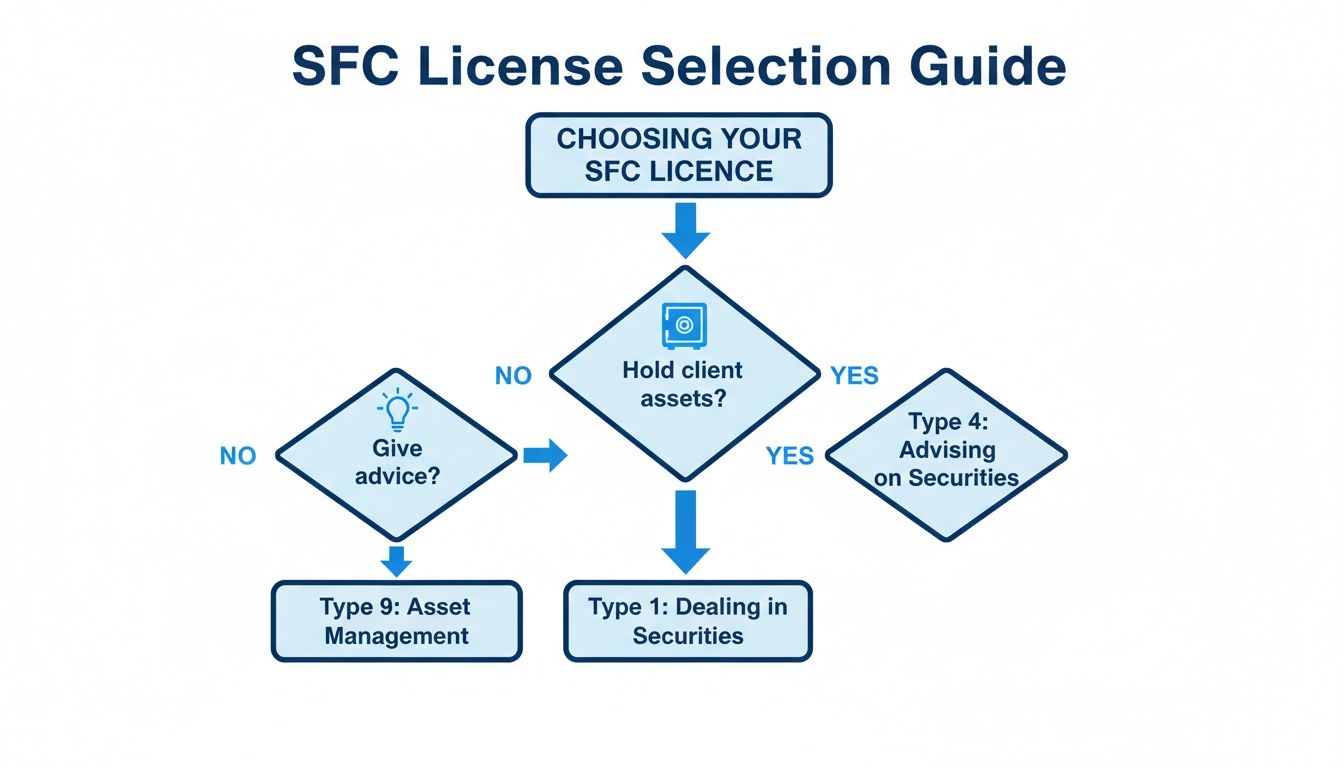

Before you even get to the fit and proper stage, you need to know which licence you’re applying for. This simple flowchart can help you think through the initial questions that determine your licence type.

As the chart illustrates, your core business activities—like whether you hold client assets or just provide advice—point directly to the licence you need. This, in turn, sets the context for how the SFC will evaluate your fitness.

The Three Pillars of the Fit and Proper Test

The SFC looks at your application through three distinct, yet related, lenses. You’ll need to provide solid proof and be completely transparent in each area.

- Reputation, Character, and Integrity

This is the most personal aspect of the test. The SFC investigates the background of the company, its directors, Responsible Officers (ROs), and major shareholders. They’re looking for red flags like criminal records, past disciplinary actions from other regulators, or any hint of dishonesty. For example, if a director was sanctioned by an overseas authority years ago, you must disclose it and provide a full explanation. The scrutiny here is intense, echoing the enhanced due diligence standards for high-risk financial activities. - Competence and Experience

Put simply, your team must know what it’s doing. The SFC reviews the academic qualifications, industry experience, and exam results of your proposed ROs. For a Type 9 (Asset Management) licence, an RO needs to have several years of direct, hands-on portfolio management experience. A finance degree alone won’t cut it; the SFC wants to see a track record of relevant, practical work. - Financial Status and Solvency

This pillar applies to both the individuals and the company. For individuals, the SFC might look into personal bankruptcy history. For the corporation, it’s all about proving you have the financial muscle to operate the business and meet the specific minimum capital requirements for the licence you’re seeking.

Keep in mind, the fit and proper test isn’t a one-and-done deal you pass at the application stage. It’s an ongoing obligation. The SFC expects your firm and everyone licensed under it to remain fit and proper at all times.

Failing to uphold these standards can trigger serious regulatory consequences down the line. So, when you build your application, focus on demonstrating strength across these three pillars. You’re not just trying to get a licence—you’re laying the groundwork for a compliant and sustainable business in Hong Kong.

Your Step-by-Step Guide to the SFC Licence Application

Tackling the SFC licence application can seem intimidating. I’ve seen many firms get bogged down in the details. But if you approach it systematically, it becomes a much more manageable project. Think of it less as an insurmountable hurdle and more as a detailed project plan. This section breaks the journey down into clear phases, ensuring you hit every critical checkpoint from initial prep to final submission.

The biggest mistake I see is firms jumping straight into the application forms without doing the necessary legwork. That’s a surefire way to invite delays and a long list of questions from the SFC. Your first focus must be on building a solid foundation.

Phase 1: Pre-Application Groundwork

Before a single form is filled out, your priority is to get your corporate and personnel house in order. Getting these fundamentals right from the start shows the SFC you’re a serious, well-prepared applicant.

For many overseas businesses, this begins with setting up a proper Hong Kong entity. The process of company incorporation in Hong Kong is the legal bedrock upon which your entire application rests.

Here’s what your essential preparation checklist looks like:

- Appoint Competent Responsible Officers (ROs): You need to identify at least two individuals who can clear the SFC’s rigorous ‘fit and proper’ test. They must have the right industry experience to actually supervise the regulated activities you plan to conduct. Crucially, at least one of these ROs must also serve as an executive director of your firm.

- Draft a Robust Business Plan: This document is your opportunity to tell the SFC your story. It’s not just a formality. Your plan must clearly articulate your business model, target clients, organisational structure, and a realistic three-year financial projection. It needs to be thorough and directly relevant to the licence type you’re seeking.

- Prepare a Compliance Manual: You must develop a comprehensive manual detailing your firm’s internal controls and procedures. This covers everything from your daily operations to how you’ll adhere to SFC regulations on critical issues like anti-money laundering (AML) and counter-terrorist financing (CTF).

Phase 2: Compiling and Submitting Your Application

With the groundwork firmly in place, you can move on to the application itself. This stage is all about precision and attention to detail. Every form must be completed accurately, and all supporting documents must be present and correct.

The SFC requires a specific set of forms for the corporation, each Responsible Officer, and any substantial shareholders. Consistency across all documents is everything. Even a tiny discrepancy can raise a red flag and lead to a query from your SFC case officer.

Pro Tip: Your application package is the SFC’s first real impression of your firm. A complete, well-organised, and clearly structured submission speaks volumes about your professionalism and competence, which can genuinely help smooth out the review process.

The final step is to submit the entire package through the SFC’s online portal, WINGS. Once submitted, the ball is in the SFC’s court. They will assign a case officer to review your submission, and it’s very common for them to come back with requisitions—requests for more information or clarification. Your ability to respond to these requests promptly and completely is key to keeping your application moving forward.

Navigating Capital Requirements and Required Documents

A successful SFC application really comes down to two things: proving your financial stability and getting your paperwork spot on. Think of it as the final, detailed inspection before you’re cleared for takeoff. The SFC needs to be confident that your firm’s financial foundations are solid and that every single document supporting your application is in perfect order.

Getting this right from the start is absolutely critical. While the official SFC licensing handbook lays out the rules, translating that into a practical checklist is what prevents the small, avoidable errors that lead to major delays. Let’s break down exactly what you need for both capital and documentation.

Understanding the Financial Thresholds

The SFC enforces strict minimum capital requirements to ensure licensed firms can handle market fluctuations and operate responsibly. This isn’t just a one-off check when you apply; it’s a financial standard you have to maintain at all times.

You’ll need to focus on two key financial metrics:

- Paid-up Share Capital: This is the actual money shareholders have invested in the company. For a Type 1 (Dealing in Securities) licence, for example, this can range from HKD 500,000 if you’re an introducing agent, all the way up to HKD 10,000,000 for firms that offer securities margin financing.

- Liquid Capital: This is about your firm’s readily available assets—like cash or securities you can sell quickly—minus its ranking liabilities. For that same Type 1 licence, you must maintain a minimum liquid capital of HKD 3,000,000. These rules ensure you always have enough cash on hand to cover your obligations.

The depth of these financial and compliance checks is a core feature of Hong Kong’s regulatory framework, designed to protect market integrity. For a deeper dive, you can find more insights on navigating the SFC’s licensing process on bovill-newgate.com.

Assembling Your Essential Document Package

Beyond the numbers, your application must be backed by a full suite of documents. Together, they give the SFC a complete picture of your business—your operations, your governance, and how you plan to stay compliant.

Your document submission is your first and most important conversation with the SFC. A complete, well-organised, and professional package signals your firm’s competence and shows you respect the regulatory process.

Here are the core documents you’ll need to prepare:

- A Detailed Business Plan: This needs to cover your business model, who your target clients are, your organisational chart, and a solid three-year financial forecast.

- A Comprehensive Compliance Manual: This is your operational rulebook. It must detail your internal controls, risk management framework, and specific policies for anti-money laundering (AML).

- Shareholding Structure Chart: A crystal-clear diagram that traces ownership right up to the ultimate beneficial owners.

- Office Lease Agreement: You’ll need to provide proof of a physical office in Hong Kong that’s appropriate for the activities you plan to conduct.

Putting these materials together with care is non-negotiable. While the context is different, many of the same principles apply to other compliance checks, which we cover in our guide on how to prepare compliance documents for a bank account. Submitting an incomplete or inconsistent package is, without a doubt, one of the most common reasons applications get held up.

Maintaining Compliance After Your Licence Is Approved

Securing your SFC licence is a massive achievement, but it’s really just the starting line of your regulatory journey. The moment your licence is granted, you shift into a new, continuous phase: ongoing compliance. This is where your firm proves its commitment to upholding the demanding standards of Hong Kong’s financial markets every single day.

Think of it like this: the application was the rigorous exam to get your pilot’s licence. Now you have it, but you’re expected to follow the flight plan and safety protocols on every trip. The SFC needs to see that you’re not just capable on paper but are a responsible operator in practice.

Your Core Ongoing Obligations

Keeping your licence in good standing is about a constant cycle of monitoring, reporting, and training. It’s far more than a box-ticking exercise; it needs to be woven into your company’s culture. The official SFC licensing handbook is your bible for these duties, but let’s break down the essential operational pillars you can’t afford to ignore.

Your primary responsibilities boil down to a few key areas:

- Maintaining Capital Adequacy: You must always meet the minimum paid-up share capital and liquid capital requirements for your specific licence type. This isn’t a one-and-done check at the application stage; your financial health is monitored continuously.

- Submitting FRR Returns: Licensed corporations are required to submit regular Financial Resources Rules (FRR) returns. These reports give the SFC a detailed snapshot of your liquid capital position, demonstrating that you remain financially sound.

- Conducting Annual Audits: You’ll need to appoint an auditor and submit your firm’s audited financial statements to the SFC within four months of your financial year-end.

This constant oversight is a signature feature of Hong Kong’s robust regulatory environment. The market has seen steady growth, with licensed corporations now numbering in the thousands and licensed individuals in the tens of thousands. The SFC’s strict post-licence supervision is what ensures this expansion doesn’t come at the cost of market integrity. For a closer look, you can always explore the latest SFC statistics on market participants.

Building a Culture of Compliance

Beyond the hard numbers in your financial reports, your firm’s internal controls are equally critical. These are the day-to-day systems and procedures that guide your team’s behaviour and—crucially—stop regulatory breaches before they even happen.

A strong compliance culture isn’t just about avoiding fines; it’s a powerful business asset that builds trust with clients, attracts top talent, and creates a stable foundation for growth.

Key internal compliance functions include:

- Robust AML/CTF Procedures: You must have stringent Anti-Money Laundering and Counter-Terrorist Financing systems in place. This includes everything from thorough client due diligence (“know your client” or KYC) to active transaction monitoring.

- Continuous Professional Training (CPT): Your Responsible Officers and Licensed Representatives have to complete a minimum number of CPT hours each year. This ensures they stay sharp and up-to-date with evolving regulations and market practices.

- Strict Internal Controls: A vital part of your duty is making sure licensed individuals don’t engage in unauthorised activities. This requires active supervision and clear internal policies for understanding and preventing misconduct like selling away.

Staying on top of these post-licence obligations is fundamental to your firm’s reputation and long-term survival. It signals to the SFC, and the wider market, that you are a serious and responsible participant dedicated to protecting investors.

Conclusion

Navigating the dense SFC licensing handbook is a challenge best met with expert guidance. At Lion Business Consultancy Limited, we don’t just process paperwork; we act as your strategic partner to ensure your application is solid, compliant, and ready for approval. Let us handle the regulatory complexities so you can focus on what you do best—building your business.