Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

Welcome to Hong Kong's dynamic property market—a landscape teeming with opportunity. For entrepreneurs and SME owners, getting a handle on property tax in Hong Kong isn't just about ticking a compliance box; it's a core business strategy that directly hits your bottom line.

Mapping Out Hong Kong Property Taxes

Diving into Hong Kong’s real estate world can feel a bit like learning a new language. As a business owner, you’re not just finding a location; you’re making a significant financial commitment. Nailing this from day one means knowing precisely which taxes apply and when they kick in.

Think of the system as a financial map for your property journey. Without it, you’re navigating blind, risking unexpected costs that can eat into profits and throw a wrench in your operations. A clear understanding, on the other hand, gives you a solid foundation for making smart, profitable real estate decisions for your growing business.

The Core Property Levies for Your Business

First things first, let's meet the main players on the board. Each tax serves a different purpose and is triggered by different events, so knowing them apart is absolutely crucial.

Here are the key taxes every SME owner needs to have on their radar:

- Property Tax: This is the big one for rental income. If you own and lease out a property—be it an office, a warehouse, or a retail shop—the government will tax the income you earn.

- Stamp Duty: Think of this as a one-off tax on property transactions. You'll encounter it when you buy, sell, or even sign a new lease. The cost can be significant, so it’s a critical piece of the puzzle for your capital planning.

- Rates and Government Rent: These are the ongoing costs of holding property. Rates help fund public services like policing and infrastructure, while Government Rent is basically a lease payment for the patch of land your building sits on.

"For SMEs in Hong Kong, property is often the second-largest expense after payroll. Treating property tax knowledge as a strategic asset, not an administrative burden, is what separates a good business from a great one."

Why This Matters for Your SME

Getting these rules down isn't just about dodging penalties. It shapes huge business decisions, like whether to lease an office or buy a commercial unit, and how to structure real estate investments for the best returns. It's also worth remembering that your property-related income can interact with your company’s main earnings. You can learn more about how your business profits are taxed by exploring our guide on Hong Kong profits tax.

This guide is designed to be your practical playbook. We’ll break down each tax, show you exactly how it’s calculated, and clarify what your obligations are. By the end, you'll have the confidence to navigate the system, turning compliance into a genuine competitive advantage.

How Property Tax on Rental Income Works

If you're renting out a property in Hong Kong, whether it's commercial or residential, the income you earn is subject to what's known as Property Tax. It's a common point of confusion, but this isn't a tax on the value of your property itself.

Think of it more like an 'income tax' specifically for your rental earnings. Every dollar of rent is revenue, and the government takes a predictable slice. This framing is especially useful for entrepreneurs and SMEs, as it helps clarify that this is a tax on a business income stream, not on the asset's capital value.

From Gross Rent to Your Taxable Base

The whole process starts with a simple number: your gross rental income. This is the total amount of rent you're entitled to collect for the financial year, which runs from 1 April to 31 March. It’s not just the base rent; it also includes any extras your tenant pays you for things like management fees or services that are ultimately your responsibility as the owner.

From this gross figure, the Inland Revenue Department (IRD) lets you make a couple of key deductions to get to what they call the Net Assessable Value (NAV). This NAV is the magic number your tax bill is actually based on.

The core idea is straightforward: tax is charged on the rental income you make from a property in Hong Kong. The government applies a flat standard rate of 15% to the net assessable value. This keeps things relatively simple for landlords. For a wider look at the local tax environment, you can find a good overview of taxation in Hong Kong on china-briefing.com.

The 20% Deduction: A Welcome Simplification

Here’s where the Hong Kong system really shines for landlords. Instead of forcing you to track and document every single penny spent on repairs, maintenance, or insurance, the IRD gives you a blanket 20% statutory allowance.

This automatic deduction is a huge time-saver. It’s taken straight off your rental income (after accounting for any irrecoverable rent or rates you’ve paid) and saves you a mountain of paperwork.

Let's walk through how it works step-by-step:

- Start with your total annual rental income (the Gross Assessable Value).

- Subtract any rent you couldn't collect (e.g., a tenant who defaulted).

- Deduct any Government Rates you paid as the owner.

- From that new total, take off the standard 20% allowance for repairs and outgoings.

- What's left is your Net Assessable Value (NAV)—the final figure that will be taxed.

It's important to remember this 20% deduction is fixed. You can't claim more if your actual repair costs were higher. On the flip side, you still get the full 20% even if you spent nothing on the property that year. It’s a trade-off for simplicity.

The Standard Rate and When You Pay

Once you have your NAV, the final step is a breeze. The property tax in Hong Kong is charged at a flat standard rate of 15%.

Tax Payable = Net Assessable Value (NAV) x 15%

So, who pays? The legal owner of the property is on the hook for filing the return and settling the bill, whether that owner is an individual, a partnership, or a company.

The payment schedule works on a provisional system. Your tax bill from the IRD will have two components:

- The final tax you owe for the previous financial year.

- A provisional tax payment for the current year, which is usually just an estimate based on last year's income.

This provisional amount is then credited towards your final bill the following year. Typically, you'll file your property tax return (Form BIR57) around May, get your assessment notice later in the year, and then pay in two instalments, usually in January and April.

Getting to Grips with Stamp Duty on Property Deals

Whenever you buy, sell, or even lease property in Hong Kong, you’re going to run into Stamp Duty. Imagine it as a one-off tax you pay to make a property agreement official. For any SME, this can be a serious chunk of change, so getting your head around the details is essential for proper budgeting and smart financial planning.

Unlike the recurring property tax on rental income, Stamp Duty is triggered by a specific event – the moment you sign a sale and purchase agreement or a tenancy agreement. It’s a major upfront cost that you absolutely have to factor into any deal right from the start.

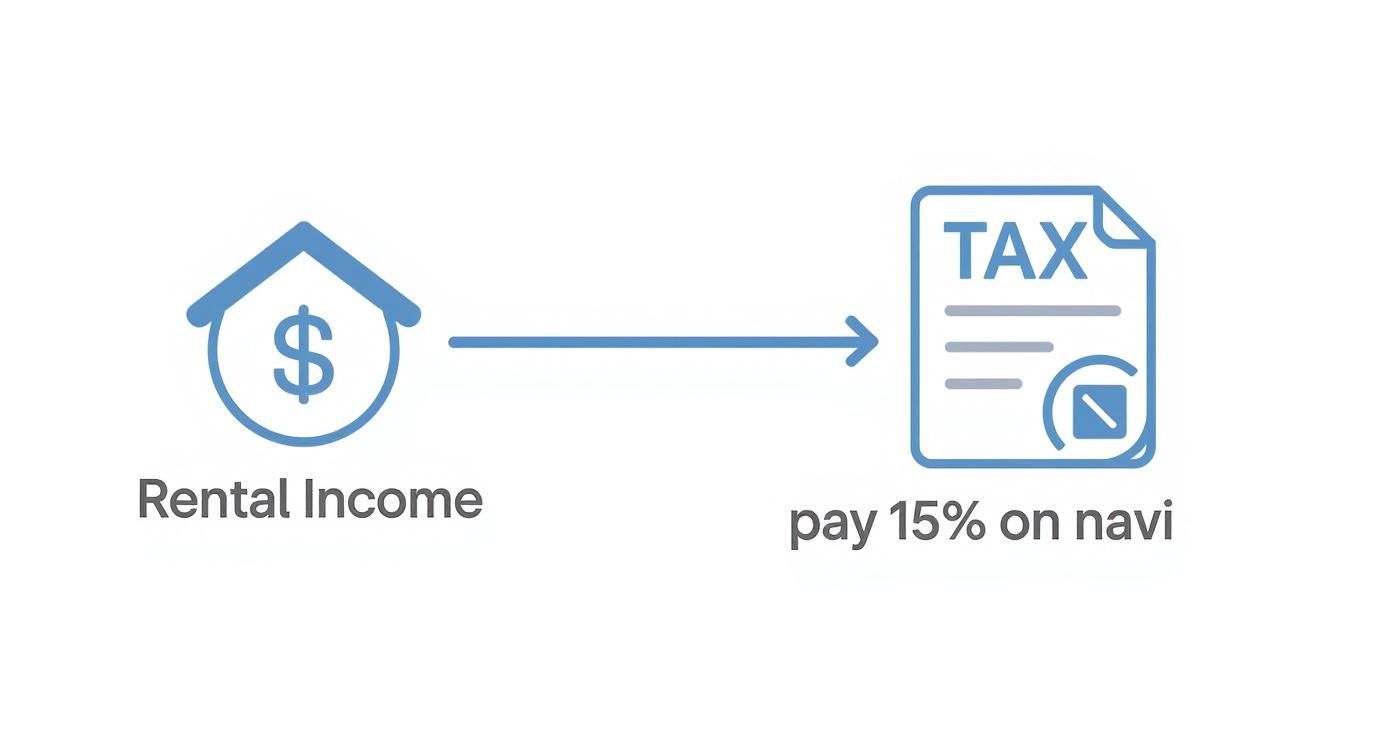

This decision tree gives you a quick visual on how property tax works based on rental income.

As you can see, the core idea is simple: if your property brings in rent, you’re looking at a 15% tax on its net assessable value.

Ad Valorem Stamp Duty (AVD)

The most common type of stamp duty is the Ad Valorem Stamp Duty (AVD). "Ad valorem" is just a fancy Latin way of saying "according to value." It’s calculated on a tiered scale based on either the property's sale price or its market value—whichever is higher.

For a long time, the AVD rates were pretty straightforward for non-first-time buyers or companies. But now, Hong Kong Permanent Residents buying their first home benefit from lower, progressive rates (known as Scale 2 rates). The government has also tweaked these tiers to give smaller buyers a bit of a break, recently raising the threshold for the lowest AVD tier from HKD 3 million to HKD 4 million.

The So-Called "Spicy Measures"

To cool down what has historically been a red-hot property market, the government introduced a few extra layers of stamp duty. In the industry, everyone knows them as the "spicy measures." They were specifically designed to clamp down on speculative buying and give local homebuyers a leg up.

These taxes add some serious cost for certain buyers or quick-turnaround sales, so if you're a non-resident investor or a company, you need to know about them.

- Special Stamp Duty (SSD): This one is all about targeting property flippers. If you buy a home and then sell it within 24 months, you’ll get hit with a hefty SSD on top of the regular AVD. The rates are punishingly high for the quickest sales, starting at 20% if you sell within the first six months.

- Buyer's Stamp Duty (BSD): This applies to any residential property bought by a non-Hong Kong Permanent Resident or any company, whether it’s local or foreign-owned. It’s a flat 15% of the property's value, and you have to pay it in addition to the AVD.

Here’s some good news for SMEs: these "spicy measures" (SSD and BSD) are almost exclusively for residential properties. If you're buying an office, a warehouse, or another commercial space, you generally don't have to worry about these extra punitive rates—you’ll just face the standard AVD.

For a quick overview, here’s how these different stamp duties stack up.

Hong Kong Stamp Duty Snapshot for SMEs

| Stamp Duty Type | Who It Primarily Affects | When It Is Applied | Key Objective |

|---|---|---|---|

| Ad Valorem (AVD) | All property buyers (tiered rates for some residents) | On signing a sale & purchase or lease agreement | To tax the value of all property transactions. |

| Special (SSD) | Short-term residential property sellers ("flippers") | On the resale of a residential property within 24 months | To discourage short-term speculation and stabilise the market. |

| Buyer's (BSD) | Non-resident and corporate buyers of residential property | On the purchase of a residential property | To prioritise local homebuyers over foreign and corporate investors. |

This table helps clarify which tax applies to whom, making it easier to see how a transaction might be structured for your business.

How This Plays Out for Your Business

Let's bring this down to earth with a practical example. Imagine your SME wants to buy its first commercial office space for HKD 10 million. In this scenario, you would only need to budget for the standard Ad Valorem Stamp Duty. Simple.

But what if your business, registered as a Hong Kong company, decides to buy a residential apartment for the same price—maybe for executive housing? The maths changes completely. You’d be on the hook for both the AVD and the 15% Buyer's Stamp Duty, which would massively inflate your upfront costs.

This distinction is absolutely critical for financial planning. The final stamp duty bill can look wildly different depending on the property type and who is buying. For a wider perspective on how such taxes can influence market behaviour, it's worth reading about understanding the impact of stamp duty on property transactions. While the market is different, the core principles of how transaction taxes shape investment decisions are universal.

Decoding Rates and Government Rent

When you own or occupy a property in Hong Kong, you’ll quickly encounter two recurring charges that are part of the landscape: Rates and Government Rent. It's a common mistake to bundle these in with 'property tax', but they are completely separate charges, each with its own purpose.

Think of them as the predictable, ongoing costs of holding property, much like a service subscription. Just as you’d budget for building management fees or utilities for your office, these are non-negotiable expenses that need a permanent spot in your financial forecasts. Getting a handle on them from the start is crucial for managing your cash flow without any nasty surprises down the line.

So, What Exactly Are Rates?

Rates are essentially a tax that helps pay for the essential public services that keep Hong Kong safe, clean, and efficient. The revenue collected is ploughed directly back into the city's operations, funding things that every business and resident benefits from.

This includes paying for:

- The Police Force and Fire Services

- Public health and sanitation, such as refuse collection

- Maintaining public infrastructure like roads, drains, and parks

In short, paying Rates is your contribution to the civic machinery that makes Hong Kong such a prime location for business. While the legal liability to pay falls on the occupier, it’s standard practice in most commercial leases for the landlord to handle the bill and then recharge the cost to the tenant.

And Government Rent?

Government Rent comes from a completely different principle. It’s rooted in the historical fact that almost all land in Hong Kong is owned by the government and leased out on long-term arrangements to developers and, by extension, property owners.

You can think of Government Rent as a small, annual rent payment you make to the government for the right to occupy the patch of land your building sits on. It's a formal acknowledgement of the government's ultimate ownership of the land itself.

This applies to nearly every property across the city. Unlike Rates, the responsibility for paying Government Rent rests firmly with the owner of the property—it’s a fundamental cost of ownership that cannot be passed on.

The Nuts and Bolts of Calculation and Payment

Conveniently, both Rates and Government Rent are calculated using the same starting point: the rateable value of your property. This is the government's official estimate of your property's annual rental value on the open market, assessed by the Rating and Valuation Department (RVD).

Here’s how the numbers stack up:

- The RVD sets the Rateable Value (RV): They assess what your property could fetch in rent for a year. This figure is updated annually to keep pace with market conditions.

- The government applies a percentage: Each financial year, a set percentage is announced for both charges.

- For the 2024-25 financial year, Rates are charged at 5% of the rateable value.

- Government Rent is charged at 3% of the rateable value.

Let’s run a quick example. Imagine your company’s office has an official rateable value of HKD 500,000 for the year:

- Annual Rates Payable: HKD 500,000 x 5% = HKD 25,000

- Annual Government Rent: HKD 500,000 x 3% = HKD 15,000

You won't get separate bills for these. They are combined onto a single "Demand for Rates and Government Rent" note, which is sent out quarterly. This means you can expect a bill four times a year, with payments typically due in January, April, July, and October. This predictable rhythm makes it easy to factor into your SME's budget.

While the government occasionally offers a waiver on Rates for a quarter or two to provide relief, it's always smartest to budget for the full annual amount, just in case.

Tax Planning and Relief Strategies for SMEs

Knowing the rules of property tax in Hong Kong is one thing. Learning how to play the game to your advantage is another entirely. For an SME, this isn't about shady loopholes; it’s about making smart, legitimate choices to manage your tax obligations effectively.

Think of it this way: tax compliance can be more than just a cost centre. With the right strategy, it becomes a powerful financial tool. Let's walk through the playbook for minimising your tax exposure and freeing up cash for your business.

The Power of Electing for Personal Assessment

One of the most effective strategies for individual property owners—and that includes many SME founders who own property in their own name—is electing for Personal Assessment. It's a voluntary option, but it can be a real game-changer.

Here’s the deal: instead of paying the flat 15% property tax on your rental income, Personal Assessment lets you group that income with all your other earnings, like your salary or business profits. This combined income pool is then taxed at progressive personal rates, which start as low as 2%.

If your total income keeps you out of the highest tax brackets, this move can seriously slash your tax bill. It’s a simple case of bundling everything together to get a better rate.

This election is a no-brainer if your personal tax rate is lower than the 15% standard property tax rate. It also lets you offset property rental losses against your other income—a huge benefit you can't get when property tax is calculated on its own.

Who Should Consider Personal Assessment

This option is a particularly good fit for:

- SME owners with moderate total income: If your salary plus rental income doesn't push you into the top tax tiers, you're very likely to save money.

- Landlords with newly acquired properties: Early on, you might face rental losses from vacancies or initial renovation costs. Personal Assessment allows you to use those losses to lower the tax on your other earnings.

- Individuals with significant personal allowances: Your basic allowance, married person's allowance, and other deductions can be applied to your total combined income, shrinking your taxable base even further.

But it’s not for everyone. If you're a high-income earner already paying tax at the top marginal rate, the flat 15% property tax might actually be cheaper. It always pays to run the numbers. Understanding the wider principles behind property investment tax benefits can also provide valuable context for making these decisions.

Other Key Reliefs and Deductions

Beyond Personal Assessment, a few other reliefs are essential to know. Getting these right ensures you’re not overpaying.

- Deduction for Unrecoverable Rent: If a tenant skips out on their rent and you can't get it back, you can deduct that amount. This is a crucial protection, preventing you from being taxed on money you never actually received.

- Owner-Occupied Business Premises: If your SME owns the property it operates from, you don't pay property tax on it because there's no rental income. Better yet, property expenses like mortgage interest can often be deducted against your business profits when calculating Profits Tax.

- Rates Paid by the Owner: As mentioned earlier, any Government Rates you pay as the owner can be deducted from your rental income before the standard 20% repair allowance is calculated.

Keeping track of all this requires organised records. That's why many business owners find that professional accounting services in Hong Kong pay for themselves by ensuring every available relief is claimed correctly and without compliance headaches.

Case Study: A Local Design Studio

Let's make this real. Imagine "Artisan Designs," a small creative studio in Sheung Wan. The founder, Emily, personally owns a small unit above the studio that she rents out to a freelance photographer for HKD 240,000 a year.

Under the standard property tax regime, her bill would be (HKD 240,000 x 80%) x 15% = HKD 28,800.

But Emily's salary from her business is fairly modest. By opting for Personal Assessment, she pools her rental income with her salary. After claiming her personal allowances, her marginal tax rate is just 10%.

Suddenly, the tax on her rental income drops significantly. This one smart decision saves her thousands of dollars every year—money she can pump straight back into growing her design studio. It's a perfect illustration of how proactive tax planning can directly fuel an SME's success.

Common Questions About Hong Kong Property Tax

Getting your head around property tax in Hong Kong throws up all sorts of practical questions, especially when you're trying to make the right call for your business. Think of this as your go-to guide for the common queries we hear from entrepreneurs every day. We'll give you straight, clear answers so you can move forward with confidence.

Can I Deduct Mortgage Interest Payments?

This is easily one of the most common questions, and the answer is a firm no—at least, not directly from your Property Tax bill.

The tax is calculated purely on your rental income, and the Inland Revenue Department gives a standard 20% allowance for all repairs and outgoings. This flat-rate deduction is a catch-all meant to cover everything from mortgage interest and management fees to general upkeep. No itemising is needed.

However, there's a vital workaround for SMEs. If your business owns the property it operates from, there's no rental income and therefore no Property Tax to pay. In that scenario, you can often deduct the mortgage interest as a standard business expense when calculating your company's Profits Tax. It's a different tax, but the outcome is the same: a valuable deduction for your business.

How Does Late Rental Income Affect My Filing?

Chasing late rent is a pain, but the tax side of it is actually quite simple. Property Tax works on an "accrual basis." This just means you report the rental income you were supposed to receive during the financial year, not what you actually had in the bank by the deadline.

Remember, the tax year in Hong Kong runs from 1 April to 31 March.

So, if your tenant owes you rent for March but doesn't pay up until May, you still have to include that March rent on your return for the year ending 31 March. If it later turns out that the rent is truly unrecoverable, you can then claim it as a bad debt deduction in the year you write it off.

Key Takeaway: You're taxed on the rent that was due within a specific financial year, regardless of when it was actually paid. It keeps the accounting clean and aligned with standard business practice.

Should My SME Buy Property Under a Company Name or My Name?

This is a huge strategic decision with serious tax implications. There's no one-size-fits-all answer here; it really depends on your business goals and personal financial situation.

Let’s break down the main angles:

- Buying as a Company: This is usually the go-to option for commercial properties. It neatly separates your business and personal liabilities, and expenses like mortgage interest can be written off against profits. The big catch? If you buy a residential property this way, your company will get hammered with the hefty Buyer's Stamp Duty (BSD).

- Buying as an Individual: If you're a Hong Kong Permanent Resident buying your first home, you get access to much lower stamp duty rates. You can also opt for Personal Assessment, which could potentially lower your overall tax rate on any rental income. The downside is that it mixes your personal and business finances, which can get messy.

This choice directly impacts your upfront costs and long-term tax bill, so it’s something you need to plan out carefully.

Are Commercial and Residential Units Taxed Differently?

When we're talking about the ongoing Property Tax on rental income, the rules are exactly the same. The flat 15% rate on the Net Assessable Value applies whether you own a downtown office, a retail shop, or a residential flat. The calculation, including that 20% standard deduction, doesn't change.

The real difference, as mentioned before, is in the Stamp Duty you pay when you buy the place. Commercial properties are exempt from the government's "spicy measures" like Special Stamp Duty (SSD) and Buyer's Stamp Duty (BSD). This makes buying a commercial space through a company far more tax-efficient than buying a residential unit—a crucial point for any SME looking to invest.

Conclusion

At Lion Business Consultancy Limited, we know every property decision is a cornerstone of your business strategy. We act as your private financial manager, offering the clear, one-on-one guidance needed to navigate complex tax structures and secure your assets for long-term growth. To build a compliant and tax-optimised framework for your global expansion, visit us at https://lionbusinessco.com.