Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

Opening a bank account in Hong Kong boils down to a few core requirements: proving who you are, where you live, and why you need the account. This might sound simple, but for entrepreneurs and businesses eyeing this global financial hub, it's the critical first step on a much bigger journey.

Getting Started with Hong Kong Banking

For anyone new to the scene, the idea of opening a bank account in Hong Kong can feel like a daunting task. It’s often the first real hurdle, tangled up in what seems like endless paperwork and strict rules. But it really doesn’t have to be a nightmare.

My aim here is to give you a clear, no-nonsense roadmap. I want to cut through the banking jargon and show you how to prepare for a smooth opening, sidestepping the common pitfalls that catch so many people out.

Hong Kong's reputation as a world-class business centre is well-earned. There are solid reasons why it’s still the top choice for international companies:

- Global Financial Centre: Its location is a strategic bridge between East and West, all backed by a reliable legal system that businesses trust.

- Freely Convertible Currency: The Hong Kong Dollar (HKD) is pegged to the US Dollar, which brings a welcome dose of stability to international transactions.

- Diverse Banking Options: You’ve got the global powerhouses like HSBC and Standard Chartered, but also a new breed of agile, digital-only banks. There’s a fit for almost any kind of business.

Understanding the Modern Banking Landscape

Banking isn't just about walking into a physical branch anymore. The rise of digital banking and new fintech solutions has completely changed the game, bringing more flexibility and efficiency to the table. As you dive in, it’s worth getting some practical insights into open banking integration to see how technology is making it easier for businesses to manage their money seamlessly.

This evolution means that while traditional banks maintain their rigorous compliance standards, technology is speeding things up. For example, several virtual banks now let you open an account entirely online, swapping face-to-face meetings for secure video calls and biometrics.

A successful bank account application is less about just submitting documents and more about telling a clear, compelling story about your business. Banks want to see a legitimate operation with a clear purpose, a logical flow of funds, and a transparent structure.

When you understand what the bank is looking for from the very beginning, you can build a much stronger application. It’s not just about ticking off boxes on a form; it’s about establishing trust with your financial partner from day one. Next, we'll get into the details of choosing the right bank and getting your documents in perfect order.

Choosing the Right Bank for Your Goals

Picking a bank in Hong Kong is about more than just finding a place to park your cash; it’s about finding a strategic partner for your business's future. The banking scene here is incredibly diverse, and the "best" bank for you is completely tied to your specific situation. If you rush this decision, you could easily end up with high fees, operational headaches, and a banking partner who just doesn't get what you do.

Let me tell you about two entrepreneurs I've worked with. The first runs a UK-based e-commerce business, sourcing products from mainland China and selling to customers worldwide. The second is a freelance software developer, a digital nomad getting paid by clients in the US and Europe. Their banking needs couldn't be more different. The e-commerce owner needed a bank with solid trade finance options and robust multi-currency accounts. The developer, on the other hand, just needed low-cost international transfers and a slick mobile banking app.

This is the heart of the matter. You have to match a bank's strengths to your day-to-day reality. Don't just open a bank account with the first one that says yes. Think of it like hiring a key employee—you need the right fit for the job.

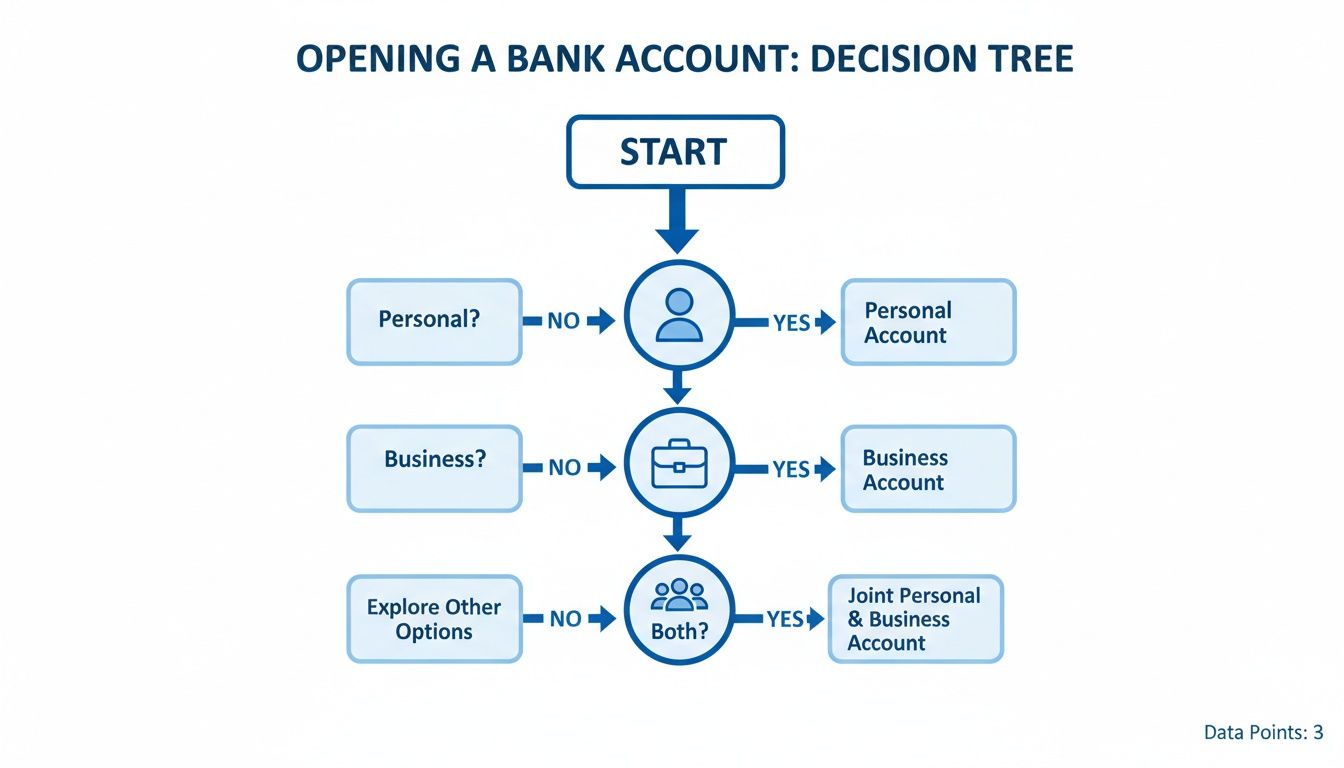

The decision tree below gives you a simple framework for mapping out your needs, whether they're for personal finances, your business, or a bit of both.

This visual guide helps you navigate that first critical choice, pushing you to decide if your main priority is managing personal money, running your business, or finding an integrated solution.

Traditional Banks vs. Virtual Banks

Hong Kong's banking world is a fascinating mix of old-school giants and agile new players. Getting a handle on their differences is key.

-

Traditional Banks (e.g., HSBC, Standard Chartered, Bank of China): These are the names everyone knows. They offer everything under the sun, from basic accounts to complex trade financing and wealth management. Their physical branches are a huge plus if you need to do things in person, like depositing large cash sums or getting complex documents certified. For an SME heavily involved in import/export, their deep expertise in letters of credit is priceless.

-

Virtual Banks (e.g., ZA Bank, Mox Bank, Airstar Bank): These are the new kids on the block, operating entirely online. They're fully licensed and regulated, just like the big guys, but their appeal comes from lower fees, easier online applications, and genuinely user-friendly apps. For a tech start-up or a consultant, a virtual bank can provide all the horsepower you need for daily operations without the traditional overheads.

The real question isn't which type of bank is "better," but which is better for you. A business dealing in physical cash or needing sophisticated trade tools will likely find a traditional bank essential. On the flip side, a digitally-native company might see the speed and low costs of a virtual bank as the perfect fit.

Key Questions to Ask Before You Choose

Before you sign on the dotted line, treat the process like an interview. You’re checking them out just as much as they’re checking you out. Make sure you get straight answers to these questions:

-

What's the real cost? Ask about account opening fees, monthly maintenance charges, and any minimum balance requirements. Really dig into the fees for international transfers—both sending and receiving—because those can pile up fast. A bank might advertise a "free" account but then hit you with high charges for the services you actually need.

-

Do they "get" your business? Does the bank have a track record with companies in your industry? This is particularly important for newer fields like e-commerce, SaaS, or digital services. A banker who understands your revenue model will make your life so much easier.

-

How good is their tech and support? Is their online platform actually intuitive? Can you do everything you need online, or will simple tasks force you into a branch? Give their customer support a test run. A responsive relationship manager can be an absolute lifesaver when you run into an urgent issue.

Making the right choice from the get-go saves you from a world of future pain. To help you weigh your options, our detailed guide on the complete list of banks in Hong Kong gives you a great overview of the players in the market. It’s the perfect starting point for shortlisting potential partners that truly align with where you want to take your business.

Preparing Your Documents for a Smooth Application

If there’s one secret to successfully opening a bank account, it’s this: preparation is everything. From my experience, the vast majority of application delays, frustrations, and flat-out rejections boil down to one simple thing—disorganised or incomplete documentation.

Think of your application not just as a form to fill out, but as the first chapter in your relationship with the bank. A messy, incomplete story raises immediate red flags for compliance officers who are trained to spot inconsistencies. On the other hand, a well-prepared, transparent, and comprehensive document package tells them you're a serious, organised professional. It builds confidence right from the start.

The Core Personal Documents Everyone Needs

Let’s start with the basics that apply to everyone, whether you’re opening a personal or business account. These are the non-negotiables for verifying who you are.

-

Valid Passport: This can’t be a simple photocopy. You'll need a clear, certified copy, which means it’s been verified by a qualified professional like a lawyer, notary, or chartered accountant.

-

Proof of Residential Address: This is a classic stumbling block. Banks need a recent utility bill (electricity, water, gas) or a statement from another bank, typically dated within the last three months. It must clearly show your full name and current address.

A common mistake I see is entrepreneurs trying to use a PO Box or a virtual office address for this. That won't work. Banks need your physical residential address for their Know Your Customer (KYC) checks. Get this right, and you've already cleared a major hurdle.

Essential Paperwork for Your Business Account

When you’re opening a business account, the document requirements go much deeper. The bank isn't just verifying you; it's verifying your entire business. They need to understand what you do, who owns the company, and where your money comes from and goes.

Here’s what you should have ready to go:

-

Company Registration Documents: This covers your Certificate of Incorporation, Business Registration Certificate, and Articles of Association. These are the official papers that prove your company legally exists.

-

Register of Directors and Shareholders: The bank needs a transparent breakdown of who controls the company. Be ready to provide ID for every significant shareholder—that usually means anyone with 10% or more ownership.

-

Proof of Business Address: Just like your personal address proof, this could be a recent utility bill for your office or a formal tenancy agreement.

-

A Detailed Business Plan: This is your chance to tell your story. It shouldn’t be a novel, but it must clearly explain your business model, target market, key suppliers and customers, and realistic revenue projections. A vague description like "international trade" is an instant red flag. Be specific.

Banks are legally obligated to prevent money laundering and terrorist financing. Your business plan and supporting documents are their primary tools for assessing risk. A clear, logical, and verifiable story makes their job easier and your approval faster.

For a deeper dive into assembling your compliance file, our guide on how to prepare compliance documents for a bank account provides a detailed checklist to ensure nothing is missed.

The Rise of Digital Verification

Thankfully, the whole process is becoming much smoother. In Hong Kong, for instance, digital banking adoption soared to 62.9% in a recent survey, a testament to the seamless shift towards virtual account openings.

This trend means you can often get everything done in minutes. Apps from virtual banks like ZA Bank or Mox use eKYC, which only requires a scan of your ID and a quick selfie. You can bypass the need to ever visit a branch. You can discover more insights about this trend and user experience on The Asian Banker.

This digital shift is fantastic news for international entrepreneurs, making banking more accessible than ever. However, the core principles haven’t changed. Whether you’re uploading a PDF or handing a document over in person, it must be accurate, complete, and tell a consistent story. Taking the time to get this right from the beginning will save you weeks, if not months, of frustrating back-and-forth.

Navigating KYC and Compliance Requirements

Once your paperwork is lined up, you enter the world of compliance. This isn't just about ticking boxes for the bank; it’s a serious legal and ethical line in the sand. To open a bank account smoothly, you need to think like a compliance officer. They aren't there to make your life difficult—they're the gatekeepers protecting the entire financial system from being exploited.

Think of it this way: a bank's reputation is everything. One bad decision involving a high-risk client can trigger massive fines and do irreparable damage. So, as they look over your application, they're asking one simple question: "Can we trust this person and their business?" Your job is to give them every reason to say "yes."

The entire process boils down to a few core ideas you'll need to get right.

Decoding KYC and AML

Know Your Customer (KYC) and Anti-Money Laundering (AML) are two sides of the same coin. KYC is how the bank verifies who you are and gauges any potential risks you might represent. AML covers the specific measures they take to prevent criminals from washing dirty money through their systems.

So, what are compliance officers actually looking for?

- A Clear Source of Wealth (SOW): Where did your start-up capital come from? Be ready to prove it with bank statements, a business sale agreement, or inheritance documents. Vague answers are a huge red flag.

- A Legitimate Business Model: Your business has to make sense on paper. If you're a software consultant, your transactions should reflect that—invoices from clients, not a stream of unexplained cash deposits.

- Total Transparency: Trying to hide who really owns the company or using overly complicated corporate structures for no clear commercial reason is a fast track to rejection.

Building a watertight case from the get-go is non-negotiable, and for non-residents, the scrutiny is even tighter. Our detailed guide on KYC requirements for non-resident accounts breaks down what you'll need to prepare for those deeper dives.

The point of compliance isn’t to block you; it’s to build a trusted, long-term relationship. A transparent, well-documented application that tells a consistent story is the quickest path to approval and helps you steer clear of account freezes down the line.

International Tax Compliance: The CRS Factor

It’s not just about your identity; banks are now on the front lines of global tax enforcement. The Common Reporting Standard (CRS) is a big part of this. It’s an international agreement that forces banks in places like Hong Kong to automatically share your financial account information with the tax authorities where you are a resident.

This means if you live in the UK and open an account in Hong Kong, your HK bank will report your account details to the Hong Kong Inland Revenue Department. They, in turn, will pass that information straight to HMRC in the UK.

There's no getting around this. You will have to fill out a CRS self-certification form declaring your tax residency when you apply. It is absolutely critical that you complete this accurately, as providing false information can bring serious penalties.

Avoiding Common Compliance Pitfalls

So many good applications get tripped up by simple, avoidable mistakes. One common headache, especially for international founders, is the digital identity check. Often, you need a local phone number for an SMS confirmation code, which is tough if you haven't physically moved yet. In these cases, using services that provide temporary virtual phone numbers for SMS verification can be a clever workaround to get you past that hurdle.

Another classic pitfall is when your stated business activity doesn't match your actual transactions. For example, you register as a management consultancy, but your account suddenly starts receiving thousands of small, frequent payments. To the bank, that looks a lot like an undeclared e-commerce venture. This is exactly the kind of inconsistency that triggers an account review, or worse, a freeze.

The lesson here is simple: be upfront and honest about your entire operation from day one.

What to Expect: Timelines, Fees, and Sidestepping Common Mistakes

Let's be realistic for a moment. When you set out to open an international bank account, managing your expectations is half the battle. Knowing roughly how long the process will take and what it’s likely to cost can turn a frustrating experience into a straightforward one. This isn't an instant process, and hidden fees can pop up if you’re not looking for them.

First, let's talk about time. If you're opening a simple personal account with a modern digital bank, you could be approved and ready to go in hours, maybe even minutes. However, for a corporate account, especially one with international shareholders or a complex ownership structure, you need to think in terms of weeks, not days. For really intricate cases, it could even take a couple of months. The bank isn't just checking one person's ID; they're digging into an entire business ecosystem to understand the risk.

Uncovering the Real Cost of Banking

Next up: fees. This is where things can get tricky. It’s easy to be tempted by an account that advertises no monthly charges, but the real costs are often buried in the fine print, tied to how you actually use the account.

Here’s a quick rundown of the typical charges you need to keep an eye on:

- Account Opening Fee: Some banks, particularly for high-value corporate clients from overseas, will charge a one-off fee just to get your application through the door.

- Minimum Deposit: While not strictly a fee, it's money you have to park in the account. This can be anything from zero for a basic retail account to tens of thousands of dollars for premium business services.

- Monthly Maintenance: This is a standard charge, but banks will often waive it if you keep a certain amount of money in the account.

- Transaction Fees: This is a big one. For any business operating internationally, the cost of sending and receiving international wire transfers can add up fast. Pay very close attention to these.

Hong Kong’s banking system is a great example of a robust market. It's incredibly liquid, with licensed banks holding total deposits of 17,945,976 million HKD as of March 2025. This stability creates a competitive landscape with a vast array of options, from simple savings accounts to highly sophisticated corporate facilities. You can dive deeper into the latest Hong Kong monetary statistics if you're interested.

Common Pitfalls We’ve Seen (And How to Avoid Them)

Over the years, I’ve seen the same handful of mistakes derail applications for even the smartest entrepreneurs. Knowing what these are from the outset will save you a world of headaches.

The number one error? A vague or confusing business description. A banker I know once put it perfectly: "If I can't explain what this business does in one sentence, it’s a no." Saying your company is in "international consulting" is a huge red flag for them. Get specific. "We provide supply chain management software for UK-based fashion retailers" is clear, credible, and builds instant trust.

Another classic mistake is dragging your feet on communication. When a bank's compliance officer emails you with a question, they're working against a clock. A prompt, detailed response shows you're organised and have nothing to hide. Letting that email sit unanswered for a week can stall your application or, worse, get it flagged as uncooperative.

A rejected application isn't usually a final judgment on your business. Think of it as feedback on how you presented it. Most rejections boil down to a failure to tell a clear, consistent, and verifiable story that fits the bank's risk profile.

Finally, picking the wrong tool for the job can be a costly blunder. Don't try to run your business out of a personal account to save a few dollars. Banks have sophisticated systems to spot this, and it’s one of the quickest ways to get your account frozen and your funds locked. Be upfront about your intentions from day one and get the right type of account. That initial honesty builds a much stronger, more reliable banking relationship for the long haul.

Your Hong Kong Banking Questions Answered

Even with a clear plan, you're bound to have questions when you're looking to open a bank account in Hong Kong. That's perfectly normal. Getting to grips with any new financial system comes with its own set of unique hurdles, and it’s always better to ask now than to find out you made a costly mistake later.

Think of this section as a frank conversation where we tackle the most common questions we hear from entrepreneurs just like you. These aren't theoretical problems; they're the real-world concerns that pop up again and again.

Hong Kong's financial scene is both massive and energetic. To give you a sense of scale, in October 2025, total deposits with authorised institutions clocked in at an incredible 2,452.554 billion USD. For a newcomer, that means you’ve got a huge amount of choice, with over 160 banks and financial institutions vying for your business. The market is liquid and stable, which is great news for anyone setting up shop here. You can dig into the numbers yourself on CEIC Data's page for Hong Kong's total deposit statistics. This robust environment makes the whole process feel a lot less intimidating than it might seem from the outside.

So, let's get into the specifics.

Can I Open a Bank Account in Hong Kong Remotely?

This is, without a doubt, the number one question we get asked. The short answer is: yes, it’s possible, but it really depends on the bank and your specific situation.

Not too long ago, a face-to-face meeting in Hong Kong was an absolute must. That's all changed with the rise of licensed virtual banks. New players like ZA Bank or Mox Bank were built from the ground up for a digital world. They use secure eKYC (electronic Know Your Customer) tech—think video calls and biometric checks—to let you open a personal or SME account from pretty much anywhere.

For the old-guard banking giants like HSBC or Standard Chartered, the story is a bit different. While they've made huge digital strides, a fully remote opening for a brand-new overseas business client is still a rare thing. However, they're known to make exceptions for a few scenarios:

- High-Value Clients: If you're setting up a substantial wealth management or private banking relationship, they tend to roll out the red carpet and offer more flexibility.

- Existing Global Relationships: If your business already has a history with them in another country, they can often fast-track the process and handle things internally.

- Using a Certified Intermediary: This is a big one. Working with a professional firm that the bank knows and trusts can sometimes get you over the line without an in-person visit, as the firm is vouching for your identity.

What Is the Minimum Deposit to Open an Account?

The "minimum deposit" causes a lot of confusion because there's no single, straight answer. The amount can be anything from literally zero to hundreds of thousands of Hong Kong dollars.

It all boils down to the type of account you’re after. For most personal savings accounts, especially with the virtual banks, there is no minimum deposit requirement at all. This makes them incredibly easy to get for individuals and digital nomads.

For business accounts, things get a bit more nuanced.

- Virtual Banks: Usually have very low or no initial deposit requirements for small and medium-sized businesses.

- Traditional Banks: You can expect them to ask for an initial deposit anywhere from HKD 10,000 to HKD 50,000 for a standard business account.

- Premium/Corporate Accounts: For accounts with more advanced services, the minimum deposit and ongoing balance requirements can jump significantly higher.

Here's a pro-tip for business accounts: banks are often less concerned with your initial deposit and far more interested in your projected business turnover. A solid business plan that shows healthy, realistic cash flow is much more powerful than simply dropping a large one-time deposit.

Why Was My Bank Account Application Rejected?

Getting a "no" from a bank is incredibly frustrating, especially when it comes with a vague, copy-paste rejection email. But a rejection isn't a final judgement on your business—it's just feedback that your application didn't tick all the boxes for that specific bank's risk appetite.

From what we've seen, rejections almost always come down to one of these reasons:

- Incomplete or Inconsistent Documents: This is the most common and easily avoidable pitfall. A simple mismatch in addresses or a missing shareholder document will bring the whole process to a screeching halt.

- High-Risk Business Model: Certain industries—like cryptocurrency, trading in high-value goods, or businesses with complicated international ownership structures—are automatically flagged as higher risk by the more conservative banks.

- Unclear Source of Funds: If you can't clearly show where your start-up capital came from with bank statements, loan agreements, or investor contracts, they won't even consider your application.

- Not a Fit for the Bank's Profile: Sometimes, it's really just not a match. A bank might be focused on local manufacturing clients, and your global SaaS start-up just doesn't align with their current customer strategy.

The key is to not take it personally. Use the rejection as a chance to learn, refine your business plan, gather more detailed supporting documents, and do a bit more research to find a bank that actually wants to work with businesses in your industry.

What Are the Alternatives to a Traditional Bank Account?

Let’s be honest: sometimes a traditional bank account isn't the best tool for the job. This is especially true for agile start-ups and international freelancers who need to move fast and keep costs low.

The world of Electronic Money Institutions (EMIs) and multi-currency fintech platforms has completely changed the game. Services like Wise, Airwallex, or Statrys offer incredible alternatives.

Now, these platforms aren't technically banks, but they give you many of the same essential functions:

- Multi-Currency Accounts: You can hold balances in USD, EUR, GBP, and dozens of other currencies without getting hit by terrible exchange rates.

- Fast International Payments: Sending and receiving money across borders is often cheaper and quicker than with traditional wire transfers.

- Digital Onboarding: The sign-up process is almost always 100% remote and can often be done in a single day.

The main trade-off is that EMIs don't offer deposit insurance (like the Deposit Protection Scheme in Hong Kong). However, they are highly regulated and required to safeguard client funds in separate, protected accounts. For managing day-to-day operational cash flow, they are an excellent, and often better, choice for many modern businesses.

Navigating the complexities of international banking is at the heart of what we do. At Lion Business Consultancy Limited, we act as your strategic partner, ensuring you not only open the right account but also build a financial structure that is secure, compliant, and ready for growth. If you need hands-on guidance to secure your banking setup, let's connect and build your global foundation together.