Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

When you start thinking about opening an offshore account, the first question is always the same: where? This isn’t just about picking a location on a map; it’s a strategic move that will shape your company’s financial future and global reach. It’s about building a foundation that can support your ambitions, whether you’re a startup entrepreneur or a seasoned SME owner.

Why Hong Kong Is a Top-Tier Choice for Offshore Banking

Before diving into the nuts and bolts of the application, let’s talk about why a world-class jurisdiction like Hong Kong makes so much sense. We need to look past the generic sales pitches and get to what this choice actually means for your business.

Picture this: you’re running an e-commerce business out of the UK, and you’re ready to expand into Southeast Asia. An offshore account in Hong Kong becomes your financial command centre. Suddenly, you can accept payments in multiple currencies from new customers and pay regional suppliers in their local currency, all without getting hammered by conversion fees. It’s not just banking; it’s about laying a solid financial foundation for global growth.

Let’s break down the key advantages that make a Hong Kong offshore account so attractive.

| Benefit | Description for SMEs & Entrepreneurs |

|---|---|

| Financial Stability | Your funds are held in one of the world’s most secure and well-regulated banking systems, giving you peace of mind. |

| Gateway to Asia | Unrivalled access to Mainland China and ASEAN markets, simplifying trade and investment in the region. |

| Favourable Tax Regime | A simple, low-tax system means you can reinvest more of your profits back into growing the business. |

| Multi-Currency Support | Easily manage transactions in major global currencies, reducing foreign exchange costs and complexities. |

| Global Reputation | A Hong Kong bank account adds credibility and prestige, opening doors with international partners and clients. |

These benefits aren’t just bullet points on a brochure. They translate into real-world advantages that can give your business a serious competitive edge.

A Pillar of Financial Stability

Hong Kong’s reputation is built on an incredibly stable and resilient banking system. The Hong Kong Monetary Authority (HKMA) keeps a tight ship, ensuring banks meet some of the highest international standards for liquidity and capital. This isn’t just financial jargon—it’s your guarantee that your money is in a secure, well-regulated environment.

For an entrepreneur, that stability means you can sleep at night. You can focus on scaling your business without constantly worrying about the political or economic drama that can rock other financial centres. It’s about predictability in an often unpredictable world.

The Ultimate Gateway to Asian Markets

Located at the heart of Asia, Hong Kong is the undisputed gateway to Mainland China and the booming economies of the ASEAN region. If your business involves international trade, manufacturing, or services, this location is a game-changer.

Imagine having an account that makes cross-border transactions, especially those in Chinese Yuan (RMB), incredibly smooth. Hong Kong has the largest offshore pool of RMB in the world, making it the most efficient place to do business with Chinese partners. This unique advantage is precisely why so many international companies choose Hong Kong. If you want to dig deeper, our ultimate guide to opening a Hong Kong offshore bank account has all the details you need.

Hong Kong’s financial dominance isn’t just talk. Projections show it’s on track to overtake Switzerland as the world’s largest offshore wealth hub by 2025, managing an estimated US$2.9 trillion in cross-border assets.

This growth is a direct result of its sophisticated financial infrastructure, investor-friendly rules, and deep connections to Mainland China.

A Simple and Favourable Tax Regime

One of the most powerful draws to Hong Kong is its refreshingly simple, low-tax system. The territory runs on a territorial source principle, a straightforward concept meaning they only tax profits generated within Hong Kong.

For your international business, the advantages are crystal clear:

- No Tax on Foreign-Sourced Income: If your business activities and profits come from outside Hong Kong, you generally won’t pay any Hong Kong profits tax on them.

- No Capital Gains Tax: Selling assets or investments? You won’t be taxed on the profit.

- No VAT or Sales Tax: This keeps your accounting simple and your operational costs down.

- Free Flow of Capital: Move your funds in and out of Hong Kong without restrictions.

This approach allows you to pour more capital back into your business, fuelling the growth you’re working so hard for. It’s a system designed to encourage international commerce, not to penalise it.

Choosing the Right Bank and Jurisdiction

Picking the right jurisdiction and bank is easily the most important decision you’ll make when going offshore. This isn’t a transactional step; you’re choosing a long-term financial partner. It’s not about chasing the lowest tax rate but finding a financial ecosystem that understands your business and can support its global ambitions.

Think about it this way: the ideal banking setup for a commodity trader based in Dubai will look completely different from what a European tech startup needs. The trader might gravitate towards a jurisdiction like Switzerland, famed for its ironclad asset protection and private banking history. The tech startup, however, needs a dynamic hub like Singapore or Hong Kong, where banks understand venture capital, cross-border payment gateways, and the speed of global expansion.

Evaluating Key Jurisdictions

While plenty of countries offer offshore banking, a handful consistently rise to the top for their stability, reputation, and specialised financial services. Hong Kong, Singapore, and Switzerland are the usual suspects, each bringing something different to the table.

- Hong Kong: The undisputed gateway to Mainland China and wider Asia. The banking sector here is built for international trade, making it a natural fit for any business with supply chains or customers in the region.

- Singapore: Known for incredible political stability and a highly respected banking system governed by the strong rule of law. It’s a top-tier hub for wealth management and a fantastic alternative for businesses focused on Southeast Asia.

- Switzerland: The classic choice, synonymous with asset protection and banking privacy. Swiss banks are legendary for their discretion and focus on long-term wealth preservation, which is why they’re so popular with family offices and high-net-worth individuals.

Your business model must be the driving force behind this choice. To help you dig deeper, our guide on the best countries to open an offshore bank account breaks down the pros and cons of each major jurisdiction.

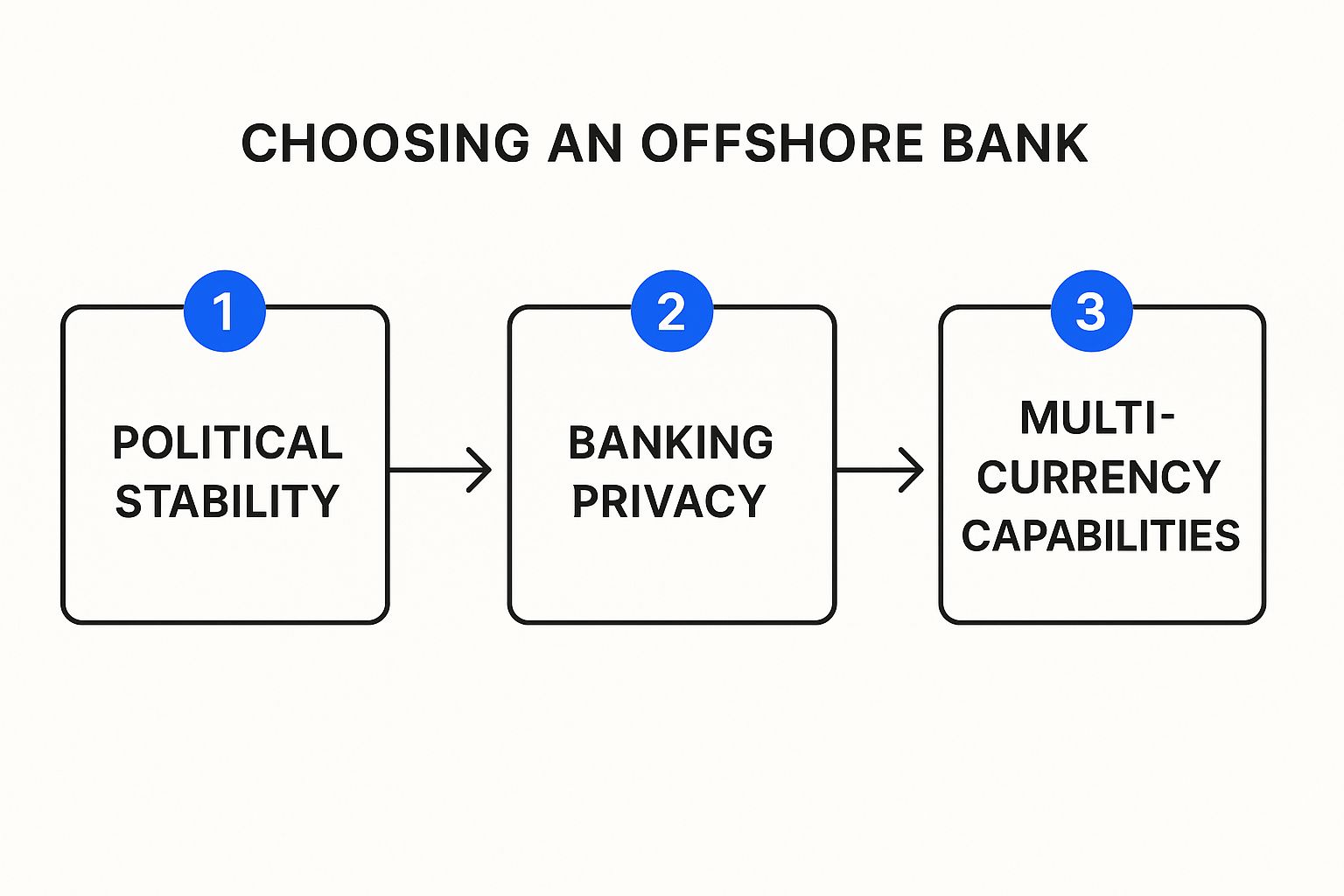

This infographic provides a great overview of the decision-making process for finding the right offshore partner.

The real takeaway here is how interconnected these factors are. You can’t have strong banking privacy or reliable multi-currency services without a foundation of political and economic stability. It all works together.

Big Global Bank vs Specialised Private Bank

Once you have a jurisdiction in mind, the next question is what kind of bank to approach. Do you go with a huge, globally recognised name or a smaller, specialised private bank?

A massive international bank offers a vast network and a predictable suite of services. This is often the right call for a straightforward import-export business that just needs reliable trade finance and a way to process payments from around the world.

A boutique private bank, however, offers a much more personal, relationship-driven experience. They excel at crafting bespoke wealth management strategies and can often be more flexible. A family business looking to manage assets across generations would find this high-touch service indispensable.

The decision isn’t just about services; it’s about culture. A large bank might see you as an account number, while a private bank sees you as a long-term client. Choose the one that aligns with how you want to be treated.

For example, Hong Kong continues to be a dominant global financial centre, with a banking sector that supports a massive volume of offshore activity. Even with global economic headwinds, total banking assets in Hong Kong recently grew by 4.5%, hitting a new high. This growth underscores the increasing demand for offshore banking in the region.

Your Personalised Offshore Banking Checklist

To get this right, you need to be brutally honest about what your business truly needs. Before you even start looking at banks, ask yourself these practical questions:

- What does my business actually do? (e.g., e-commerce, consulting, international trade, holding investments)

- What currencies will I be dealing with most often? (e.g., USD, EUR, HKD, RMB)

- Do I need any special services? (e.g., trade finance, letters of credit, sophisticated investment management)

- What’s my realistic monthly transaction volume and value?

- How important is having a dedicated relationship manager I can call?

Answering these will give you a clear profile of your ideal banking partner, making the search process far more focused and effective.

And remember, banking is just one piece of the puzzle. If you’re planning a full relocation, this comprehensive guide for expatriates preparing to move abroad covers all the other essentials you’ll need to consider. Taking the time to nail this first step is the single best investment you can make in the future of your global business.

Preparing Your Application Documents

This is where the rubber meets the road. Getting your paperwork in order is arguably the most critical part of the entire process, and it’s where most applications get stuck. Think of it less like filling out a form and more like pitching a compelling business proposal.

The bank isn’t just opening an account; they’re vetting a new partner. A messy, incomplete application file sends immediate red flags. But a professionally organised, crystal-clear set of documents? That builds trust right out of the gate and shows them you’re a serious, organised professional. It can make all the difference.

The Core Personal and Corporate Documents

While every bank has its own unique checklist, the foundational documents are pretty much the same everywhere. These are the non-negotiables that prove who you are and establish your company’s legitimacy.

For every single person involved—directors, shareholders, and ultimate beneficial owners (UBOs)—the bank must perform identity and address verification. This isn’t just a box-ticking exercise; it’s a strict requirement under global Anti-Money Laundering (AML) laws.

You’ll almost certainly need:

- A Certified Passport Copy: Not just a photocopy. This means a high-quality copy of the main photo page, officially certified as a true copy by a notary public, lawyer, or certified accountant.

- Proof of Residential Address: This must be recent, usually issued within the last three months. Think utility bills, bank statements, or official government letters that clearly show your name and current home address.

For the company itself, the list gets longer. You’ll have to provide the full suite of corporate documents proving your business is legally registered and in good standing. This means having your Certificate of Incorporation, Memorandum and Articles of Association, and a Register of Directors and Shareholders ready to go.

Crafting a Compelling Business Narrative

Now, let’s move beyond the legal boilerplate. The bank needs to understand what your business does. This is where a well-thought-out business plan is absolutely essential.

Your plan needs to be clear, concise, and answer these key questions:

- Your Business Model: What exactly do you sell? Who are your clients? How does the money flow?

- Your Target Markets: Which countries will you be sending money to or receiving it from?

- Transaction Patterns: Give them a realistic picture of your expected transaction volumes, frequencies, and average amounts.

- Purpose of the Account: Be specific. Why do you need an offshore account in this particular jurisdiction?

This narrative gives the compliance officer the context they need to understand your financial activity. It explains the “why” behind your transactions, which is crucial for their risk assessment.

Just as important is your proof of funds or source of wealth. The bank must understand where the money to start the business and fund the account came from. Whether it’s from personal savings, a business loan, or an investment, be prepared to show the paper trail—personal bank statements, loan agreements, you name it.

Here’s the bottom line: The bank is legally responsible for every single transaction that passes through its systems. When you provide a transparent, detailed story about your business and your funds, you aren’t just filling out a form. You’re actively helping the bank meet its own stringent regulatory duties, which makes them far more likely to say “yes.”

The Crucial Step: Certifying and Apostilling Your Documents

Here’s a common tripwire I’ve seen delay countless applications: document certification. Simply sending a scan of your passport will get your application rejected instantly.

Banks require key documents to be certified or notarised. This means you need a qualified professional, like a notary public or a solicitor, to physically inspect your original document, verify it’s you, and then stamp and sign the copy to attest to its authenticity.

For international banking, you might also need an apostille. This is another layer of verification, recognised by countries that are part of the Hague Convention. It’s essentially a government-issued certificate that authenticates the signature of the official (like the notary) who certified your document.

Getting this wrong is one of the top reasons for applications being delayed for weeks. My advice? Always confirm the bank’s exact requirements for certification and apostilles before you start gathering anything. It will save you an enormous amount of time and frustration.

Essential Documents for Offshore Account Opening

To help you get organised, here’s a quick comparison of the typical documents needed for personal versus corporate accounts. Having these ready will put you way ahead of the game.

| Document Type | Required for Personal Account | Required for Corporate Account | Pro Tip |

|---|---|---|---|

| Certified Passport | Yes | Yes (for all directors/shareholders) | Ensure the certifier’s details are clearly legible. A smudged stamp can cause a rejection. |

| Proof of Address | Yes | Yes (for all directors/shareholders) | Use a document from a reputable source, like a major utility company or a well-known bank. |

| Business Plan | No | Yes | Be specific about your international activities and the currencies you’ll be using. |

| Proof of Funds | Yes | Yes | Provide a clear paper trail showing the origin of your capital. Gaps will raise questions. |

| Corporate Documents | No | Yes | Have these ready from your company formation agent and double-check they show the company is in good standing. |

Getting this documentation stage right from the beginning is the single best thing you can do to ensure a smooth and successful application.

Getting Through Due Diligence and Compliance

So, you’ve put together a stellar application package and sent it off. What now? You’re heading into the due diligence phase. For many, this part feels a bit mysterious, but it’s a straightforward—and mandatory—part of modern international banking. It’s how banks protect themselves and the integrity of the global financial system.

This whole process boils down to two key ideas: Know Your Customer (KYC) and Anti-Money Laundering (AML). Think of these as the bank’s security protocols. They have a legal duty to confirm who you are, what your business does, and that your money comes from legitimate sources. It’s nothing personal; it’s a global standard everyone must follow.

What the Bank Really Wants to Know

During due diligence, a compliance officer is essentially building a profile of your business. They’ll take the documents you provided and cross-reference them with public records and other data to understand any potential risks. They need to get comfortable that your business is above board and fits within their risk tolerance.

Let’s use a real-world case. Imagine an entrepreneur named Sofia who runs an e-commerce business. She sources artisanal goods from Europe and sells them to customers across Asia. When she applies for an account in Hong Kong, the bank’s compliance team will ask a few core questions:

- Who is Sofia? They’ll start by verifying her identity using her passport and proof of address. Simple enough.

- What’s her business model? They will dive into her business plan to get a clear picture of her products, suppliers, and customer locations.

- How will the money move? They’ll look at the expected flow of funds. In Sofia’s case, they’d expect to see payments going out to European suppliers and coming in from Asian customers. If the money trail makes sense, it’s a huge green flag.

Dealing with CRS and FATCA

You’re also going to run into a couple of important acronyms during this stage: CRS and FATCA. Both are international agreements designed to increase tax transparency and stop tax evasion.

- CRS (Common Reporting Standard): This is the global version. Banks in nearly every country automatically report information on accounts held by foreign tax residents back to their home tax authorities.

- FATCA (Foreign Account Tax Compliance Act): This one is specific to the U.S. It requires foreign banks to report any accounts held by American citizens directly to the IRS.

The bottom line is that an offshore account isn’t about hiding money from the taxman. It’s a legitimate tool for international business, and these reporting standards ensure everything stays transparent. For a deeper dive into managing these ongoing duties, check out our guide on how to maintain compliance with a Hong Kong bank account.

A solid grasp of foreign exchange control is also crucial. It’s a fundamental part of managing international finance and keeping your offshore activities compliant.

The key takeaway is this: honesty and transparency are your greatest assets during the due diligence process. A clear, logical explanation of your business will do more to build trust than any other factor.

The reputation of financial hubs like Hong Kong is built on this very foundation of trust and regulatory rigour. We see this reflected in the numbers—total deposits with authorised institutions recently increased by 2.5%. Foreign currency deposits, which are closely tied to offshore banking, also grew by 1.8%, showing that international confidence remains strong.

In the end, getting through due diligence smoothly is all about clear communication. Be ready to answer questions, provide extra details if asked, and approach it as the first step in building a solid relationship with your new bank.

Bringing Your New Account to Life and Keeping It Healthy

Congratulations—the bank has given you the green light. Getting the account approved is a huge milestone, but the work isn’t quite over. Now, the focus shifts from opening the account to using this powerful financial tool effectively.

Think of it like being handed the keys to a high-performance car. The real skill isn’t just getting the keys; it’s learning how to drive it smoothly and safely. Your new offshore account is much the same.

Making That First Deposit

First things first: you need to fund the account. Most banks will give you a specific window, usually 30 to 60 days, to make an initial deposit to officially activate everything.

This first transfer is critical. It must come from an account in the exact same name—whether personal or corporate—that you used on the application. Sending funds from a third-party account right off the bat will raise immediate red flags with the compliance team you just spent weeks satisfying.

Setting Up Your Digital Command Centre

Once your deposit clears, it’s time to set up your online banking. This is your portal for everything from checking balances to wiring funds across the globe.

Banks in reputable jurisdictions don’t mess around with security. You can expect to set up multi-factor authentication (MFA), which often involves:

- A physical security token that generates a new code every time you log in.

- A mobile authenticator app, like Google Authenticator, on your smartphone.

- Biometric verification, such as a fingerprint or facial scan via the bank’s mobile app.

Spend some time getting comfortable with the online platform. Explore the features, find the daily transfer limits, and save the contact number for their international support desk. You don’t want to be scrambling to figure this out when an urgent payment is on the line.

Getting a Handle on the Fee Structure

Offshore banking operates on a different fee schedule than what you might be used to at home. To avoid any nasty surprises, ask for the bank’s schedule of fees and actually read it.

Be on the lookout for common charges like:

- Monthly maintenance fees: Often waived if you keep a certain amount in the account.

- Inward and outward wire fees: Can vary wildly based on the currency and destination.

- Currency conversion fees: Pay close attention to the exchange rate margin the bank takes. It’s often hidden in the rate itself.

For a business that’s constantly moving money internationally, these seemingly small fees can really add up. Knowing the costs upfront helps you manage your finances much more efficiently.

A classic rookie error is to focus only on the big wire transfer fees while ignoring the smaller monthly charges. Smart account management means understanding the entire cost structure. This ensures your offshore account remains a valuable tool, not a surprise expense.

Building a Real Relationship with Your Banker

Don’t treat your new banking relationship as purely transactional. The single best way to keep your account in good standing and steer clear of compliance headaches is to maintain open and proactive communication.

Your relationship manager should be seen as a partner. If your business is about to expand into a new region or you’re expecting a large, unusual payment, let them know before it happens. A sudden, unexplained change in transaction patterns is a textbook trigger for an account review or, worse, a temporary freeze.

Giving them a simple heads-up provides crucial context for the activity on your account. It shows you’re transparent and helps build the long-term trust that’s essential for a healthy offshore banking relationship. This simple habit is probably the most effective thing you can do to ensure your account remains a stable asset for years to come.

Answering Your Top Offshore Account Questions

Even with the best guide, going offshore for the first time naturally brings up questions. As a consultant, I get asked these all the time by entrepreneurs, so let’s cut through the noise and get you the straight answers you need.

Can I Really Open an Offshore Account 100% Online?

This is probably the number one question I hear, and for good reason—who has time to fly around the world just to open a bank account? While many banks have made their initial applications digital, a completely remote opening isn’t always a given.

Top-tier banks in the most reputable jurisdictions often insist on some form of direct identity verification as a non-negotiable part of their Know Your Customer (KYC) process. This might be a scheduled video call with a bank officer or, in some cases, a quick trip to a local branch.

That said, a new breed of fintech-focused institutions is changing the game, making fully remote openings more accessible. If you go this route, you must do your homework on their credibility and regulatory standing.

A good middle ground I’ve seen work well is asking if the bank can send a representative to meet you in your home country. It’s not always possible, but for the right client, some banks will do it. Always clarify the bank’s exact verification policy before you get too deep into the paperwork.

What’s the Real Minimum Deposit for an Offshore Account?

There’s no magic number here; the minimum deposit for an offshore bank account is all over the map. It depends entirely on the country, the bank, and what you plan to do with the account.

To give you a realistic picture:

- A Standard Corporate Account: For a business account in a major hub like Hong Kong or Singapore, expect the initial deposit to be somewhere between US$10,000 and US$50,000.

- Private Banking and Wealth Management: For those looking for more hands-on service to protect and grow their wealth, the price of entry is much higher. You’re typically looking at a starting deposit of US$250,000, and it can easily climb past US$1 million for premium services.

Don’t just focus on the initial deposit. You also need to ask about the minimum ongoing balance. Dropping below this threshold can trigger hefty monthly fees that eat into your capital, so make sure it’s a number you’re comfortable maintaining.

Is It Actually Legal to Have Money in an Offshore Account?

Yes, absolutely. Holding money in an offshore bank account is perfectly legal for countless legitimate reasons, from managing international business transactions and protecting assets to diversifying your investments. The negative reputation comes from the small minority who use these accounts for illegal activities like money laundering or tax evasion.

It all boils down to transparency and proper reporting. Your offshore banking is completely above board as long as you follow your home country’s tax laws and comply with global standards like the Common Reporting Standard (CRS). This simply means declaring the account and any income it generates to your local tax authorities.

Think of it like any powerful tool: it’s not the tool itself that’s illegal, but how you choose to use it.

How Long Does It Take to Open an Offshore Account?

This is where patience is a virtue. The timeline for offshore account opening can feel unpredictable, but preparation on your end can make a massive difference.

If you have all your documents in perfect order and your business is straightforward, you could have an active account in as little as two to six weeks. But honestly, you should plan for potential delays.

Here’s what can slow things down:

- The bank’s internal backlog—you might just be in a long queue.

- A complex company structure with multiple owners or trusts.

- The compliance team coming back with extra questions during their due diligence.

The single best piece of advice I can give you is this: submit a flawless, complete application right from the start. Being organised, transparent, and quick to respond to the bank’s questions shows you’re a serious, low-risk client, and that can often get your application moved to the top of the pile.

Navigating the complexities of global finance requires more than just information—it demands a strategic partner who can anticipate challenges and secure your financial future. At Lion Business Consultancy Limited, we act as your private financial manager, ensuring every step of your international expansion is built on a foundation of security, compliance, and strategic foresight.

Ready to build a truly bankable and protected global business? Contact us today for a private consultation.