Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

Welcome to your practical guide for Hong Kong property tax. If you're an entrepreneur or running a small to medium-sized business, you know that taxes can often feel like a major distraction from what you do best. This guide is here to change that.

Let's get one thing straight from the start: property tax in Hong Kong is not a tax on simply owning property. Instead, it’s a charge on the income you generate from renting it out. This is a game-changer for anyone coming from a country with traditional property taxes.

Getting to Grips with Property Tax

Think of this guide less like a dense textbook and more like a chat with a seasoned advisor. We’re going to skip the confusing jargon and get straight to what matters for business owners who need to handle their tax obligations in one of the world's most dynamic property markets. The goal is simple: to give you the confidence to manage your tax duties efficiently, without the usual headache.

For many international business owners, the term "property tax" conjures up images of a hefty annual bill based on a property's market value. Hong Kong flips that concept on its head. It’s a direct tax on your rental income stream, which makes it feel much more like an income tax than a wealth tax. This crucial distinction shapes everything from how you structure your lease agreements to your wider investment strategy.

The Core Concepts You Need to Know

To get started, let's nail down two key ideas that form the foundation of everything we'll discuss:

- Standard Tax Rate: This is the flat percentage that gets applied to your taxable rental income. No complex brackets, just one straightforward rate.

- Net Assessable Value (NAV): This isn't just your gross rent. Think of it as your rental income after the government has given you a discount. It’s the final number you’re taxed on after subtracting all legally allowed deductions.

Grasping these two concepts is the first real step to mastering your liabilities. It's a completely different system from how a company's general profits are taxed, which you can explore in our overview of Hong Kong Profits Tax.

The government has streamlined the process with a simple online portal where you can manage all your property tax affairs.

This portal acts as a one-stop-shop for e-filing, making payments, and finding the forms you need, which helps centralise the whole process and cuts down on paperwork.

In Hong Kong, property tax is charged at a flat standard rate of 15% on the net assessable value of your rental income. This rate has been consistent since the 2008/09 assessment year, which brings a welcome level of predictability for landlords and investors.

Your NAV is calculated by taking your gross rental income and then subtracting allowable deductions. The big ones are a standard 20% allowance for repairs and outgoings and any government rates you've paid as the landlord. This simple formula makes it relatively easy for property owners to forecast their tax bills.

How to Calculate Your Property Tax Liability

Figuring out your property tax in Hong Kong is surprisingly straightforward once you get the hang of it. Many business owners I’ve spoken to anticipate a complicated mess of spreadsheets, but the Inland Revenue Department (IRD) has a clear, predictable formula. Let's break it down so you can forecast your tax obligations with confidence and avoid any nasty surprises.

The entire calculation hinges on one critical number: the Net Assessable Value (NAV). Just think of this as your "taxable rental income." It isn't the raw rent you collect; it's the amount left after a few key deductions are made. This NAV is the foundation for your final property tax bill.

Determining Your Assessable Value

First things first, we need to find your property's assessable value. For any given tax year, this starts with the total rental income you've actually received. This is your top-line figure before we start subtracting anything.

From there, you get to apply the deductions the IRD allows. The most significant one is a flat-rate allowance designed to cover the cost of repairs and general upkeep, saving you a ton of administrative work.

The IRD gives every landlord a standard deduction of 20% from their net rental income (after subtracting any rates you paid on behalf of your tenant). This is a huge time-saver. It means you don't have to keep a shoebox full of receipts for every minor repair.

This flat-rate approach keeps things beautifully simple. Whether you spent a fortune on renovations this year or didn't touch a thing, that 20% deduction is yours to claim. The process is always the same: start with your gross rent, make a few subtractions, and then apply the allowance. Having a good grasp of the principles of property valuation can also give you a better sense of how your property's value is perceived in the wider market.

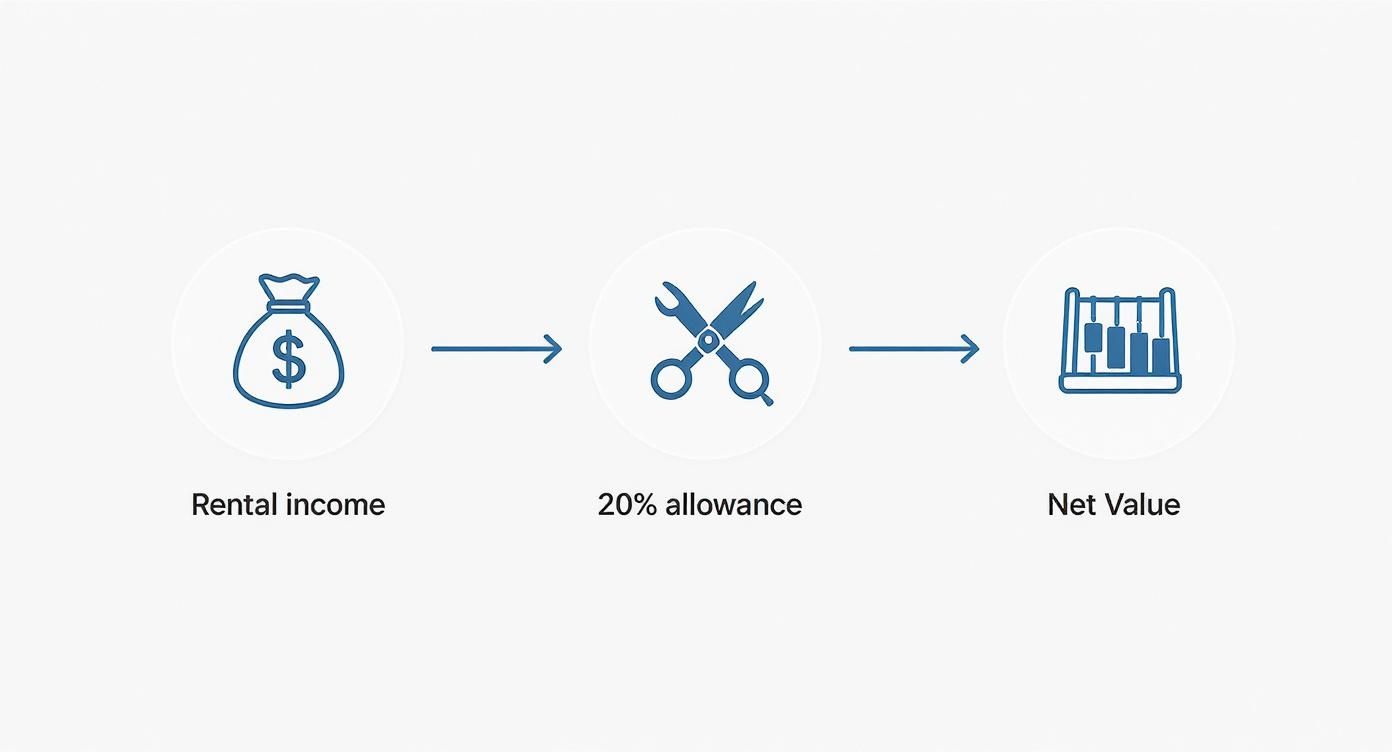

This simple flow chart gives you a bird's-eye view of how the numbers come together.

As you can see, you move from your total rent to your net assessable value by applying deductions and the standard 20% allowance. From there, calculating your final tax bill is just one simple step away.

A Practical Case Study

Let's walk through a real-world example to see how this plays out. Imagine you own a small commercial space in Sheung Wan that you're leasing to a local design studio.

- Annual Rental Income: The studio pays you HKD 40,000 a month, which works out to HKD 480,000 for the year.

- Government Rates: As the landlord, you've agreed to cover the government rates, which come to HKD 15,000 for the year.

- Unrecoverable Rent: Unfortunately, the studio had a tough quarter and missed one month's rent (HKD 40,000), which you've had to write off as bad debt.

Here’s the step-by-step calculation for your property tax:

- Start with Gross Rent: HKD 480,000

- Subtract Unrecoverable Rent: HKD 480,000 – HKD 40,000 = HKD 440,000

- Subtract Rates Paid by Landlord: HKD 440,000 – HKD 15,000 = HKD 425,000

- Apply the 20% Standard Allowance: HKD 425,000 x 20% = HKD 85,000

- Calculate Net Assessable Value (NAV): HKD 425,000 – HKD 85,000 = HKD 340,000

- Calculate Final Property Tax: HKD 340,000 x 15% (Standard Rate) = HKD 51,000

This shows how different factors—like who pays the rates and whether you had any bad debt—can directly influence your final tax bill.

Sample Property Tax Calculation Scenarios

To give you an even clearer picture, this table illustrates how the calculation works across a few different common scenarios.

| Scenario | Annual Rental Income (HKD) | Rates Paid by Landlord (HKD) | Net Assessable Value (NAV) | Property Tax Payable (15% of NAV) |

|---|---|---|---|---|

| A: Tenant Pays Rates | 240,000 | 0 | 192,000 | 28,800 |

| B: Landlord Pays Rates | 240,000 | 10,000 | 184,000 | 27,600 |

| C: Higher Income | 600,000 | 25,000 | 460,000 | 69,000 |

| D: Unrecoverable Rent | 600,000 (with 50k lost rent) | 25,000 | 420,000 | 63,000 |

As you can see, details like who pays the rates have a direct impact on your Net Assessable Value before the standard 20% allowance is even applied. By understanding this formula, you can accurately plan for your property tax in Hong Kong and keep your finances in check.

Navigating the Property Tax Filing Process

Filing your property tax return can seem like just another task on a long to-do list, but in Hong Kong, the system is designed to be surprisingly manageable. Think of it less as a complex puzzle and more as an annual checklist. Once you know the key documents and deadlines, it simply becomes a routine part of your business operations.

The whole process kicks off when the Inland Revenue Department (IRD) sends out the property tax returns, usually right at the start of the financial year. Depending on whether you're a sole owner or part of a corporation, you'll receive a specific form. Familiarising yourself with that form is your first step.

The Key Forms You Will Encounter

For most property owners, it all starts with one of two documents. These forms are basically the IRD’s way of asking: “So, how much did you make in rent last year?”

- Form BIR57: This one is the Property Tax Return for Jointly Owned or Co-owned Property. If you share ownership with a spouse, a business partner, or another party, this is the form for you. It's where you'll declare the total income and each owner's respective slice.

- Form BIR58: Known as the Notice of Rent, Rates, and Other Particulars of Property, this form usually goes to new owners or when the IRD needs fresh details about a tenancy agreement.

Don't let the official jargon throw you. At their core, these are just tools for reporting your rental income and making sure you get all the deductions you're entitled to.

Your Filing Timeline and Deadlines

When it comes to taxes, timing is everything. The IRD typically issues property tax returns around the first working day of April. Once that form lands on your desk, the clock starts ticking—you usually have just one month to complete and send it back.

Miss that deadline, and you could be looking at an estimated assessment from the IRD, not to mention potential penalties. It’s a date you’ll want to circle on your calendar. For a better sense of how this fits into the broader financial year, have a look at our guide on the tax year in Hong Kong.

The real takeaway here is to act the moment you receive your tax return. Gather your documents and start the process early. Last-minute scrambles are where simple mistakes happen, and they can be costly.

Good organisation is your best friend in avoiding any compliance headaches. In fact, you should have your documents ready even before the form arrives.

Gathering Your Essential Documentation

A painless filing experience boils down to one thing: good record-keeping. The IRD can ask for proof, so having your paperwork in order isn't just a good habit—it's essential.

Here’s a quick checklist of what you should have ready to go:

- Tenancy Agreements: Keep a signed copy of the current lease for each property. This is the foundation for everything.

- Rental Receipts or Bank Statements: You need a clear trail of all rental payments you've received. Clean bank statements are perfect for this.

- Proof of Rates Paid: If you, the landlord, covered the Government Rates, hold onto those receipts. You can claim this as a deduction.

- Records of Unrecoverable Rent: In the unfortunate event a tenant didn't pay, you'll need to show you made a real effort to collect the debt.

Once you have these documents lined up, you're all set to decide how you'll file. The IRD offers both the old-school paper method and a convenient digital option, giving you the flexibility to choose what works best for your business.

Uncovering Key Exemptions and Tax Reliefs

Most entrepreneurs and SMEs see the flat 15% property tax and assume that’s the end of the story. But stopping there can be a costly mistake. Hong Kong's tax system has built-in relief routes that can seriously cut your tax bill, but only if you know where to look.

Think of it like choosing a route on a map. The standard property tax is one path, but alternatives—like Personal Assessment for individuals or Profits Tax for companies—can lead to a much better financial outcome. It all comes down to knowing which option makes the most sense for your specific situation.

For Individual Property Owners: The Personal Assessment Election

If you're an individual earning rental income, one of the most powerful tools in your arsenal is the option to elect for Personal Assessment. This isn't a typical exemption; it’s a completely different way of calculating what you owe.

When you opt for Personal Assessment, you lump your rental income together with all your other personal income, like your salary. Instead of being taxed at a flat 15%, this combined income is taxed at progressive rates, which start as low as 2%.

So, when is this a smart move? It’s often a winner if:

- Your total income puts you in the lower tax brackets.

- You have deductions you can't claim against property tax directly, like mortgage interest payments.

- You’ve had business losses that you can use to offset your rental income.

Choosing Personal Assessment can transform a simple tax calculation into a strategic financial win, potentially saving you a significant chunk of cash.

For Corporate Property Owners: Profits Tax vs. Property Tax

For companies that own and rent out property, the situation is different but just as strategic. A corporation's rental income usually falls under Profits Tax, not Property Tax. This is a critical distinction with big implications for your bottom line.

While the standard Profits Tax rate (16.5% for corporations) is a touch higher than the property tax rate, it unlocks a much wider range of deductible expenses. Under Profits Tax, you can deduct the actual costs you incurred to generate that rental income.

This means you can go far beyond the fixed 20% repair and outgoings allowance under Property Tax. Instead, you can claim for real-world costs like repairs, management fees, and other direct expenses, which often add up to more than that standard allowance.

This is especially valuable for businesses that actively manage their properties and have higher running costs. To see how this fits into a broader corporate tax plan, it’s worth understanding how to handle an offshore profits exemption claim in Hong Kong. Making the right choice here ensures your tax strategy is as sharp as your business operations.

Staying Ahead in the Current Tax Environment

Keeping up with Hong Kong's fiscal policy is essential for smart tax planning. For example, the government held the property tax rate steady at 15% in its 2025-26 budget, which was welcome news for property owners. However, other changes were made, like adjustments to stamp duty on property sales, which affect the cost of transactions. While these don’t change the property tax calculation itself, they show how quickly the landscape can evolve.

At the end of the day, finding savings requires a proactive mindset. To get the best possible outcome, you should explore the various Real Estate Investment Tax Benefits available and see how they could apply to your portfolio. That’s what separates passive property owners from savvy investors who truly maximise their returns.

Common Mistakes and Proactive Tax Planning Tips

When it comes to property tax in Hong Kong, the best defence is a good offence. Too often, busy entrepreneurs treat tax as a reactive chore—only dealing with problems once they pop up. This section is all about flipping that script, helping you get ahead of the game by sidestepping common mistakes and leveraging smart, legitimate strategies.

Many of the most expensive errors we see are surprisingly simple. They usually start as small oversights that, left unchecked, can grow into significant financial headaches. By understanding these common pitfalls, you can build a much stronger financial foundation for your property investments.

Avoiding Common Filing Errors

The difference between a smooth tax season and a compliance nightmare often boils down to preparation. A few key issues consistently trip up property owners, but with a bit of foresight, they are all entirely avoidable.

Keep an eye out for these top mistakes:

- Miscalculating Assessable Value: This is a classic. Landlords often forget to deduct the Government Rates they've paid before applying the standard 20% allowance. It’s a small slip-up that inflates your Net Assessable Value and, in turn, your tax bill.

- Poor Record-Keeping: If your records for tenancy agreements, rental income, and vacancy periods are a mess, you're asking for trouble. The Inland Revenue Department (IRD) can request these documents at any time, so having organised files isn't just good practice—it's essential for compliance.

- Missing Filing Deadlines: The IRD is not flexible on deadlines, which are usually one month from the date the return is issued. Miss it, and you could face penalties and an estimated assessment that is almost always higher than what you actually owe.

The guiding principle is simple but powerful: treat your property tax paperwork with the same rigour you apply to your core business operations. An organised system prevents costly errors and ensures you never pay a dollar more than you legally have to.

This proactive approach is particularly crucial in Hong Kong’s fast-moving fiscal environment. While the 15% property tax rate is famously stable, the wider tax system can see adjustments that indirectly impact property owners. Staying alert is key.

Strategic Tax Planning for Property Owners

Once you have the basics of compliance down, you can start thinking strategically. This isn't about finding secret loopholes; it's about making smart, informed decisions that legally reduce your tax liability. And good planning begins long before your tax return is even due.

Take your tenancy agreements, for instance. Clearly stating who is responsible for paying Government Rates directly affects your final tax calculation. If you, the landlord, pay them, it becomes a deductible expense before the 20% allowance kicks in, ultimately lowering your tax bill.

Timing major expenses can also be a strategic lever. Although the standard 20% allowance covers most repairs, if you own the property through a corporation and are taxed under Profits Tax, scheduling significant renovations can impact your deductible expenses for that financial year.

On a broader scale, Hong Kong’s overall tax-to-GDP ratio has been trending downwards, falling to 13.0% in 2023 from 14.1% the previous year. This reflects various fiscal adjustments, but property tax remains a vital revenue stream thanks to the city's high real estate values. The IRD’s consistent application of the 15% tax on rental income provides stable revenue, highlighting just how important this tax is to Hong Kong’s economy. You can dive deeper into these fiscal trends by reading the full report from the OECD.

Ultimately, proactive planning changes property tax from a chore you dread into a manageable—and even optimisable—part of your business finances.

Got Questions About Hong Kong Property Tax? We’ve Got Answers.

Even the clearest guides can leave you with a few specific questions. That’s completely normal. This section tackles the most common queries we hear from business owners and investors about property tax in Hong Kong. Think of this as our chance to sit down and clear up any final bits of confusion, so you can handle your tax obligations with total confidence.

What’s the Real Difference Between Property Tax and Rates?

This is, without a doubt, the question we get asked the most. It’s easy to mix them up, but they are two completely different taxes serving different purposes.

The simplest way to think about it is this: Rates are like a city subscription fee. You're paying for services that benefit everyone, like public lighting and road maintenance. It's a tax on the occupation of a property, calculated at a flat 5% of its rateable value. Every property owner pays this, whether the property is sitting empty, rented out, or used personally.

Property Tax, on the other hand, is a tax purely on income. It only kicks in when you actually lease your property and start collecting rent. The government then charges a standard rate of 15% on your net rental income.

So, to boil it down:

- Rates: Everyone pays. It's the cost of having the property.

- Property Tax: Only landlords earning rent pay. It’s a tax on the income generated.

Can I Deduct My Mortgage Interest from Property Tax?

A very sharp question, and one that gets to the heart of tax strategy. The short answer is no, not directly on a standard property tax return. But there's a powerful workaround.

Here's why you can't deduct it directly: the Inland Revenue Department (IRD) automatically gives every landlord a generous 20% statutory allowance for repairs and outgoings. This flat-rate deduction is a catch-all, meant to cover all your expenses—mortgage interest, management fees, repairs, you name it—without you having to track every last dollar.

However, if you're an individual owner, you have another option: electing for Personal Assessment. This is where you can be strategic. By choosing this route, you lump your rental income together with your other earnings (like your salary). Under this combined assessment, you can deduct your actual mortgage interest payments. For landlords with high interest costs, this can often lead to a much smaller tax bill overall. It's something every individual property owner should look at every single year.

What Happens If I Own a Property with Someone Else?

Co-owning property is incredibly common, whether with a business partner or a family member. The tax system is set up to handle this fairly and transparently.

If you're a joint owner or a tenant in common, the IRD splits the tax liability based on your ownership percentage. When you fill out your tax return (Form BIR57), you’ll need to report the total rental income the property earned, and then state your share.

For instance, if you own 60% of a property and your partner owns 40%, the IRD won't send one bill. They'll issue two separate assessments: one for you based on 60% of the net income, and one for your partner based on their 40%.

The key here is communication. It is absolutely crucial that all co-owners report the same total income and ownership figures. Any mismatch is a red flag for the IRD and can lead to questions, delays, and unnecessary headaches.

Do I Still Pay Property Tax If My Property Was Empty?

Nope. If your property was vacant and you weren't earning any rent from it, you don't owe any property tax for that period.

Remember, property tax is a tax on income. No income, no tax. Simple as that.

When you fill out your return, you only declare the rent you received for the months it was actually tenanted. If there was a two-month gap between tenants, for example, you just leave that income out of your calculation. You’re only taxed on the money you actually brought in.

One critical thing to remember, though: you are still on the hook for Government Rates for the whole year. Rates are a tax on the property itself, not its income. Your obligation to pay them doesn't stop just because the property is vacant. Keeping this distinction in mind is vital for accurate budgeting.

Conclusion

Navigating the specifics of property tax in Hong Kong requires a partner who understands the nuances of both local compliance and international business structures. At Lion Business Consultancy Limited, we provide the hands-on, strategic advisory that entrepreneurs and SMEs need to operate with confidence.

From optimising your tax position to securing your banking and protecting your assets, we act as your private financial manager. If you're ready for a partnership that aligns with your long-term expansion goals.