Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

For any entrepreneur with an eye on the world stage, opening a business account in Hong Kong isn't just a box to tick—it's the foundational move that turns global ambition into reality. Think of it as the key that unlocks seamless international trade, elevating your business from a local player to a genuine global contender.

Your Gateway to Global Trade

Picture this: your business is taking off, but every time you try to transact with an international client or supplier, you hit a brick wall. Payments are sluggish, eaten away by high fees, and tangled up in bureaucratic red tape. This isn't a rare scenario; it's a frustratingly common story for businesses whose growth is being held back by banking friction.

This is exactly where a Hong Kong business account flips the script. It transforms that frustrating barrier into your most powerful strategic tool. You’re not just getting an account number; you're plugging your business directly into the central nervous system of global commerce.

Why Hong Kong is Still a Financial Powerhouse

Even with all the shifts in the global economy, Hong Kong holds its ground as a top-tier financial centre. There are solid, practical reasons for this that directly benefit your business. Think of it like choosing the right operating system for your company’s financial future—one engineered for stability, speed, and reliability.

The core advantages are clear:

- A Stable, Freely Convertible Currency: The Hong Kong Dollar (HKD) is pegged to the US Dollar, giving you a predictable and secure medium of exchange for international deals. No sudden currency shocks to worry about.

- Unrestricted Capital Flow: Hong Kong has no foreign exchange controls. This is a game-changer. You can move money in and out of your account without restriction, which is absolutely critical for managing cash flow when you operate across borders.

- Strategic Position in Asia: It’s the perfect financial bridge between Mainland China and the rest of the globe, offering unmatched access to the booming Asian market.

A huge part of the appeal is how effortlessly a Hong Kong account handles money coming from all over the world. If you're dealing with payments from multiple countries, you need a system that makes it simple. For a deeper dive into the mechanics, check out a complete guide on how to accept international payments, which is packed with practical advice.

It's More Than an Account, It's Access

The real strength of Hong Kong's banking sector goes far beyond simple transactions. Recent statistics show why opening a business account in Hong Kong is still a cornerstone of regional treasury management. In the first half of a recent fiscal year, total deposits with authorised institutions jumped by 7.6%, with Hong Kong dollar deposits alone climbing 7.0%.

For a small or medium-sized enterprise, what these numbers really mean is access. You’re tapping into a deep pool of capital and a very active credit market. This directly impacts your ability to secure working capital, trade finance, and foreign exchange facilities when you need them.

This robust financial environment means your business isn’t just opening an account; it's gaining access to a mature ecosystem of financial products designed to support growth and international trade.

At the end of the day, choosing Hong Kong is a strategic play. It’s about picking a jurisdiction that is fundamentally built to support your global vision, ensuring your financial operations can be as agile and borderless as your business needs them to be.

Choosing the Right Banking Partner for Your Business

Picking where to open your business account in Hong Kong isn't just a box-ticking exercise. It’s one of the most important strategic decisions you’ll make, and it will directly impact how easily your company operates for years.

Think of it like choosing a vehicle for a cross-country road trip. Are you hauling heavy cargo and need a powerful truck, or are you zipping through city traffic and need a nimble electric car? The right choice depends entirely on your business model and where you plan to go.

Get it wrong, and you’ll face constant friction: surprise fees for essential services, a clunky online portal that wastes your time, or a lack of support for the payment gateways your customers actually use. But the right banking partner? They become a silent engine for growth, making everything run so smoothly you barely notice they’re there.

The Three Tiers of Hong Kong Banking

The Hong Kong banking scene can be broken down into three main categories. Each serves a different kind of business, and knowing which is which is the first step to finding your ideal fit.

-

The Global Giants (e.g., HSBC, Standard Chartered): These are the heavy-duty haulage trucks of the banking world. They’re built for scale, complexity, and serious international trade. If your business deals with letters of credit, trade finance, or moving large sums across continents, these institutions have the rock-solid infrastructure and reputation you need. The trade-off? They often demand higher minimum balances and have a more bureaucratic, paper-heavy onboarding process.

-

The Local Champions (e.g., Bank of East Asia, Hang Seng Bank): These banks possess a deep, nuanced understanding of the local and regional market. They tend to be more flexible and relationship-driven, offering a personal touch that the global behemoths can sometimes lack. They are a fantastic choice for businesses with a major operational focus on Hong Kong and the Greater Bay Area.

-

The Digital Disruptors (Virtual Banks & EMIs): These are the agile, zippy electric cars of finance. Built from the ground up for the digital economy, providers like ZA Bank or Airwallex are perfect for e-commerce sellers, tech startups, and consultants. Their strengths lie in fast, low-cost multi-currency transactions, easy API integrations with platforms like Stripe and Shopify, and a completely remote sign-up process. They are all about speed and user experience, but they probably won’t offer the complex trade finance products you’d find at a traditional bank.

Key Factors to Guide Your Decision

Once you’ve identified the right category, it’s time to look at the specific features that will affect your day-to-day operations. After all, a slick mobile app is worthless if it can’t handle the currencies you actually trade in.

Drill down into these critical factors:

- Multi-Currency Support: Can you hold, receive, and send money in the currencies your clients and suppliers use? Don’t just check if they offer it; look closely at the foreign exchange (FX) rates and transfer fees. Seemingly small percentages can bleed significant cash from your bottom line over a year.

- Digital Platform Usability: Is the online banking portal intuitive, or will it be a daily source of frustration? A poorly designed interface that makes it hard to execute payments, download statements, or manage users will cost you countless hours in administrative headaches.

- Integration Capabilities: How well does the account play with the other tools in your tech stack? For an e-commerce business, seamless integration with Stripe or PayPal isn't a "nice-to-have," it's essential. For others, connecting directly to accounting software like Xero can save days of manual reconciliation work each month.

- Access to Credit and Finance: If you think you might need working capital, trade finance, or business loans down the road, building a relationship with a traditional bank and a dedicated manager is often the smarter long-term play.

Your goal is to find a perfect alignment between your business model and the bank's core strengths. A mismatch here will create unnecessary operational headaches down the line, pulling focus away from what really matters—growing your business.

To get a clearer picture of all the players in the market, our team has put together a comprehensive list of banks in Hong Kong for you to review.

Beyond the bank itself, remember to consider other essential services that make global business possible. For example, solid communication tools are vital; looking into the best VoIP services for small businesses can ensure you stay connected with clients and partners anywhere in the world. This holistic approach ensures every part of your operational infrastructure is set up for success.

Your Essential Document Checklist for a Smooth Application

Let's be honest: the paperwork for opening a business account in Hong Kong can feel like the biggest hurdle. It’s easy to get bogged down and see it as just a mountain of bureaucracy. But I find it helps to look at it differently. You're not just filling out forms; you're telling the bank your business's "Compliance Story."

The goal is to paint a crystal-clear picture of who you are, what your business does, and why the money moving through your account is legitimate. If you get this story right from the get-go, you sidestep most of the frustrating delays and put yourself on the fast track to approval.

Why All the Paperwork?

Every single document the bank asks for has a purpose. They aren't trying to make your life difficult, I promise. They're legally required to check every box under strict anti-money laundering (AML) and know-your-customer (KYC) rules. When you understand the 'why' behind each request, the whole process shifts from a chore to a strategic exercise.

Take a Certificate of Incumbency, for instance. It isn't just another form. It’s the official document that proves who has the legal authority to sign papers and make decisions for the company. A detailed Business Plan isn’t just about your vision; it shows the bank you have a real commercial purpose and that the types of transactions you expect are logical and above board.

Core Documents for Hong Kong Limited Companies

If you've set up a limited company—which is what most international entrepreneurs do—your checklist will be a bit longer. Your compliance story needs the backing of official corporate records.

Here's a rundown of what pretty much every bank will ask for:

- Certificate of Incorporation & Business Registration Certificate: Think of these as your company's birth certificates. They prove it legally exists and is properly registered with the Hong Kong government.

- Articles of Association: This is your company's internal rulebook. It lays out how the business is run, the rights of shareholders, and the duties of directors, giving the bank a clear view of who's in charge.

- Director & Shareholder ID: You’ll need pristine, certified copies of passports and a recent proof of address (like a utility bill or bank statement) for every director, major shareholder (typically anyone with 10-25% ownership), and the Ultimate Beneficial Owners (UBOs).

- Company Structure Chart: A simple diagram is often the best way to show the ownership hierarchy. This is especially important if you have other companies as shareholders or a multi-layered structure. It gives the bank a quick, visual map of who ultimately calls the shots.

A quick note: many of these documents need to be certified. Getting this right is crucial, as incorrect certification is a common reason for rejection. If you're unsure, it's worth reading up on what constitutes a proper true and certified copy in our guide.

I always tell my clients to think of their document package as a professional pitch. A complete, neatly organised submission tells the bank you’re a serious, low-risk client—exactly the kind they want to work with.

Tailoring Your Application for Success

Beyond the standard documents, the quality of your supporting information can make or break your application, particularly if you're not a Hong Kong resident.

- Craft a Compelling Business Plan: This is where you tell your story. Don’t just hand over a generic template. Clearly explain your business model, who your customers are, where your suppliers are located, and what kind of transaction volumes you expect. The more specific, the better. If you run an e-commerce store, list the main countries you ship to. If you’re a consultant, describe the industries your clients are in.

- Provide Substantial Business Proof: You need to show your business is a real, operating entity. This could be anything from signed client contracts and supplier invoices to a professional website or active corporate social media profiles. The more tangible evidence you can provide, the stronger your case becomes.

- Gather Valid Proof of Address: This is a surprisingly common tripwire. Make sure the document is recent (usually within the last three months), clearly shows your full name and residential address, and comes from a reputable source like a government agency, a utility company, or another established bank.

By meticulously preparing each document and understanding its role in your compliance story, you’re no longer just a passive applicant. You become a proactive partner in the process. This approach doesn't just get your business account in Hong Kong opened faster; it starts your relationship with your new bank on a foundation of trust.

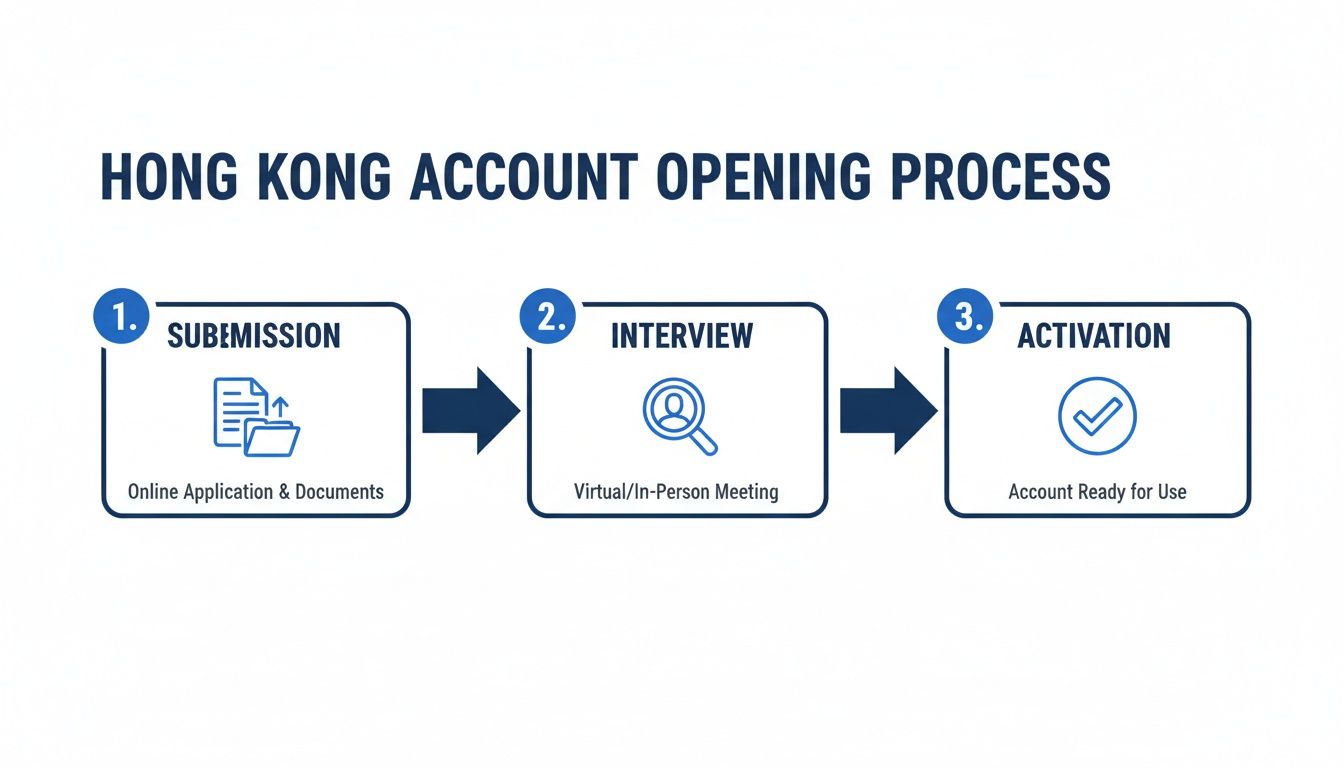

Your Step-by-Step Guide to Opening the Account

Trying to open a business account in Hong Kong can sometimes feel like you’ve been thrown into a maze with no map. But it’s not as chaotic as it seems. Once you know the stages involved, the path becomes much clearer. Think of it not as a series of random obstacles, but as a structured process where you and the bank get to know and trust each other.

The exact steps will differ depending on where you go. A big traditional bank will likely want you to come in for a chat, whereas a digital bank lets you do everything from your laptop. But no matter which you choose, the core milestones are the same: you make contact, you submit your application, you have the crucial compliance interview, and then, finally, your account goes live.

Stage 1: The First Contact and Application Pack

It all starts the moment you pick a bank and kick off the application. With old-school banks, this usually means calling them or dropping by a branch to pick up the right paperwork. For the digital players, it’s often as easy as hitting a "Get Started" button online.

This is your moment to hand over that folder of documents you’ve so carefully put together—think of it as your company's "Compliance Story." A complete, well-organised submission is your first chance to make a good impression. If it’s missing anything, you've just given them a reason to put your file at the bottom of the pile, and that's the number one cause of delays.

Stage 2: The All-Important Compliance Interview

This is the big one, and it's where most people get tripped up. It could be a face-to-face meeting across a desk or a video call with a compliance officer. The whole point of this interview is for the bank to confirm that the story you told on paper is real. They're not trying to trick you; they’re just doing their job.

During this conversation, the banker is looking for three main things:

- Consistency: Does what you're saying now line up perfectly with your business plan and documents? Even a tiny inconsistency can look like a red flag.

- Clarity: Can you clearly explain what your business does, who your customers and suppliers are, and what your cash flow will look like? If your answers are vague, they'll get suspicious.

- Legitimate Purpose: Do you have a solid, believable reason for wanting a business account in Hong Kong? You need to show them there's a genuine business need connected to the city.

My best advice for this stage is simple: know your business inside and out, and be transparent. The compliance officer wants to approve you, but you have to give them every reason to feel confident in your business.

Stage 3: Account Activation and What to Expect on Timelines

Once you’ve aced the interview and the bank has finished its background checks, you’ll get the good news: your account is approved. Getting it activated usually just involves wiring over an initial deposit and setting up your online banking login.

Now, let’s talk about how long this all takes, because this is where reality can bite. For a modern digital bank or EMI, the whole thing can be over in a few business days if your application is straightforward. With the big traditional banks, you're looking at a longer wait, typically two to four weeks for a well-prepared case. If your company structure is a bit unusual or your paperwork is messy, don't be surprised if it drags on for several months.

The rise of fintech has really shaken things up. Hong Kong's status as a financial hub is increasingly being driven by technology. With over 1,100 fintech firms and eight fully licensed digital banks, the entire corporate banking scene is changing. Initiatives like the Commercial Data Interchange have already handled over 50,000 loan applications by connecting banks directly with data sources, proving how tech is making finance more accessible. You can find more details about Hong Kong's integration of fintech in capital markets on hkex.com.hk.

While you can certainly go it alone, this journey doesn't have to be a solo mission. Partnering with a specialist firm like Lion Business Co. is like having a seasoned guide who knows the shortcuts, anticipates the bank's questions, and helps you move through each stage smoothly. It can turn a frustrating, months-long ordeal into a simple, predictable process.

How to Avoid Common Pitfalls and Account Freezes

Getting your business account in Hong Kong open is a huge win, but it’s not the finish line. Far from it. The real work begins now: building a healthy, trusted relationship with your bank. Think of it less as a one-time transaction and more as the start of a long-term partnership where consistency and clear communication are everything.

Many entrepreneurs live with a nagging fear: what if the bank freezes my account? It’s a completely valid worry. A frozen account can grind a thriving business to a halt overnight. But here’s the good news—the vast majority of these situations are entirely preventable. They almost always boil down to a simple breakdown in communication or business activity that looks strange to a bank's compliance software.

This infographic shows the typical path to getting your account up and running, but keeping it that way means learning to see things from the bank's point of view.

Each of these steps—from submitting documents to the interview and finally activating the account—helps the bank build a picture of your business. This picture becomes their baseline for what "normal" activity looks like for you.

Understanding the Bank's Red Flags

Banks aren't trying to catch you out personally. They use sophisticated systems designed to spot unusual patterns that might signal money laundering or other illegal activities. These systems are just pattern-recognition machines. Your job is to make sure your transaction patterns match the "Compliance Story" you told them in your application.

Here are the most common triggers that will get your account flagged for a review or, worse, a freeze:

- Sudden, Large Incoming Transfers: If your account normally handles transactions under $10,000, a sudden wire for $250,000 will set off alarm bells. Expecting a big payment? A quick heads-up to your bank manager can prevent a lot of headaches.

- Erratic Transaction Patterns: A string of small, regular payments followed by one huge transfer out to a new third party can look like a textbook money laundering technique called "layering."

- Transactions with High-Risk Jurisdictions: Every bank has a list of countries considered high-risk. Sending or receiving money from these places without a crystal-clear, well-documented business reason is a surefire way to trigger an alert.

- Mismatched Business Activity: You told the bank you're a software consultant, but now your account is receiving payments for imported textiles. The system will immediately flag this as an inconsistency.

The rules behind this are known as AML (Anti-Money Laundering) and KYC (Know Your Customer). Don’t think of them as obstacles. See them as the framework for building trust. When you operate transparently, you're proving to the bank that you're a low-risk, reliable partner.

Proactive Steps to Keep Your Account Healthy

The secret to keeping your account in good standing is simple: proactive communication and meticulous record-keeping. The goal is to never surprise your bank.

This diligence is especially critical in Hong Kong. The city manages around US$4 trillion in assets, and roughly 66% of that comes from international investors. This massive influx of foreign capital means banks are under intense regulatory pressure to be vigilant. By keeping your paperwork in perfect order, you're showing you're part of the legitimate flow of capital. For more on this, you can read about Hong Kong's investment climate and regulatory landscape on state.gov.

An account freeze is rarely a surprise attack. It's usually the last resort after a series of automated flags have been ignored or poorly explained. Consistent, clear communication is your best defence.

To help you navigate these waters, we’ve put together a practical guide. Check out our Hong Kong banking checklist and how SMEs avoid freezes for actionable steps to keep your account safe.

Ultimately, if you understand what banks are looking for and operate with transparency, you can all but eliminate the risk of an account freeze. It just comes down to treating your banking relationship with the same professional care you give every other part of your business.

When to Partner with a Professional Advisory Firm

Thinking about opening a Hong Kong business account on your own? For a simple, locally-owned company, it's absolutely doable. It’s a bit like assembling flat-pack furniture — with a straightforward design and clear instructions, you can manage it yourself. You follow the steps, hand over the standard documents, and you’re good to go.

But what happens when the business structure isn't so simple? The instruction manual gets thicker, the parts multiply, and the risk of a costly mistake skyrockets. Suddenly, that DIY approach isn’t a smart way to save money; it's a massive business risk. Knowing when to call in a professional isn’t giving up — it’s making a smart strategic move.

Identifying the Triggers for Professional Guidance

So, when does it actually make sense to bring in an expert? There are a few clear red flags that signal professional help isn't just a nice-to-have, but essential for getting your account opened.

Look out for these common triggers:

- Complex Ownership Structures: If your company is owned by a trust, has layers of corporate shareholders in different countries, or uses nominee arrangements, you’ve moved way beyond a simple setup. Banks will put these structures under a microscope, and a poorly presented application is almost certain to be rejected.

- Regulated or High-Risk Industries: Are you in fintech, crypto, or international trade dealing in high-value goods? These sectors immediately flag you as higher risk. A good advisor knows exactly how to position your business activities to satisfy the bank's tough compliance standards right from the start.

- Non-Resident Directors or Shareholders: When your key people live in countries that banks view as higher-risk, the whole process becomes a lot harder. An expert can see the bank’s potential concerns a mile off and prepare the evidence needed to build trust and get you approved.

An expert advisor doesn't just fill out forms. They're your translator and your advocate, turning your complex business reality into a clear, compelling, and bank-ready story that even the most demanding due diligence teams will understand and accept.

This is where an advisory firm like Lion Business Co. becomes your strategic partner. We don't just file your paperwork; we architect your application for success. We speak directly with senior compliance officers, anticipate their questions, and help ensure your entire corporate structure is not just bankable today, but built to last. It turns a frustrating, uncertain process into a predictable and efficient one, making that professional expertise your most valuable asset.

Questions..

Let's cut to the chase. Here are some straight answers to the questions we hear most often from entrepreneurs looking to set up their business banking in Hong Kong.

Can I Open a Hong Kong Business Account as a Non-Resident?

Absolutely. Hong Kong's reputation as a global financial hub was built on serving international business, so being a non-resident isn't a barrier.

That said, you should be prepared for a more thorough due diligence process. The bank will want to see a solid business plan, real proof of your business activities, and crystal-clear identity documents for every director and shareholder. While some of the old-guard banks might still ask for an in-person meeting, many now handle the entire process remotely, especially if you're working with a firm that can vouch for you. The secret to a smooth approval is putting together a professional, transparent application from the start.

What Is the Minimum Deposit Requirement?

This is a classic "it depends" situation, as the requirements swing wildly from one institution to another. The big international banks, for instance, often look for an initial deposit between HK$50,000 and HK$100,000. They may also hit you with monthly fees if your balance drops below a certain threshold.

On the other hand, most of the newer digital banks and fintech platforms have very low, or even zero, initial deposit requirements. This makes them a fantastic option for startups and smaller businesses. Before you commit, always get your hands on the bank's full fee schedule. You need to know exactly what you'll be paying for account maintenance, individual transactions, and currency exchange.

How Long Does the Account Opening Process Take?

The timeline can be anything from a couple of days to a few months. It really comes down to the provider you choose and how complex your business structure is.

- Digital Platforms: These are your speed demons. For a straightforward application from an approved country, you could be looking at an approval in as little as 48-72 hours.

- Traditional Banks: This route is more involved. A perfectly prepared application might take two to four weeks. But if you submit an application that's incomplete or raises questions, you could easily get stuck in a back-and-forth cycle with the bank that drags on for two or three months.

Ultimately, the quality of your application dictates the speed of the process.

Conclusion

This is exactly where having an expert in your corner makes all the difference. At Lion Business Co., we specialise in building bank-ready applications that tick every compliance box from day one. We know what banks are looking for, which means a faster, more predictable journey for you. Learn how our private advisory can secure your banking setup in Hong Kong.