Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

In the simplest terms, the outstanding balance is the total amount of money you owe on an account at this very moment. It’s the live, real-time figure that includes everything—even that coffee you bought just five minutes ago which hasn't shown up on a formal statement yet.

What an Outstanding Balance Really Means for Your Business

Let's ditch the textbook definitions for a moment. Picture your business having a running tab at your favourite local cha chaan teng. The outstanding balance isn't just what you ordered for lunch today; it's the grand total of everything you've ordered over the past month, minus any payments you've already settled. It’s the most up-to-the-second snapshot of your debt.

For any entrepreneur in Hong Kong, getting this right is fundamental to managing your cash flow. It’s all too easy to mix it up with similar-sounding terms like 'current balance' or 'statement balance', a simple mistake that can lead to miscalculated budgets and unexpected fees.

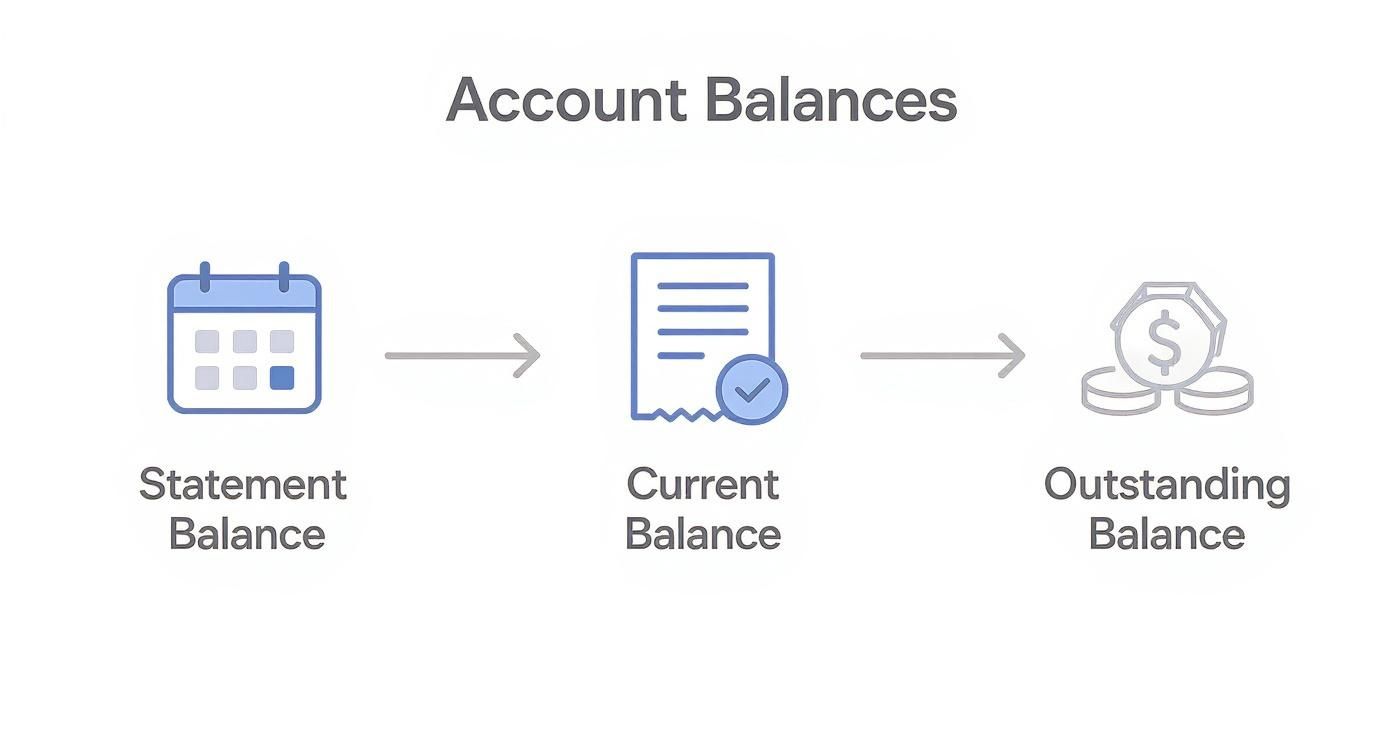

Key Differences in Account Balances

Getting a handle on these different balances isn't just about financial trivia; it directly impacts your planning and decision-making. Each term offers a different view of your financial position. Think of it like this: your statement balance is a photo from last month, the current balance shows what’s been processed since then, and the outstanding balance is the live video feed.

This infographic helps visualise how the balances connect, moving from a static, historical number to a dynamic, real-time total.

As you can see, the flow from the fixed statement balance to the live outstanding balance highlights why the latter is the truest measure of what you owe right now.

The concept of an outstanding balance is a cornerstone of Hong Kong's banking and finance sector. To give you a sense of scale, HSBC reported that its total loans and advances to customers stood at roughly HK$3.61 trillion as of June 2025. That massive number is essentially the combined outstanding balance of all its customers, showing just how vital this metric is to the wider economy.

To better understand how these figures fit into your own company's financial health, it’s worth learning how to analyze a balance sheet, as it lays out all your assets and liabilities in one place. This skill helps you see the complete picture, not just one account in isolation.

For a busy SME owner, the outstanding balance is your most honest financial mirror. It reflects every single transaction—purchases, payments, fees, and interest—the second it occurs, giving you a completely unfiltered view of your obligations.

Knowing the difference isn't just good practice; it prevents nasty surprises and empowers you to make smarter financial decisions. This kind of clarity is the bedrock of any stable and growing business.

Seeing Outstanding Balances in the Real World

The concept of an outstanding balance really comes to life when you take it out of the textbook and apply it to actual business situations. It’s not just a static number on a spreadsheet; for a Hong Kong SME, it’s a living, breathing figure that tells you a story about your cash flow, your debts, and your day-to-day operations.

Let's walk through three common scenarios to see how this plays out on the ground.

The Retail Shop in Mong Kok

Picture a boutique fashion store in the heart of Mong Kok. They use a business credit card to keep their shelves stocked with the latest trends. This week, they place a big order for new inventory from a Korean supplier, charging HK$50,000 to their card. The second that transaction goes through, their outstanding balance jumps by that amount. It doesn't wait for the monthly statement to arrive.

The next day, the owner makes a HK$20,000 payment towards the card. Instantly, the outstanding balance drops to HK$30,000. This number moves in real-time with every purchase and every payment, giving the shop owner an up-to-the-minute view of their short-term debt. Keeping a close eye on this is essential for any business, and our guide to opening a Hong Kong bank account provides more tips on using these financial tools effectively.

The Tech Startup in Tsim Sha Tsui

Now, let's head over to a co-working space in TST, where a tech startup is busy building its platform. They kickstarted their journey with a HK$500,000 SME loan. Six months in, they've been diligently making their HK$10,000 monthly payments, totalling HK$60,000 paid so far.

You might think their outstanding balance is now HK$440,000, but it’s not that simple. Each of those HK$10,000 payments was split between paying down the principal (the original loan amount) and covering the interest. So, the outstanding balance only goes down by the portion of the payment that hit the principal. This is a critical detail for any founder trying to figure out their true path to becoming debt-free.

The Consulting Firm in Central

Finally, imagine a consulting firm based in Central that bills its clients on net-30 terms. For them, the outstanding balance is their accounts receivable—a fancy term for all the money clients currently owe them. Let’s say they have three clients with invoices for HK$80,000, HK$120,000, and HK$50,000. Their total outstanding balance is HK$250,000.

This figure is the lifeblood of the firm. It’s not cash they can spend today, but it’s the future income they’re counting on to pay salaries and rent. A growing outstanding balance can be a sign of healthy sales, but if those invoices aren't paid on time, it quickly turns into a major cash flow headache.

These real-world examples show that an outstanding balance isn't just a number—it’s a direct reflection of your business's financial activity. Whether it's debt you owe or money you're owed, it's the most accurate measure of your current financial position.

Keeping tabs on these balances isn’t just good business practice; it also paints a bigger economic picture. For instance, the total outstanding credit card balances across the city give us a glimpse into wider debt trends. According to Hong Kong Monetary Authority data, the city's total outstanding credit card debt was around HK$149 billion in the second quarter of 2025. You can discover more insights about these financial trends to see how they connect to the broader business environment.

How Your Balances Affect Your Business Credit Score

When we talk about an outstanding balance, it’s not just a number on a statement. Think of it as a direct message to lenders about how your business handles its finances. This figure is a critical component of your business credit score, directly influencing whether you get approved for loans and the interest rates you'll be offered. For any SME, getting this right is non-negotiable.

Your credit utilisation ratio is probably the best health metre for your business's credit. Consistently high balances are a red flag—it’s like trying to run a marathon at a full sprint. It’s unsustainable, and lenders see it as a sign of financial strain, which might lead them to offer less favourable terms or higher rates.

In Hong Kong, credit agencies are looking at a few key things when they assess your balances:

- Credit Utilisation: What percentage of your available credit are you actually using?

- Payment Punctuality: Are you paying on time? Is there a history of defaults?

- Outstanding Balance Trends: Is your debt growing or shrinking over time?

- Account Mix: Do you have a healthy variety of credit types, like loans and trade credit?

All these factors are woven together to create your credit profile, which tells a story of your reliability—or your risk. Credit reference agencies like TransUnion Hong Kong and CRIF are the ones collecting and interpreting this data.

Credit Utilisation As A Health Meter

Of all the metrics, your credit utilisation ratio often carries the most weight. Generally, credit reference agencies in Hong Kong like to see this ratio stay below 30%. Anything higher might start to raise concerns.

Staying under this threshold signals that you're not over-reliant on debt and can manage your finances responsibly. Of course, this number isn't static; it can change daily as you make new purchases or payments.

Imagine a wholesale importer who takes out a significant loan to stock up for a peak season. Their utilisation will temporarily spike, but once they sell the stock and repay the loan, it drops back down. This cycle, when managed well, can actually demonstrate financial strength.

A healthy credit utilisation ratio is like a steady heart rate—it shows consistent financial control and resilience.

Keeping a close eye on this metric helps you avoid unexpected drops in your credit score. It's a good habit to regularly check your credit profile through platforms like TransUnion to stay on top of things.

Practical Tips To Optimise Your Balances

Managing your balances isn't just about paying bills on time; it's about being strategic. Here are a few practical ways to keep things in check:

- Make small, frequent payments. Instead of one large payment at the end of the month, scheduling several smaller ones can help keep your average balance lower.

- Ask for a higher credit limit. If your business is in good standing, requesting a credit limit increase can instantly lower your utilisation ratio without you taking on more debt.

- Automate your payments. This is a simple but effective way to avoid late fees, which needlessly inflate your outstanding balance.

It's also worth considering a diverse mix of credit lines. Having access to trade credit, an overdraft facility, and term loans shows lenders you can confidently manage different types of financial obligations.

Ultimately, consistent and thoughtful management of your outstanding balances paves the way for better financing deals. A lower credit utilisation ratio often opens doors to larger loans and, crucially, lower borrowing costs. By putting these simple practices into place, you can quickly strengthen your credit profile and set your SME up for sustainable growth.

If you’re ready to get a firm grip on your business finances and build a credit history that works for you, get in touch with Lion Business Consultancy Limited. Our private advisory services are designed to guide you through every step of balance management and credit improvement.

Calculate Your Outstanding Balance with Confidence

You don’t need to be a seasoned accountant to get a firm grip on your numbers. Figuring out how your outstanding balance is calculated is one of the most powerful things you can do for your business's financial health, turning what looks like complex maths into clear, actionable insights.

Let’s break down the process for two of the most common financial tools you’re likely using.

For many entrepreneurs, the day-to-day calculations can feel like a distraction from the real work. If you find yourself buried in spreadsheets instead of focusing on strategy, bringing in professional accounting services in Hong Kong can provide a ton of clarity and free you up to do what you do best.

The Simple Formula for Revolving Credit

When it comes to revolving credit, like your business credit card, the calculation is refreshingly straightforward. The balance is constantly in motion, a direct reflection of your daily business activities.

Think of it like a running tab:

The formula for a credit card's outstanding balance is basically: Previous Balance + New Purchases + Fees – Payments = New Outstanding Balance.

Every time you buy new inventory, pay for a software subscription, or make a repayment, this number shifts. It’s a live tally of your short-term debt, giving you the most up-to-the-minute picture of what you owe.

How Loan Balances Decrease Over Time

Calculating the outstanding balance for something like a term loan for new equipment—what’s known as an amortising loan—works a bit differently. With each fixed monthly payment you make, you’re tackling two things at once: the principal (the original loan amount) and the interest that has built up.

- Principal Portion: This is the part of your payment that actually reduces the amount you borrowed.

- Interest Portion: This is the lender's fee for letting you borrow the money.

At the beginning of the loan, a larger chunk of your payment gets eaten up by interest. But as you keep making those payments, the tables turn, and more of your money starts going towards clearing the principal. This is why your outstanding balance seems to shrink faster and faster over the life of the loan.

Here’s a simplified look at how this plays out over the first three months of a business loan.

Sample Outstanding Balance Calculation for a Business Loan

| Month | Starting Balance | Monthly Payment | Interest Paid | Principal Paid | Ending Outstanding Balance |

|---|---|---|---|---|---|

| 1 | HK$100,000.00 | HK$3,000.00 | HK$416.67 | HK$2,583.33 | HK$97,416.67 |

| 2 | HK$97,416.67 | HK$3,000.00 | HK$405.90 | HK$2,594.10 | HK$94,822.57 |

| 3 | HK$94,822.57 | HK$3,000.00 | HK$395.09 | HK$2,604.91 | HK$92,217.66 |

As you can see, even though the payment stays the same, the amount of principal paid increases each month.

Understanding this split is crucial. It shows you exactly how much progress you’re making on paying down the actual debt, not just servicing the interest. Armed with this knowledge, you can track your long-term liabilities with real confidence and plan your company's financial future with much greater precision.

Smart Ways to Manage and Reduce Your Balances

Understanding what an outstanding balance is is one thing; getting it under control is where the real work begins. For any busy entrepreneur in Hong Kong, mastering your liabilities is more than just paying bills on time. It's about smart financial management that fuels your company's growth. Let's dig into a few proven methods to start chipping away at those numbers.

Choosing Your Repayment Strategy

Juggling multiple debts—say, a credit card, a supplier credit line, and a small business loan—can feel overwhelming. Where do you even start? Thankfully, two popular strategies can give you a clear plan of attack.

-

The Debt Avalanche Method: This is the purely logical approach. You focus on paying off the debt with the highest interest rate first, while making only the minimum payments on everything else. From a numbers perspective, this method saves you the most money on interest in the long run.

- Who it's for: Perfect for business owners who are disciplined and motivated by the financial efficiency of saving money over time.

- How to implement: List all your debts from the highest interest rate to the lowest. Throw every spare dollar at the debt at the top of the list. Once it's paid off, you "roll" that entire payment amount over to the next one on the list.

-

The Debt Snowball Method: This strategy is all about psychology and momentum. You start by paying off your smallest balance first, no matter what the interest rate is. The idea is to get some quick wins under your belt, which builds the motivation to keep going.

- Who it's for: Great for entrepreneurs who need to see tangible progress to stay on track. Those small victories can make a huge difference.

- How to implement: Line up your debts from the smallest balance to the largest. Attack the smallest one with everything you've got until it's gone, then take its payment and add it to your attack on the next smallest debt.

Automating Payments and Negotiating Terms

Beyond just deciding which debt to tackle first, a few other proactive steps can prevent your balances from getting out of hand.

Set Up Automated Payments

Late fees are the absolute worst—they're completely avoidable costs that do nothing but bloat your outstanding balance. Setting up automatic payments for at least the minimum amount due is a simple safety net. It guarantees you’ll never miss a due date, which helps protect both your credit score and your cash reserves.

Negotiate Better Supplier Terms

A huge chunk of your outstanding liabilities comes from your accounts payable—the money you owe to your suppliers. Don't just accept the standard terms. If you've built a solid payment history with a vendor, have a conversation. Asking for extended payment terms, like moving from Net 30 to Net 45, can give you crucial breathing room and align your expenses more closely with your income cycle. For a deeper dive, consider implementing best practices for accounts payable, which is all about managing what you owe suppliers more effectively.

A well-managed balance sheet isn't about being debt-free; it's about making debt work for you. By strategically reducing high-cost liabilities and aligning payments with your income cycle, you turn debt from a burden into a tool for growth.

At the end of the day, these strategies are all about putting your business in a stronger financial position. A huge part of that is maintaining healthy income, which is why we’ve put together 4 proven strategies for positive cash flow to complement your debt reduction efforts. When you combine smart repayment tactics with strong cash flow, you're on the fast track to financial stability.

Your Business and the Broader HK Economy

It’s easy to get lost in the day-to-day numbers of your own business, but your company’s finances don't exist in a vacuum. They're a small but important piece of a much larger economic picture. When we talk about outstanding balance, the concept scales up from your SME loans and credit cards to become a key indicator of Hong Kong's overall economic health.

Think about it this way: just as your business might take on debt to fund growth, so does the government. These larger financial tools, like government bonds, work on the exact same principle. They represent a total amount owed and give us a big-picture view of the market's confidence and the government's financial strategy. For example, the Hong Kong government often issues bonds to raise money for huge infrastructure and sustainability projects that benefit everyone.

Think of the city's total outstanding government debt like a business taking out a massive loan for a new factory. It's a strategic liability, a calculated risk taken to spark long-term growth and stability for the whole community.

As of October 2025, the Hong Kong Monetary Authority (HKMA) reported significant outstanding amounts under its various Bond Programmes. These figures aren't just abstract numbers; they represent the government's total debt that's still waiting to be paid back, showing how public finances are managed on a massive scale. If you're curious, you can explore the monthly data from the HKMA yourself to see the trends.

Keeping an eye on these broader economic currents helps you understand how major market shifts can eventually affect your own operations. It’s a good reminder that your own careful financial management doesn’t just help your company—it contributes to the stability of the entire ecosystem we all operate in.