Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

Yes, you absolutely can open an offshore account online. In today’s interconnected world, the process has shifted from stuffy, in-person meetings to streamlined digital experiences. It typically involves pinpointing the right country for your business goals, gathering your documents, and applying through a bank’s secure portal or with the help of a specialist firm. Thanks to digital uploads and video verification calls, you can now establish your global financial footprint from your own office.

The Reality of Global Banking for Your Business

Before we dive into the “how,” let’s set the stage. For a modern entrepreneur, offshore banking isn’t some clandestine plot from a spy movie, reserved for the ultra-wealthy. It’s a pragmatic, often essential, strategy for any business with ambitions that stretch beyond its home borders.

Forget the old clichés. Think of it less as hiding money and more as building a financial command center for your international operations. It’s about creating a stable and efficient foundation from which your business can scale globally.

Why Modern Businesses Go Offshore

The motivations are almost always born from tangible business needs. Imagine a Hong Kong-based e-commerce company that’s found a growing customer base in Europe. Opening an offshore account in a business-friendly European jurisdiction makes receiving payments in Euros seamless. This single move can slash currency conversion fees and shield profit margins from volatile exchange rates.

For many businesses, especially those in sectors facing banking challenges for high-risk industries, these accounts aren’t just a perk; they’re a lifeline. They offer a legitimate and stable channel to conduct international trade without constant friction.

At its core, the appeal boils down to a few key advantages:

- Asset Protection: Placing capital in a jurisdiction with a robust rule of law can insulate your business from economic or political instability at home.

- Operational Efficiency: It simply makes everything smoother. You can manage multiple currencies, streamline cross-border payments, and access global financial markets with far less bureaucracy.

- Strategic Growth: An offshore account is often a crucial first step when entering a new international market. It instantly lends credibility with local partners, suppliers, and customers.

A Look at Hong Kong’s Role

Hong Kong’s private banking sector remains a global powerhouse. In fact, some analysts predict its offshore wealth could surpass Switzerland’s by 2025. A huge part of this appeal is its territorial tax system, meaning income generated outside Hong Kong is generally not taxed locally.

But there’s a catch. While it’s fairly simple for residents to open accounts, non-residents face a much higher bar. You’ll often need to register a local company or be prepared to make a very substantial initial deposit.

This guide is designed to walk you through the entire journey, from strategy to execution. You’ll see that while it requires diligence and organization, the ability to open an offshore account online is more accessible today than ever before.

How to Choose the Right Jurisdiction

Choosing the right jurisdiction is the most critical decision you’ll make when you decide to open an offshore account online. This isn’t just about picking a bank; it’s about selecting an entire country’s financial ecosystem, legal framework, and political climate to support your business. The outdated notion of simply finding a “tax haven” is gone—this is a strategic business decision.

The secret is finding the perfect fit. An e-commerce business selling into Asia might thrive with an account in Singapore, leveraging its world-class tech infrastructure and strong intellectual property laws. In contrast, a family office focused on wealth preservation might look to Switzerland for its legendary stability and private banking heritage. Your business model should always lead the way.

Your Business Goals Come First

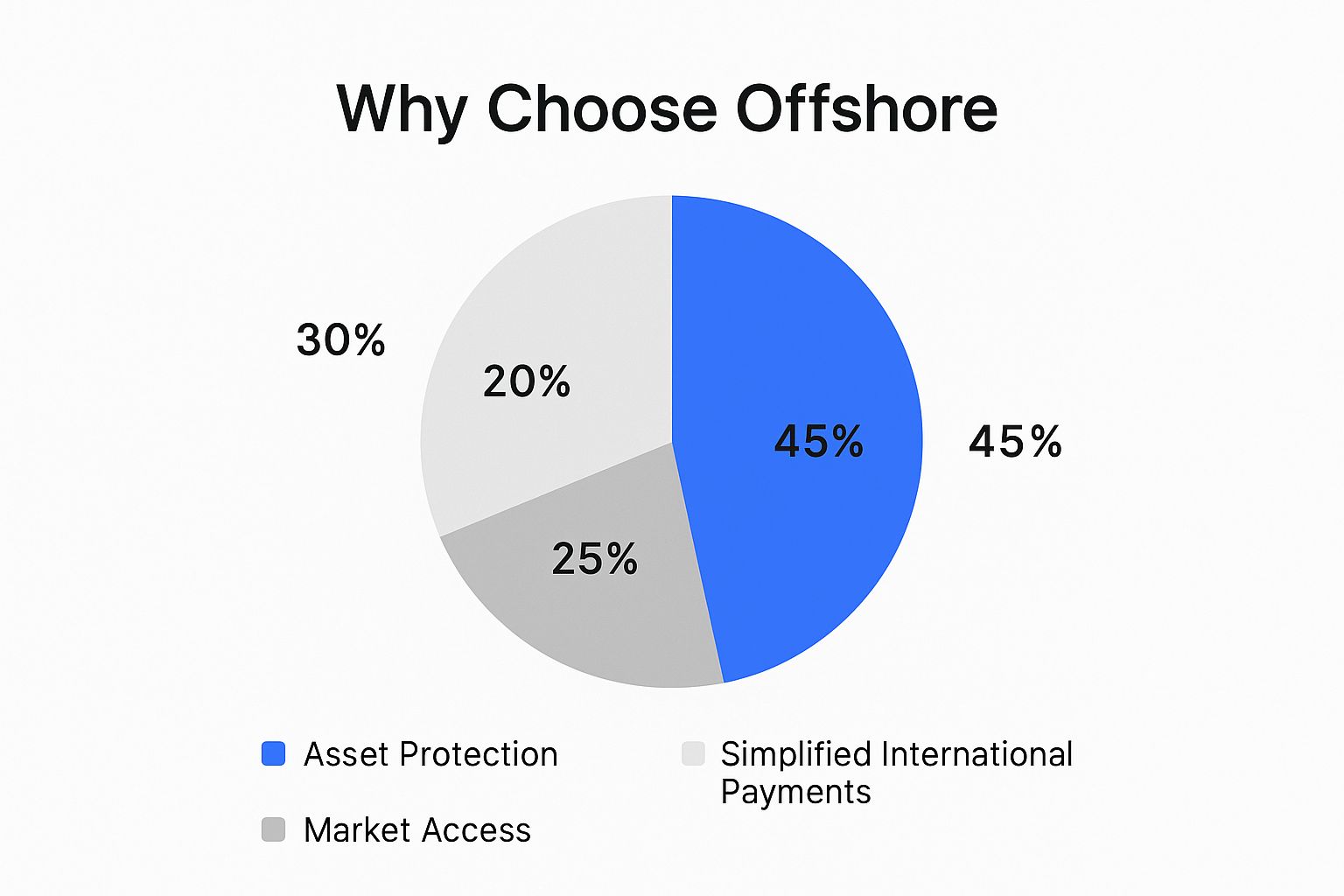

Before you even start comparing countries, take a hard look at your business plan. The right jurisdiction is a natural extension of that plan. What are you truly trying to accomplish? Is it primarily about asset protection, simplifying international payments, or gaining a foothold in new markets?

This infographic breaks down the primary drivers for entrepreneurs going offshore.

As you can see, asset protection remains the top priority for 45% of businesses. This really underscores how vital political and economic stability are when making your choice.

Comparing Top Offshore Banking Jurisdictions

Every financial hub has its own unique character. Hong Kong, for instance, is a phenomenal gateway to mainland China and the rest of Asia. Its banking sector is incredibly robust—total deposits in authorized institutions jumped by 6.7% year-on-year, proving its lasting appeal. The challenge? Major banks like HSBC and Standard Chartered can make it difficult for non-residents to open accounts entirely online.

This is why you need to dig deeper and compare your options carefully. The table below offers a quick snapshot of some popular choices to get you started.

| Jurisdiction | Key Advantage | Typical Minimum Deposit | Online Accessibility | Best For |

|---|---|---|---|---|

| Singapore | High-tech banking & strong global reputation | US$20,000 – US$50,000 | Good to Excellent | Tech startups, e-commerce, and businesses trading in Asia. |

| Switzerland | Unmatched stability & private banking prestige | US$500,000+ | Moderate | High-net-worth individuals and wealth preservation. |

| Belize | Low deposit requirements & accessibility | US$1,000 – US$5,000 | Excellent | Startups, digital nomads, and small online businesses. |

| Hong Kong | Gateway to China & major trade finance hub | US$10,000 – US$25,000 | Limited for non-residents | Businesses with significant trade in/out of China. |

| Mauritius | Strong ties to Africa & India, favourable tax treaties | US$5,000 – US$10,000 | Good | Investment funds and companies operating in Africa/Asia. |

This comparison makes it clear that there’s no single “best” option—only the best option for you. A nimble startup has vastly different needs than a multi-generational family office.

No matter where you’re leaning, there are a few non-negotiable factors to consider:

- Political and Economic Stability: Look for a long track record of stable governance and the rule of law. This is the bedrock of long-term security.

- Reputation and Compliance: Ensure the jurisdiction is on international “white lists.” A well-respected financial center means fewer headaches when dealing with partners in the US or Europe.

- Banking Specialisation: Does the country’s banking scene cater to your industry? Some are experts in trade finance, others in private wealth, and a growing number in fintech.

Choosing a jurisdiction is like picking a long-term business partner. You need to ensure their strengths complement your needs and that you can trust them to be reliable for years to come. A mismatch here can create immense friction down the line.

Ultimately, this decision requires homework to align a country’s environment with your vision. Our detailed guide on the best countries to open an offshore bank account provides a much deeper dive into the top contenders. Getting this choice right lays the foundation for your international success.

Getting Your Paperwork in Order for a Flawless Application

Trying to open an offshore account online with disorganized paperwork is like showing up to a marathon in flip-flops. It’s a complete non-starter. Banks aren’t just being difficult; they are legally bound to follow strict global regulations, making their due diligence process absolutely non-negotiable.

Thorough preparation is more than half the battle. Before you even think about an application form, your first job is to gather and correctly prepare all your documents. This isn’t just about having the right files—it’s about presenting them in the exact format the bank requires. One blurry scan or an uncertified copy can lead to weeks of frustrating delays or, worse, an outright rejection.

The Core Document Checklist

Let’s imagine a freelance consultant based in Hong Kong who wants to open a business account in Belize to manage payments from her international clients. Her first move should be to methodically organize her essential documents. While every bank has its quirks, they will all ask for this core set of paperwork.

You’ll almost certainly need the following:

- Certified Proof of Identity: This is usually a high-quality, color copy of your passport. The key here is certified. A notary public, lawyer, or accountant must officially stamp and sign the copy to verify it’s a true likeness of the original.

- Proof of Residential Address: A recent utility bill or bank statement is the standard. It must clearly show your full name and current address and typically needs to be less than three months old. If it’s not in English, you’ll need a certified translation.

- Professional Reference Letter: It’s quite common for banks to request a letter from your current bank or a professional like a lawyer or accountant. This person should have known you for some time and be able to vouch for your good standing.

For a business account, the paperwork requirements become much more detailed. The bank needs a complete picture of your company to satisfy its Anti-Money Laundering (AML) obligations.

Making a Strong Case for Your Business

Treat your application like a business proposal. You’re not just requesting an account; you’re demonstrating that you’re a credible, low-risk client. Vague, one-word descriptions of your business are a massive red flag for any compliance officer.

A common mistake I see is a poorly defined business activity. Simply writing “consulting” on the form won’t cut it. You need to explain precisely what services you offer, who your typical clients are, your expected monthly transaction volumes, and the geographical source of your income.

Your business documents must tell a clear and compelling story:

- Corporate Documents: This includes your Certificate of Incorporation, Memorandum and Articles of Association, and a current Register of Directors and Shareholders.

- Proof of Source of Funds/Wealth: This is critically important. You must be prepared to show where the money for your initial deposit and future transactions is coming from. This can be supported by documents like client contracts, sales invoices, or personal investment statements.

For anyone looking to do business in Hong Kong, understanding the specific local rules is crucial. Our dedicated guide on Hong Kong bank account requirements for non-residents offers a much deeper look. Nailing this documentation from the start transforms your application from a hopeful wish into a professional submission—and that makes all the difference.

Navigating the Online Application and Compliance Maze

Alright, this is where your careful preparation pays off. You’ve organized your documents, selected the right jurisdiction, and are now facing the bank’s digital application form.

Hitting ‘submit’ might feel like launching your business plan into the void, but it’s actually the start of a structured, human-led review. Your application doesn’t go to a faceless algorithm; it lands on the desk of a real person—a compliance officer. Their job isn’t to find reasons to say no. It’s to verify that you and your business are a solid, low-risk match for their institution.

Think of it as pitching a potential business partner. They need to be convinced that your story adds up, meticulously checking every detail against the bank’s risk policies and international regulations.

The Verification Call: What to Expect

A crucial step when you open an offshore account online is often a video verification call. This is your opportunity to put a face to the name and clarify any ambiguities in your application. The compliance officer will need to see you, match your face to your passport, and ask some straightforward questions about your business.

They’ll likely ask things like:

- “Can you walk me through your business model in your own words?”

- “Who are your main clients, and where are they located?”

- “What will be the primary use of this account, and what is your estimated transaction volume?”

- “Could you explain the origin of your initial funding?”

Be prepared. Your answers need to be confident, consistent, and directly align with the story your documents tell. This isn’t an interrogation; it’s a conversation designed to build trust. For a deeper dive, our guide on common questions and answers about offshore bank account opening can help you prepare.

Seeing Things from the Bank’s Perspective

It’s easy to get frustrated by the process, but it helps to understand the immense pressure these banks are under. Financial institutions, especially in top-tier jurisdictions, are on the front lines of preventing money laundering and terrorist financing. The amount of capital flowing across borders is staggering.

Take Hong Kong, for example. Its banking sector is responsible for 53.3% of the city’s enormous external financial claims, totaling a mind-boggling HK$14,948.8 billion—that’s 4.7 times its GDP. These numbers highlight just how central these banks are to the global economy and why their compliance checks must be airtight.

When you understand the bank’s perspective, the compliance process becomes much less intimidating. Demonstrating that you’re aware of financial security protocols, like the details of Anti-Money Laundering (AML) transaction monitoring, positions you as a serious, well-prepared applicant.

From the moment you click submit to the final approval, the entire process can take anywhere from a few days to several weeks. Patience is key. By presenting a professional, transparent, and thoroughly documented application, you can turn what seems like a hurdle into a straightforward step toward getting your offshore account up and running.

Managing Your Offshore Account Responsibly

Congratulations, you got the approval! But don’t break out the champagne just yet. Opening the account is a significant milestone, but transforming it into a stable, long-term asset for your business is where the real work begins.

Think of your new banking relationship less like a simple account and more like a partnership. And like any good partnership, it thrives on clear communication and mutual respect.

The number one rule? Communicate, communicate, communicate. Banks dislike surprises. If you’re about to pivot your business model, expand into a new country that might be considered high-risk, or you’re expecting an unusually large wire transfer, give your relationship manager a heads-up. A simple, proactive email can be the difference between a smooth transaction and a compliance-triggered account freeze that ties up your funds for weeks.

Day-to-Day Best Practices

Beyond the big-picture communication, smart account management boils down to good habits. Keeping your account in good standing isn’t just about avoiding red flags; it’s about actively demonstrating that you’re a low-risk, transparent, and valuable client.

Here are a few practical tips to integrate into your routine:

- Mind the Minimums: Most offshore accounts have a minimum balance requirement. Dipping below it can trigger surprisingly high monthly fees or, in some cases, prompt the bank to close your account. I always advise setting a recurring calendar reminder to check your balance.

- Know Your Fees: International transfers, currency conversions, and even basic account maintenance have associated costs. Spend an hour reading the fee schedule. It’s not thrilling, but it will save you from those “where did that money go?” moments down the road.

- Leverage Multi-Currency Features: If you bill clients in different countries, this is a game-changer. Holding funds in USD, EUR, GBP, or other major currencies directly shields your capital from the whims of exchange rate fluctuations. It’s a core benefit, so make sure you’re using it.

Staying Compliant in a Transparent World

Let’s be clear: the era of hiding money in a secret Swiss account is long over. Global standards like the Common Reporting Standard (CRS) have created a system of automatic information exchange between the tax authorities of over 100 countries.

Your offshore bank is legally required to report your account details to its local government. That government then shares the information with the tax agency in your home country.

This isn’t a reason to panic; it’s a reason to be organized. Full, honest disclosure with your home tax authorities is non-negotiable. The goal of modern offshore banking is legitimate asset protection and business efficiency—not tax evasion.

This new era of transparency makes meticulous record-keeping essential. Retain every invoice, contract, and transaction statement related to the account. Not only does this simplify your own bookkeeping, but it also ensures you’re always prepared if your tax authority has questions.

When you manage your account responsibly, it becomes exactly what it was designed to be: a powerful and secure tool for taking your business global.

Answering Your Top Questions About Offshore Accounts

Even with a clear plan, stepping into the world of global banking can feel a bit daunting. I understand. Over the years, I’ve seen the same key questions come up time and again. Let’s tackle them head-on so you can move forward with confidence.

Is It Actually Legal to Open an Offshore Bank Account?

Absolutely, yes. For any legitimate business purpose—such as managing international revenue, safeguarding corporate assets, or structuring your tax affairs more efficiently—opening an offshore account is a perfectly standard and lawful financial strategy. The entire modern system is built on transparency and compliance.

The critical element is playing by the rules of both your home country and the offshore jurisdiction. This means you must declare the account and any income it generates to your local tax authorities, just as you would with a domestic account. Illegality only enters the picture when accounts are intentionally used to conceal money and evade taxes, which is a serious crime. This guide is strictly focused on the smart, compliant use of offshore banking to help your business grow.

What’s the Real Cost? How Much Money Do I Need to Start?

This is probably the most common question I hear, and the honest answer is: it truly depends. The financial requirements vary widely, and the right fit hinges on your specific goals.

- The Private Banking Elite: Think of the classic Swiss private banks. These institutions are designed for serious wealth preservation and often require an initial deposit of $500,000 or more. They cater to a specific, high-net-worth clientele.

- Established International Banks: For most SMEs, this is the sweet spot. Reputable banks in solid jurisdictions like Singapore, Mauritius, or Hong Kong have much more accessible entry points. You’re typically looking at minimum deposits in the $5,000 to $25,000 range.

- The New Guard (Digital Banks & EMIs): Financial technology has been a game-changer. A new wave of digital-first players offers business accounts with incredibly low—or even zero—minimum deposit requirements. The trade-off might be slightly higher monthly fees, but the barrier to entry has effectively been removed.

My advice? Be realistic about your company’s capital from day one. It will save you a lot of time and help focus your search.

The old myth that offshore banking is exclusively for the super-rich is just that—a myth. While premium, white-glove services still demand significant capital, the digital shift has opened up a world of global banking for startups and SMEs.

Can I Really Open an Offshore Account Online Without Getting on a Plane?

Yes, you can, and it’s rapidly becoming the standard. The days of needing to fly halfway around the world for a formal, in-person meeting are largely behind us, at least for the majority of business accounts. Most modern international banks and specialized service providers have refined their remote onboarding processes into a science.

It usually looks something like this:

- You upload all your certified documents through a secure online portal.

- You participate in a video call with a bank representative who verifies your identity against your passport.

A handful of old-school private banks might still request a face-to-face meeting for their ultra-high-net-worth clients, but the industry trend is crystal clear: digital onboarding is the future. This has made it easier than ever to open an offshore account online right from your desk.

How Does the Common Reporting Standard (CRS) Affect Me?

The Common Reporting Standard (CRS) is a big deal. It’s essentially a global agreement for the automatic exchange of financial account information between tax authorities. With over 100 countries participating, it has created a new standard of worldwide financial transparency.

Here’s what it means for you: when you open an offshore account, your new bank will identify your country of tax residence. It is then legally obligated to report details about your account (like the balance and gross income) to the local tax authority in its jurisdiction. That authority then automatically forwards the information to the tax agency in your home country.

Put simply, the concept of “banking secrecy” from tax authorities is a relic of the past. CRS makes it non-negotiable to be fully transparent and compliant with your tax reporting at home. It reinforces why you should only use offshore accounts for legitimate, strategic purposes, not to hide assets.

Conclusion

At Lion Business Consultancy Limited, we navigate these complexities every day. We don’t just help you get an account opened; we help you build a secure, compliant financial foundation that supports your global vision. If you’re seeking personalized, one-on-one guidance to ensure your international expansion is done right, let’s have a conversation.