Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

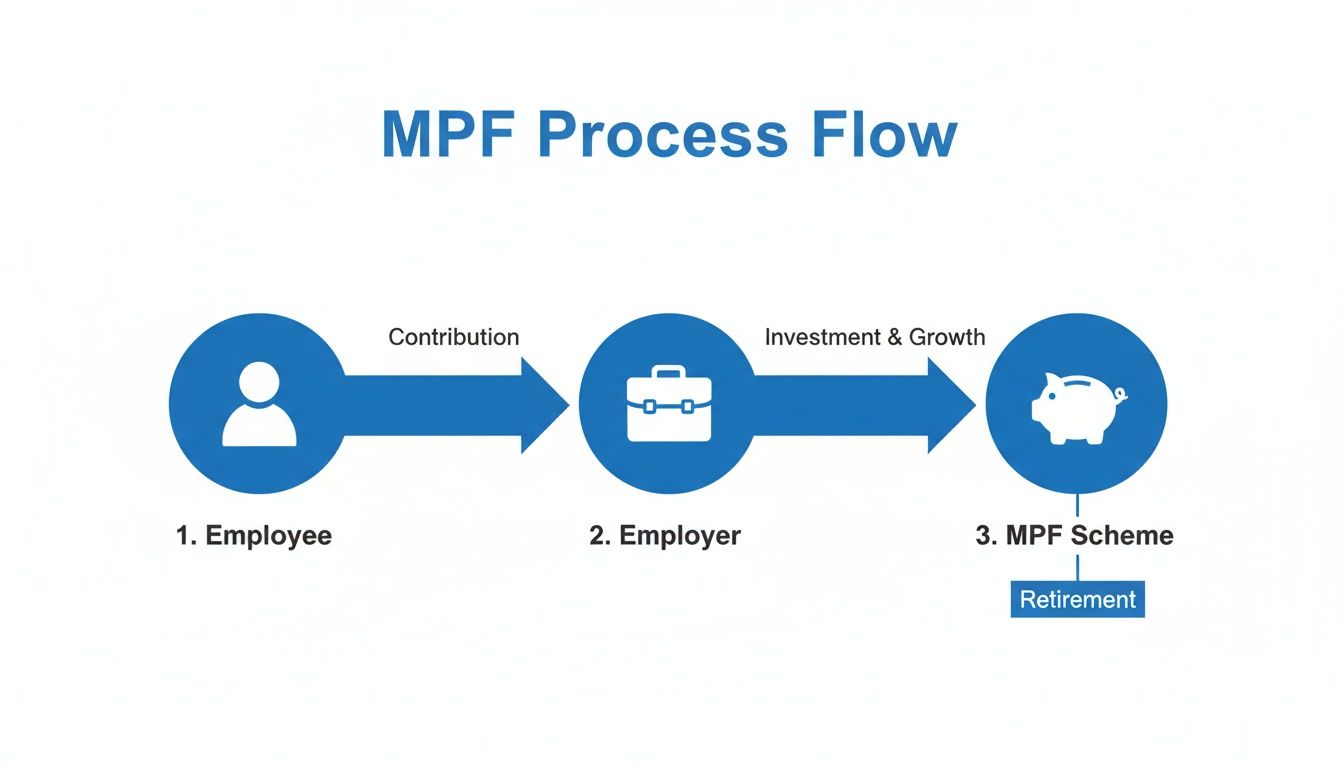

If you're running a business in Hong Kong, the Mandatory Provident Fund (MPF) is one of the first things you need to master. Think of an MPF HK contribution as a compulsory monthly deposit into a retirement savings account for your employees—a fund that both you and your team pay into. It’s a foundational legal duty, woven into the fabric of employment in this city.

What is an MPF Contribution?

At its heart, the MPF is a shared retirement savings plan. It's a financial partnership between you, the employer, and your team member. Every month, you make a mandatory payment into your employee’s personal retirement fund, and they chip in a portion of their salary, too. This isn't just another line item on a payslip; it's the bedrock of Hong Kong's retirement security system.

For a small or medium-sized business, getting this right from day one is non-negotiable. It keeps you compliant and ensures your payroll runs like a well-oiled machine. With every salary payment, a calculated slice of your employee’s income, plus a matching contribution from your company, goes directly into their chosen MPF scheme. This slowly but surely builds a financial nest egg they can draw on when they retire.

Why MPF is a Core Employer Responsibility

Your role in the MPF system isn't optional—it's central to being a lawful and responsible employer in Hong Kong. The government created the system to help an ageing workforce build a basic level of financial security for their post-working years.

Since its launch back in December 2000, the MPF has grown into a major pillar of retirement savings. To put its size into perspective, total MPF assets are expected to hit around HK$1,530 billion by the end of September 2025. That incredible growth is powered by the consistent, mandatory contributions from employers and employees just like you and your team.

Here’s a quick snapshot of the essential MPF obligations every Hong Kong employer must manage.

Core Employer MPF Responsibilities at a Glance

| Responsibility | What It Means for Your Business |

|---|---|

| Enrol New Employees | You must sign up all eligible staff for an MPF scheme within the first 60 days of employment. |

| Calculate Contributions | You are responsible for accurately calculating both your and your employee's contribution amounts. |

| Make Employer Payments | You need to pay your share of the contribution for every single employee on your payroll. |

| Remit Payments on Time | The total amount (both your and your employee's share) must be sent to the MPF trustee monthly. |

Getting these steps right is crucial. Stumbling here can lead to serious penalties from the authorities, but handling them correctly shows you’re committed to your team’s long-term financial well-being.

For a wider view on how retirement savings work, it’s also helpful to look at general principles for understanding workplace pension schemes in a global context.

How to Calculate MPF Contributions Accurately

Alright, let's move from theory to the reality of your monthly payroll run. Getting the MPF amount right for your team doesn't have to be a headache. It all boils down to one key concept: relevant income.

Once you nail down what this includes, calculating the correct mpf hk contribution becomes a simple, repeatable task.

So, what is it? Think of relevant income as the total cash compensation an employee receives before any deductions are made. This covers their basic salary, of course, but also things like commissions, bonuses, leave pay, and any cash allowances. Get this figure right, and the rest of the calculation is surprisingly straightforward.

The whole idea is a shared responsibility, where both you and your employee build their retirement savings together.

As the employer, you collect both portions and pass them along to the MPF trustee, who manages the funds for the long term.

Understanding the 5% Rule and Income Thresholds

At its heart, the system is simple. The standard contribution is 5% from the employer and 5% from the employee, based on their monthly relevant income.

But there's a small catch: this 5% rule only applies within specific income brackets set by the Mandatory Provident Fund Schemes Authority (MPFA). Knowing these thresholds is crucial.

- Minimum Income Level: If an employee’s monthly relevant income is less than HK$7,100, they don't have to contribute a cent. You, as the employer, however, still need to contribute your 5% share.

- Standard Income Level: For anyone earning between HK$7,100 and HK$30,000 a month, the standard 5% + 5% rule applies perfectly.

- Maximum Income Level: For high earners making over HK$30,000 a month, contributions are capped. The mandatory contribution is fixed at HK$1,500 from both you and the employee.

A common trip-up for new business owners is thinking no contribution is needed for low-income staff. That’s a mistake. The employer’s 5% obligation is always there, no matter what the employee earns. Your responsibility never drops to zero.

Real-World Calculation Examples

Abstract rules are one thing, but seeing the numbers in action makes it all click. Let's walk through a few scenarios you'll almost certainly encounter.

Example 1: A Full-Time Sales Director

Meet Alex. He’s a sales director with a fixed monthly salary of HK$45,000.

- Relevant Income: HK$45,000

- Analysis: Alex's income is well above the maximum level of HK$30,000.

- Employer Contribution: Capped at HK$1,500.

- Employee Contribution: Capped at HK$1,500.

- Total Monthly MPF Payment: HK$3,000

Even though 5% of his salary is HK$2,250, the cap kicks in. For a closer look at how this works for top earners, check out our guide on the MPF maximum contribution rules.

Example 2: A Part-Time Contract Designer

Now, let's look at Ben, a contract designer who works flexible hours. Last month, his work brought in HK$12,000.

- Relevant Income: HK$12,000

- Analysis: Ben's income falls squarely in the standard range (HK$7,100 to HK$30,000).

- Employer Contribution: 5% of HK$12,000 = HK$600.

- Employee Contribution: 5% of HK$12,000 = HK$600.

- Total Monthly MPF Payment: HK$1,200

Example 3: An Intern Earning a Small Stipend

Finally, consider Chloe, an intern who earned HK$6,500 last month.

- Relevant Income: HK$6,500

- Analysis: Chloe's income is below the minimum threshold of HK$7,100.

- Employer Contribution: 5% of HK$6,500 = HK$325.

- Employee Contribution: HK$0 (she is exempt).

- Total Monthly MPF Payment: HK$325

As you can see, the calculation just adapts to different pay scales. First, identify the relevant income, then check it against the thresholds. Do that, and you can confidently work out the correct mpf hk contribution for every person on your team.

Fulfilling Your Employer MPF Obligations

Getting the MPF numbers right is just one part of the puzzle. The other, equally crucial part, is managing your responsibilities throughout an employee's time with your company. Think of it as a compliance roadmap—following it not only keeps you in good standing with the Mandatory Provident Fund Schemes Authority (MPFA), but it also shows your team you're taking their retirement savings seriously.

Your duties kick in the moment a new hire walks through the door and continue right up until their last day. The process itself isn't complicated, but it demands attention to detail.

From Onboarding to Offboarding: The MPF Lifecycle

Managing your mpf hk contribution isn't a once-a-month chore. It’s a continuous cycle that follows an employee's entire journey with your business. Each stage has its own clear rules that every SME owner needs to get right.

Let's walk through the three key phases you'll need to handle:

- Employee Enrolment: You must enrol any new, eligible employee into your chosen MPF scheme within their first 60 days of employment. This is a firm deadline. It doesn't matter if they're on probation—the clock starts ticking on day one.

- Monthly Contributions: Once they're enrolled, it's your job to send both your and your employee's contributions to the MPF trustee every single month. The absolute cut-off date is the 10th day of the following month.

- Final Payment on Termination: When an employee leaves, you need to make their final MPF payment and inform the trustee of their departure. This final payment is also due by the 10th of the month after their last day of work.

That 60-day enrolment window often trips people up. It's a grace period to sort out the paperwork, but your contribution liability starts from the employee's first day. All those back-contributions are due once the enrolment is complete.

The Consequences of Getting It Wrong

The MPFA doesn't mess around with these deadlines. Missing them can hit your business with immediate financial penalties. It's not just a light slap on the wrist; the penalties are there to make the employee whole for the delay and to ensure it doesn't happen again.

If you fail to make an mpf hk contribution by the 10th of the month, the MPFA will slap you with a payment notice for the overdue amount plus a 5% surcharge. This isn't a fine that goes to the government; that surcharge is paid directly into your employee’s MPF account to compensate them for the lost investment growth.

Repeated non-compliance can lead to even bigger penalties and, in serious cases, legal action. The best way to avoid these headaches is to have a solid payroll process that flags these dates automatically. Staying on top of it protects your business and secures your team's financial future.

This commitment to regular contributions is especially meaningful when you see how it impacts an employee's retirement savings over time. For instance, despite market ups and downs, MPF funds have shown solid medium-term growth. As of September 30, 2025, the 376 registered MPF funds in Hong Kong reported impressive average returns, with a year-to-date average of +16.6% and a three-year average of +42.2%. For business owners, these figures show just how much consistent contributions matter, which can be a powerful tool for retaining talent. You can find more detail on these performance trends in Refinitiv Lipper's analysis.

Handling MPF for Different Types of Workers

The modern workforce is rarely a simple nine-to-five affair. As a business owner in Hong Kong, you're likely working with freelancers, part-time specialists, and maybe even international talent. This flexibility is a huge asset, but it can make navigating your mpf hk contribution obligations feel a bit tricky.

Getting this right isn't just a box-ticking exercise. It's about treating everyone who contributes to your business fairly and legally. Let's break down the different work arrangements and what they mean for your MPF duties.

MPF Rules for Self-Employed Individuals

So, you've just hired a freelance designer for a big project. Are you responsible for their MPF? In short, no.

In Hong Kong, self-employed persons (SEPs)—from independent consultants to gig-economy workers—are in the driver's seat for their own retirement savings. They're required to enrol themselves in an MPF scheme within 60 days of starting their business.

- Their Responsibility: The freelancer is solely responsible for calculating and making their own MPF contributions based on their income.

- Your Role: As the company hiring them, you have no employer obligation to contribute. Your job is simply to pay their invoices on time.

This is a clean-cut distinction. You get the benefit of their expertise without taking on the administrative burden of their MPF, which sits squarely with them.

Managing Contributions for Part-Time and Casual Staff

This is where your responsibilities as an employer kick back in, and the details matter. Many businesses, particularly in retail, F&B, and construction, depend on part-time and casual workers.

Part-Time Employees: If you have a part-timer who works for you for 60 continuous days or more, you must enrol them in your MPF scheme. It doesn't matter how many hours they work per week; once they cross that 60-day threshold, the rules are the same as for your full-time staff. Contributions are calculated based on their monthly relevant income.

Casual Employees: The rules are even tighter for "casual employees," which typically means staff hired on a day-to-day basis or for less than 60 days. This is common in the construction and catering industries. For these workers, you have to start making an mpf hk contribution from their very first day on the job.

To make this easier, the MPFA has set up Industry Schemes. These are a practical solution that allows casual workers to have one MPF account that they can carry with them as they move between different employers in the same sector.

Key Takeaway: The 60-day rule is a hard line. If a part-time worker’s contract is renewed or they simply keep working past that mark, their MPF eligibility is triggered. Ignoring this can lead to hefty penalties and the headache of sorting out back-payments.

A diverse workforce brings a mix of MPF obligations. The table below provides a quick side-by-side look at the rules for different types of workers in Hong Kong.

MPF Rules for Different Types of Workers

| Worker Type | Enrollment Requirement | Contribution Responsibility |

|---|---|---|

| Full-Time Employee | Mandatory enrollment within 60 days of employment. | Both employer (5%) and employee (5%) contribute. |

| Part-Time Employee | Mandatory if employed for 60 continuous days or more. | Both employer and employee contribute, same as full-time. |

| Casual Employee | Mandatory from the first day of employment (often via Industry Schemes). | Primarily employer contribution, sometimes with employee portion. |

| Self-Employed Person | Must self-enrol within 60 days of starting their business. | Solely responsible for their own contributions. |

| Exempt Expat | Not required if part of an overseas scheme or in HK for < 13 months. | No MPF contribution required from either party. |

As you can see, your role shifts dramatically depending on the nature of the employment relationship. Always be clear about the terms of engagement to ensure you’re meeting the correct obligations from day one.

Exemptions for Expats and Rules for Departing Employees

What about talent from overseas? Hong Kong is a global business hub, so it's common for SMEs to hire expatriates. An employee holding an employment visa might be exempt from the MPF system, but only if they meet specific conditions, like:

- They are already a member of a retirement scheme in their home country.

- They have permission to stay in Hong Kong for 13 months or less.

Watch out for changes in their status. If an expat’s visa gets extended beyond 13 months, they lose their exemption. At that point, you have 60 days to get them enrolled in your MPF scheme.

And finally, what's your role when an employee—local or expat—leaves Hong Kong for good? They have the right to withdraw their accumulated MPF benefits early.

Your responsibility is to make their final contribution payment accurately and on time. After that, it’s between the employee and their MPF trustee. They’ll need to provide proof of their permanent departure (like a visa for their new home country) and sign a statutory declaration. Once you've made that last payment, your part is done.

Using MPF for Tax Deductions and Financial Strategy

For many business owners in Hong Kong, the monthly MPF contribution feels like just another box to tick—a mandatory cost of doing business that shows up on every payroll report. But if that’s all you see it as, you're missing a trick.

Viewing your MPF obligations as purely a compliance task is a missed opportunity. Smart entrepreneurs know how to frame this cost as a strategic financial tool, one that can directly benefit the company's bottom line while also making your compensation packages more attractive. It all starts with a simple shift in perspective.

The Power of Tax Deductibility

Here's the key: every single dollar you contribute to your employees' MPF accounts on a mandatory basis is fully tax-deductible. This isn't just some minor perk; it's a direct reduction of your company's profits tax liability.

Think of it this way: the government is essentially giving you a tax break for helping build your team's retirement security.

Let's say your company's total mandatory employer MPF contributions for the year come to HK$120,000. When it’s time to file your profits tax return, you can claim that entire amount as a legitimate business expense. This immediately reduces your taxable profit by HK$120,000, which translates into real, tangible savings for your business.

The government has put a cap on this deduction at 15% of an employee's total annual income, but this is a generous ceiling that covers almost every standard mandatory payment scenario. It cleverly transforms a compliance headache into a smart financial move.

Going Beyond the Mandatory Minimum

The 5% mandatory contribution is just the starting point. The MPF system is actually designed with flexibility in mind, offering powerful ways to do more for your team—and for yourself as a business owner. This is where Voluntary Contributions (VCs) enter the picture.

There are two main types of voluntary contributions you should know about:

- Standard Voluntary Contributions (VCs): Both you and your employees can decide to contribute more than the required 5%. As an employer, offering to make extra VCs can be a fantastic way to sweeten a compensation package, helping you attract and hold on to top talent in a very competitive market.

- Tax Deductible Voluntary Contributions (TVCs): This is more of a personal savings tool that your employees—and you, as an individual—can use to top up retirement funds while simultaneously lowering personal tax bills. Anyone can open a separate TVC account and contribute up to HK$60,000 a year, then claim that full amount as a deduction on their personal tax return.

While you don't manage your employees' personal TVC accounts, simply educating them about this option is a valuable, no-cost benefit you can offer. It demonstrates that you're invested in their overall financial well-being, not just ticking regulatory boxes.

Building a Strategic Benefits Package

When you combine mandatory contributions with voluntary options, your approach to the mpf hk contribution evolves. It stops being a simple obligation and becomes a cornerstone of your company's financial and HR strategy. The conversation shifts from monthly deductions to long-term wealth creation for your team.

For instance, you could roll out a loyalty programme where the company makes an additional 2% voluntary contribution for any employee who stays with you for over three years. This not only rewards commitment but is also a tax-deductible expense for the business.

Ultimately, by getting to grips with the tax benefits and exploring the voluntary contribution landscape, you can transform the MPF from a cost centre into a strategic asset. It becomes a powerful tool to lower your tax burden, attract and keep great people, and build a more financially secure future for everyone involved.

Integrating MPF into Your SME Payroll System

Knowing the rules is one thing, but actually building a reliable payroll workflow is where the pressure hits for many small business owners. Setting up a seamless process for your mpf hk contribution isn't just about ticking a compliance box. It’s about creating an efficient, almost automatic system that runs smoothly in the background, freeing you up to focus on what really matters: growing your business.

Think of it as setting up a financial assembly line. Once you get it right, it just works, month after month, without any drama. This checklist is your blueprint for making MPF management a simple, repeatable part of your operations.

Your Step-by-Step Integration Checklist

A solid MPF workflow comes down to a few key one-time decisions and a disciplined monthly routine. Here’s how you can break it down into manageable steps.

Phase 1: Initial Setup

- Choose the Right MPF Trustee: This is your first big decision. Don't just pick the first one you see. Compare trustees based on their fund performance, management fees, and, importantly, the quality of their employer portal. A clunky, outdated system will cause you headaches down the road; a user-friendly one will save you hours.

- Set Up Your Employer Account: After you've picked a trustee, you need to get your business officially registered with them. This usually involves submitting your Business Registration Certificate and filling out their participation forms to get your company’s MPF account up and running.

Phase 2: Monthly Process

3. Establish a Calculation & Payment Routine: Your monthly payroll run needs a dedicated step just for MPF. If you can, use payroll software to automate the calculations—it’s much better at remembering the latest income thresholds and contribution caps than we are. Set a non-negotiable reminder in your calendar to get the payment sent off before the 10th of each month.

4. Create a Solid Record-Keeping System: Hong Kong law requires you to keep MPF records, like remittance statements, for at least seven years. The easiest way to handle this is to set up a digital folder for each financial year. It keeps things organised, easy to find, and ready in case of an audit.

Best Practices for Employee Communication

Don't forget the human side of things. Clear communication with your team about their MPF builds trust and shows you're invested in their future.

One of the biggest sources of employee confusion comes from the payslip. Make sure it clearly breaks down the employee's contribution, the employer's contribution, and the total amount going to their MPF account. This little bit of transparency goes a long way in preventing questions and reassuring your staff that everything is being handled correctly.

For many SMEs, the real challenge is getting payroll and accounting to talk to each other seamlessly. To take the headache out of these administrative tasks, many business owners turn to outsourced bookkeeping solutions, which can handle everything from payroll to MPF management.

If you'd rather keep things in-house but need a hand designing a compliant and efficient system, our team is ready to help make this part of your business run like clockwork.

Common Questions About MPF Contributions

Diving into the world of MPF contributions can feel like you're trying to solve a puzzle, especially when you’re already juggling the demands of running a business. Let’s walk through some of the most frequent questions we hear from fellow entrepreneurs, with clear answers to keep you on the right track.

What Happens If I Miss an MPF Contribution Deadline?

The MPFA is very strict about deadlines, and missing the 10th of the month cut-off has immediate consequences. If you’re late, a payment notice will be issued automatically, demanding not just the overdue contribution but also a 5% surcharge.

This isn't a government fine, either. That surcharge goes directly into your employee's MPF account to make up for the investment growth they missed out on. Let these notices pile up, and you could be looking at steeper financial penalties and even legal trouble. The simplest way to avoid this headache is to stick to a consistent, reliable payroll schedule.

Can an Employee Opt Out of the MPF Scheme?

For almost everyone on your team, the answer is a clear no. MPF participation is mandatory for any employee in Hong Kong between the ages of 18 and 64 who has worked for you for 60 days or more. This rule covers both your full-time and part-time staff.

The exceptions to this rule are few and far between. They're typically reserved for specific cases, like expatriates who are part of an approved overseas retirement plan or domestic helpers. So, for the vast majority of your workforce, opting out simply isn't an option.

Do I Make MPF Contributions During Probation?

Yes, you absolutely do. This is a classic trip-up for new employers. Your legal duty to make MPF contributions begins the moment an employee starts working for you—probation period included.

You have a 60-day window to get a new hire formally enrolled in your company's MPF scheme, but don't mistake this for a payment holiday. It's just an administrative grace period. You are still responsible for contributions from day one, and you'll need to make back-payments for this initial period once they're enrolled.

It’s best to think of it this way: the 60-day rule is for handling the paperwork, but the contribution clock starts ticking from their very first day on the job.

Conclusion

Figuring out the ins and outs of MPF, tax structures, and international banking is what we live and breathe. At Lion Business Consultancy Limited, we step in as your private financial manager, making sure your business is compliant, secure, and set up for long-term growth. Let us manage the fine print so you can focus on the big picture. Learn how our private advisory can secure your business's future.