Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

Picture this: you have a business bank account that's been put on lockdown by your bank simply because no one has touched it for a while. It’s a security measure, sure, designed to protect your money from fraud. But for a busy entrepreneur, it's a major headache. Suddenly, all your transactions are frozen solid until you step in and prove you’re still around.

This isn't just a minor inconvenience; it's a full-stop on your cash flow for that account. Let's break down what this really means for your business.

Unpacking What a "Dormant Account" Really Means

Let’s tell a quick story. You opened a business bank account for a new project, but then a bigger, more urgent opportunity came along and things got sidetracked. Two years fly by, and that account has been sitting there, gathering digital dust. When you finally go to use it, you discover it’s completely frozen. That, in a nutshell, is a dormant account.

For a small or medium-sized enterprise (SME) in Hong Kong, this isn't just an "old" or "unused" account. It's a specific security status triggered by a prolonged period of inactivity from your end.

Think of it as a safety lock on a valuable asset. If your office building stood dark and empty for over a year, you’d want someone to secure the doors, right? Banks apply the same logic to your money. When they see no deposits, withdrawals, or transfers for a certain period—usually between 12 to 24 months—they flag the account to shield it from potential thieves who might target forgotten funds.

The Bank's Protective Role

This isn't your bank trying to punish you. It’s a proactive measure to protect your business. By freezing the account, they're erecting a barrier against security threats that often prey on neglected funds. This is a standard and necessary part of their risk management playbook.

In Hong Kong, financial institutions manage a huge number of these accounts. Local regulations require them to monitor dormant funds closely to reduce fraud and handle unclaimed money responsibly. The Hong Kong Monetary Authority (HKMA) provides clear guidelines on how these situations should be managed. You can dive deeper into these banking rules on the official HKMA website, which details how Authorised Institutions are expected to handle such accounts.

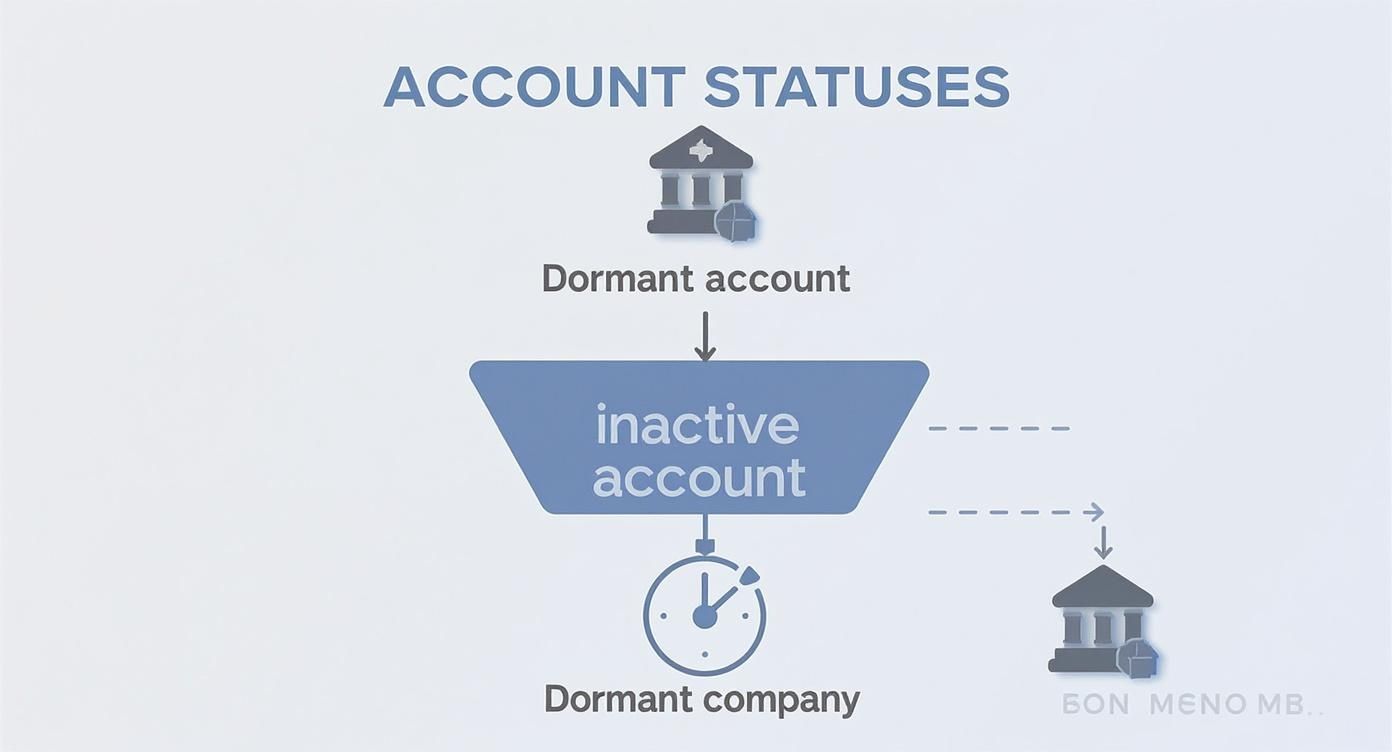

As the infographic highlights, a "dormant account" is a specific banking term. It’s a step beyond a simple "inactive account" and is worlds apart from a "dormant company," which is a formal legal status for your business. Nailing this distinction is absolutely critical for any business owner.

Dormant Account vs Inactive Account vs Dormant Company

It's easy to blur the lines between these terms, but they represent very different realities. Here’s a quick breakdown to keep them straight, particularly within the Hong Kong business landscape.

| Term | What It Means | Primary Context | Key Action Required |

|---|---|---|---|

| Dormant Account | A bank account frozen by the bank after a long period (e.g., 24+ months) of no customer-initiated transactions. | Banking & Finance | Contact the bank to verify your identity and reactivate the account. |

| Inactive Account | A bank account with no transactions for a shorter period (e.g., 6-12 months). It's a warning stage before dormancy. | Banking & Finance | Make a simple transaction (deposit, withdrawal) to keep it active. |

| Dormant Company | A legal status for a registered company that has no significant accounting transactions during a financial year. | Corporate & Legal | File a special resolution with the Companies Registry; annual filings are still required. |

Understanding these differences is key. A dormant company is a deliberate strategic choice you make, while a dormant account is usually an accidental oversight with immediate financial consequences.

Why This Matters for Your SME

For an entrepreneur, the fallout from a dormant account can be surprisingly disruptive. A frozen account can silently derail your operations by blocking automatic payments, stopping incoming revenue in its tracks, or creating a tangled mess for your financial reporting.

A dormant account isn’t a sign that your business is failing; it’s just an administrative slip-up. But the consequences can feel just as severe if you don’t stay on top of it. It’s a quiet risk that can pop up at the worst possible moment.

Getting your head around the dormant account meaning is the first step. The real work is putting systems in place to avoid it. This guide will walk you through exactly why accounts go dormant, the risks involved, and the practical steps to either bring a frozen account back to life or—even better—prevent it from happening in the first place.

Common Reasons Business Accounts Go Dormant

An account doesn't just fall asleep overnight. It's more of a slow drift, often triggered by completely normal business situations. It’s one thing to know the textbook definition, but it's another to see just how easily an active account can end up on that list. For most business owners, it boils down to a simple case of "out of sight, out of mind."

Think of a business bank account like a specialized tool you buy for a single, important job. Once that job is done, the tool goes back into the shed, and eventually, you forget it’s even there. The same thing happens with accounts set up for a specific purpose. Once that purpose fades, the account slips into the background.

Forgotten Project-Specific Accounts

One of the most common culprits we see is the project-specific account. Let's say your creative agency in Hong Kong lands a one-off government grant for a digital arts festival. To keep the books clean and transparent, you wisely open a new bank account just to handle those funds.

The festival is a massive success. You pay all the suppliers, file your reports, and the team moves on to the next big win. But a small balance, maybe just a few hundred dollars, gets left behind in the festival account. Life gets busy. That account is never touched again. Fast forward two years, and you get a notice that it's been frozen.

Ventures That Never Took Off

Another classic scenario is the account opened for an idea that never quite got off the ground. Entrepreneurs are famous for juggling multiple concepts, and sometimes an idea progresses just far enough to need a bank account before it gets put on hold indefinitely.

Imagine a tech founder in Kowloon with a brilliant app concept. They incorporate a company and open a business account to look credible for early investor meetings. But then, a more promising opportunity pops up. The app project is shelved, and the associated bank account is completely forgotten. It just sits there, empty and unused—a financial ghost of what could have been, slowly drifting towards dormancy.

A dormant account often starts with good intentions—a special project, a new venture, or a temporary need. The problem isn't the setup; it's the lack of a clear 'off-boarding' process for financial tools you no longer need.

Administrative Oversights and Staff Changes

Sometimes, dormancy is simply a result of human error, particularly when a company is going through changes. If a key finance person leaves and the handover isn't perfect, knowledge of certain bank accounts can walk right out the door with them.

It happens more often than you'd think:

- Lost in the Handover: A departing financial controller forgets to list a minor, rarely used account in their handover notes for the new hire.

- Decentralized Management: Different departments have the power to open their own accounts, meaning no single person has a complete view of the company's banking footprint.

- Outdated Contact Information: The bank sends dormancy warnings, but they go to an old office address or a former employee's email. You never even see the alerts.

These small administrative gaps are all it takes for an account to slip through the cracks. Without a central, constantly updated list of all company bank accounts, it's dangerously easy for one or two to become inactive and eventually get flagged. Here, dormancy isn't just a banking issue; it's a clear signal of a weakness in your internal financial controls.

The Real Risks of a Dormant Business Account

When a business account is flagged as dormant, it's not just a minor inconvenience. It triggers a cascade of problems that can freeze your operations, eat into your funds, and create a mountain of administrative work. For any business owner in Hong Kong, understanding what happens next is essential.

The first and most immediate consequence is that the bank will freeze the account. Think of it as putting the account into a financial quarantine. All transactions—both incoming and outgoing—are blocked. This isn't a temporary hold; it's a hard stop.

This freeze can throw a wrench into your day-to-day operations almost instantly. Automated payments for software, rent, or supplier invoices will start failing. Any money your clients try to send will bounce back, which can strain relationships and choke your cash flow. All of a sudden, that forgotten account has become a very real, very urgent problem.

The Financial Drain of Dormancy Fees

Once an account is frozen, the financial damage usually begins. Many banks start levying dormancy fees or inactive account management fees. These charges might seem small month-to-month, but they quietly add up, steadily chipping away at whatever balance was left behind.

If there's only a small amount of money left, these fees can eventually drain it completely. It’s a slow bleed that punishes inaction, turning what was once a company asset into a liability before you even realize it.

A dormant account is like a boat with a slow, silent leak. At first, you don't notice it, but given enough time, the vessel that was meant to carry you forward is now underwater—and you’re left with the salvage operation.

This slow drain is precisely why it’s so important to understand the dormant account meaning not just as a label, but as an active financial risk.

The Point of No Return: Unclaimed Property

If an account is left dormant for an extended period—we're talking several years—a much more serious process kicks in. Following guidelines from regulators like the Hong Kong Monetary Authority (HKMA), the bank may reclassify the money as unclaimed property.

At this point, the bank is legally required to hand the funds over to a government body. This process, known as escheatment, means the money is no longer held by your bank at all. While you can technically still reclaim it, the journey becomes far more bureaucratic and complicated. Instead of dealing with your familiar bank branch, you'll be navigating government procedures.

- Initial Freeze: All transactions are blocked instantly.

- Fee Accumulation: Monthly fees start to eat away at the balance.

- Escheatment: After several years, the funds are transferred to a government agency as unclaimed property.

Trying to reclaim your funds from the government is a long and frustrating ordeal that requires stacks of paperwork and a great deal of patience to prove ownership.

The Security and Compliance Hurdle

While freezing an account is done to protect your funds, reactivating it brings its own hurdles. Banks are held to very strict Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations.

You can't just call up and ask them to unfreeze the account. You'll have to prove who you are and that your business is legitimate all over again. This typically involves:

- In-Person Verification: Showing up at a branch with your original ID documents.

- Updated Business Records: Providing a current Business Registration Certificate and other up-to-date corporate documents.

- Source of Funds Scrutiny: Answering detailed questions about your business activities and explaining why the account fell into disuse.

This entire process is designed to stop financial crime, but for a legitimate business owner, it’s a time-consuming and frustrating task. The lesson is clear: proactive account management isn’t just good financial hygiene—it’s a vital strategy for keeping your company stable and secure.

Understanding Dormant Company Status in Hong Kong

It’s a common mistake to hear "dormant account" and "dormant company" and think they're one and the same. But for any business owner in Hong Kong, this is a crucial distinction. Mixing them up can lead to missed opportunities or, worse, surprise compliance headaches.

The truth is, they represent two completely different scenarios. One is a reactive banking issue, while the other is a proactive legal strategy you can choose to implement.

A dormant bank account, as we've covered, is a label your bank applies after a long period of inactivity. It's an operational hiccup you need to fix. A dormant company, however, is an official status you choose for your registered business. Think of it as putting your entire company into a planned, legal hibernation.

A Strategic Pause, Not an Accidental Freeze

So, why would you want to do this? You might decide to make your company dormant if a venture is temporarily on hold, if you want to reserve a company name for a future project, or perhaps during a significant restructuring. It's a deliberate business move, not a clerical error.

This status is fantastic for reducing the administrative load and costs that come with running an active company.

The core difference really boils down to control. A dormant account is something that happens to you, often without you noticing until it's too late. Declaring a company dormant is a step you take, giving you a strategic edge when your business doesn't need to be fully operational.

The Legal Framework in Hong Kong

Under Hong Kong’s Companies Ordinance, a private company can formally declare itself dormant so long as it has had no "significant accounting transactions" during a financial year. To get the ball rolling, the company’s members need to pass a special resolution and file the necessary paperwork with the Companies Registry. This official step effectively pauses many of your usual corporate obligations.

Declaring a company dormant is like taking your car off the road and filing a Statutory Off Road Notification (SORN) in the UK. You can't legally drive it, but you're also relieved of the costs of tax and insurance until you're ready to get back behind the wheel. It’s a recognised, legal way to pause operations.

This strategic move brings some pretty significant benefits for a non-trading company. You gain exemptions from:

- Holding annual general meetings (AGMs)

- Appointing auditors

- Preparing and filing audited financial statements

These exemptions alone can save a business thousands of dollars in professional fees and cut down on countless hours of admin. But it's not a complete shutdown. You're still required to maintain a registered office and file an Annual Return, which includes key details like your business registration number.

For businesses navigating this process, professional company secretarial services can be a lifesaver, ensuring all the right boxes are ticked even while the company is inactive. It's vital to remember that while many duties are paused, the company still legally exists and must meet certain core statutory requirements. Getting this wrong can lead to penalties, proving that even a hibernating company needs a watchful eye.

How to Reactivate Your Dormant Business Account

It’s a heart-stopping moment for any entrepreneur: discovering a key business account has been frozen. You feel like you've hit a financial brick wall. But here's the good news—reactivating a dormant account isn't some impossible puzzle. It's a well-trodden path, and it’s all about following the bank's playbook.

For business owners in Hong Kong, the journey back to an active account is straightforward, though it demands careful attention to detail. It's less of a battle and more of a formal re-introduction. You’re simply showing the bank your business is still active, legitimate, and ready to get back to work. Let’s walk through the steps to get your funds flowing again.

Step 1: Get in Touch with Your Bank

Everything starts with a single, crucial action: contacting your bank. Don't put this off. A quick call to your relationship manager or the bank’s business banking hotline is usually the best place to start.

When you call, have your company name, account number, and your own details as an authorised signatory ready to go. The goal of this first chat is simple: confirm the account is dormant and get their specific checklist for reactivation. Every bank has its own slightly different process, so understanding their requirements is your top priority.

This initial call sets the stage for everything that follows and shows the bank you're tackling the issue head-on.

Step 2: Round Up Your Documents

After that first call, the bank will send over a list of documents they need. This is where being organised really pays off. Hong Kong’s strict regulations mean you'll have to provide up-to-date corporate paperwork to re-verify your business's identity.

This isn’t optional; it’s about satisfying the bank’s Know Your Customer (KYC) obligations. While the exact list can differ slightly between banks, you should be ready to pull together the following:

- Updated Business Registration Certificate: Your latest, valid certificate from the Inland Revenue Department.

- ID for All Directors/Signatories: Passports or Hong Kong Identity Cards (HKIDs) for every single person authorised to use the account.

- Proof of Business Address: A recent utility bill or bank statement (from the last three months) that shows the company’s registered address.

- Company Chop: Your official company seal will almost certainly be needed to stamp forms.

Having these items ready will make the next stage go much more smoothly. If you want a refresher on what's typically required, our guide on the process of opening a corporate bank account in Hong Kong gives a detailed breakdown that's just as useful for reactivation.

Step 3: Plan for an In-Person Visit

Because of Hong Kong’s tough Anti-Money Laundering (AML) regulations, you can bet the bank will require an in-person visit from the account signatories. This isn't just a formality; it's a critical step to verify who you are.

The bank needs to physically see the authorised people and check their original ID documents to prevent any chance of fraud. During the appointment, you'll hand over the documents you’ve gathered and probably fill out a specific reactivation form.

Think of the in-person visit as a "financial handshake." It re-establishes trust between you and your bank, confirming the real owners are back in charge and ready to resume business.

Step 4: Make a Transaction to Seal the Deal

The final step is usually the easiest one: just make a transaction. Once the bank has processed your paperwork and confirmed your identity, they’ll typically ask you to perform a small, simple action to officially "wake up" the account.

This could be something as straightforward as:

- A small cash deposit at the counter.

- A minor withdrawal.

- A transfer to another account.

This one action is the last piece of the puzzle. It signals to the bank's systems that the account is no longer dormant and is back under your control. And just like that, your account is live again, and your business can get back to what it does best.

Keeping Your Business Accounts Active and Secure

The easiest way to deal with a dormant account is to make sure it never becomes one. Think of it like regular maintenance on a critical piece of machinery—a little bit of attention now saves you from a massive, expensive breakdown later. For busy SMEs, this isn't about adding another complicated task to your plate. It's about building simple, effective financial habits.

Good financial hygiene is your best defence. It's a strategy built on awareness and consistency, designed to keep your business agile and protect your assets from being frozen or chipped away by fees. A few straightforward practices can save you an incredible amount of time and keep your operations running smoothly.

Building Your Proactive Management Checklist

The secret is routine. Instead of waiting for a problem to pop up, you can set up a simple framework to keep all your accounts healthy and active. This doesn't need to be complex; it just needs to be consistent.

Here are a few practical habits to get into:

- Conduct Semi-Annual Account Audits: Twice a year, block out some time to review every single bank account your business holds. Look at the transaction history, check the balance, and ask yourself, "What is this account for?" If you find one you no longer need, start the official process to close it.

- Consolidate and Simplify: Does your business really need seven different bank accounts? It's common for SMEs to open new accounts for specific projects and then forget about them. By consolidating funds into fewer, more active accounts, you reduce the clutter and lower the risk of one slipping through the cracks.

- Set Up Small, Automated Transfers: This is a lifesaver for accounts you need to keep open but don't use often. A tiny, recurring transfer—even just a few dollars—between your own accounts is enough to count as customer-initiated activity. It effectively resets the dormancy clock.

Maintaining Control and Compliance

Beyond just making transactions, keeping clear records and an open line of communication with your bank is vital. An organised approach gives you a complete picture of your financial footprint and ensures your bank can always reach you with important notices.

Financial security isn't just about strong passwords; it's about strong processes. Keeping a detailed and updated account register is one of the most powerful yet simple tools an entrepreneur can have to prevent financial oversight.

Maintain a central list of all company bank accounts. Note down the bank, account number, its purpose, and who is authorised to sign on it. Most importantly, always keep your contact details—your business address, email, and phone number—up to date with every single bank. This simple step ensures you'll get any warning letters before an account is flagged as dormant.

Proper record-keeping is more than just good housekeeping; it's a cornerstone of good governance and a key part of maintaining compliance with a Hong Kong bank account, which ultimately protects your business for the long haul.

Your Questions, Answered

When you're running a business, the last thing you want is a surprise from your bank. Let's walk through some of the most common questions we hear from business owners in Hong Kong about dormant accounts, with some straightforward answers.

How Long Before My Business Account is Considered Dormant?

There isn't one single answer that applies to every bank, but the typical window in Hong Kong is between 12 to 24 months. The key here is "customer-initiated activity"—we're talking about deposits, withdrawals, or transfers that you or someone authorised on the account makes.

Don't be fooled by automated transactions. Things like the bank crediting interest or deducting service fees do not count as you using the account. The best advice? Dig into the terms and conditions of your specific bank to know their exact timeline.

Will the Bank Let Me Know Before an Account Goes Dormant?

They're supposed to. Hong Kong banks are generally required to make a good faith effort to reach you, which usually means sending a letter to the address they have on file.

The problem is, this system only works if your contact details are up to date. If your company has moved offices and you forgot to tell the bank, that crucial notification will never reach you. It's a simple but powerful reason to make sure your bank always has your current information.

Can a Dormant Account Hurt My Company's Credit Score?

Directly? No. A dormant account is a classification used by your bank; it isn't something that gets reported to credit agencies and won't impact your company's legal standing in Hong Kong.

But the indirect risks are very real. Imagine you have automatic payments set up for essential suppliers, loan repayments, or government taxes. Once the account is frozen, those payments will fail. That's what leads to the real damage: late fees, defaults, and a hit to your business's financial reputation.

Does It Cost Money to Reactivate a Dormant Account?

You probably won't see a line item called a "reactivation fee" on your statement. But that doesn't mean you're in the clear. Many banks charge ongoing "dormancy fees" or "inactive account management" fees for every month the account has been sitting idle.

These charges are usually taken right out of the account's balance. When you go to wake the account back up, make sure you ask for a full statement of all accrued fees. It’s better to know what you’re dealing with upfront.

Conclusion

Knowing the dormant account meaning is one thing, but actively managing your international banking is what sets successful businesses apart. At Lion Business Consultancy Limited, we operate as your private financial manager, making sure your accounts are secure, compliant, and structured for growth. Book a private consultation with our experts today to protect your assets and get your business ready for its next big step.