Hong Kong

Hong Kong

Singapore

Singapore

UAE

UAE

Malaysia

Malaysia

Turkey

Turkey

UK

UK

EU

EU

US

US

Switzerland

Switzerland

Bahamas Bank Account

Bahamas Bank Account

Cayman Islands Bank Account

Cayman Islands Bank Account

Mauritius Bank Account

Mauritius Bank Account

BVI

BVI

Seychelles

Seychelles

For entrepreneurs with global ambitions, a Hong Kong bank account isn't just a place to park cash—it’s a key piece of strategic infrastructure. Securing one is a clear signal that you’re serious about international business, giving you a powerful foothold in one of the world's most vibrant commercial hubs.

But let's be honest, the process can feel intimidating. This guide is designed to change that. We'll walk you through the entire journey, cutting through the complexity to give you a clear, step-by-step path to getting it done right.

Your Gateway to Global Commerce in Hong Kong

Think of a Hong Kong bank account as the financial control tower for your international operations. Imagine you run an e-commerce business. You're sourcing products from mainland China, but your customers are scattered across Europe and North America. Your Hong Kong account becomes the central hub where all the financial pieces connect.

It’s where you’ll seamlessly receive payments in multiple currencies, pay your suppliers without friction, and manage your cash flow, all within a banking system that’s trusted worldwide. Hong Kong’s legendary financial stability and its status as a free port make it the logical choice for any business looking to scale globally.

Why Hong Kong Stands Out

The city's financial clout is immense. To put it in perspective, as of Q2 2025, Hong Kong's banking sector held an incredible 53.1% of the region's external debt. That figure alone shows just how central it is to Asia's financial plumbing.

During that same period, Hong Kong posted a balance of payments surplus of US$105.5 billion, a testament to its rock-solid financial position.

So, what does all this mean for your business? It means you're plugging into a system purpose-built for commerce, which comes with some very real advantages:

- Effortless Multi-Currency Management: You can hold and transact in major currencies like USD, EUR, and GBP, dodging the hefty conversion fees you’d get hit with elsewhere.

- Access to Serious Trade Finance: Hong Kong banks are pros at this. They offer sophisticated tools like letters of credit and trade loans—essentials if you’re moving physical goods across borders.

- Instant Credibility: Having an account with a major Hong Kong bank tells partners and customers that your business is legitimate and established. It builds trust instantly.

"Think of your Hong Kong account as more than just a place to hold money. It's a strategic asset that signals your business is serious about global trade and is positioned for growth."

Ultimately, the goal is to find a reliable banking partner who understands and supports your vision. While getting set up requires careful preparation, the payoff is huge. You can read more about the specific benefits of a Hong Kong bank account for international businesses to see exactly how it could work for you. From navigating compliance to picking the right bank, this guide will give you the practical know-how to succeed.

How to Choose the Right Bank for Your Business

Choosing a bank for your business in Hong Kong isn't about picking the biggest name. It's about finding a genuine financial partner whose strengths actually match what your company does day-to-day. You wouldn't buy a sports car to haul construction materials, right? The same logic applies here.

A global trading company moving goods across continents needs the banking equivalent of a heavy-duty lorry. This points towards established players like HSBC, Standard Chartered, or Bank of China. They bring robust trade finance tools, deep multi-currency capabilities, and a vast international network to the table.

On the other hand, a local digital marketing agency might find a nimble city car a much better fit. A smaller regional bank or a modern digital bank could offer lower fees, a slick online platform, and more personal, accessible service for everyday transactions. The right choice is all about your business model.

Analysing the Banking Giants

Hong Kong’s banking world is dominated by a few major players. This isn't an exaggeration—as of 2021, the three largest banks held about 62.47% of the entire sector's assets. This concentration means the big international names are often the default choice for businesses looking to open a bank account in Hong Kong.

Their global reach is a huge advantage, especially for companies with complex international supply chains or customers scattered around the world. An established name also gives your business an immediate injection of credibility. But that scale can have its downsides, like higher fees, tougher compliance hurdles, and a customer service experience that feels a bit impersonal.

Key Factors to Consider in Your Decision

To make the right call, you have to look past the brand and dig into the practical features that will affect your daily operations. A systematic approach is your best friend here.

Here are the core things to weigh up:

- Relationship Management: Will you get a dedicated relationship manager who actually understands your business? Or will you be stuck navigating a call centre? A good manager is worth their weight in gold for complex needs like trade finance or future funding.

- Online Banking Platform: Is the digital interface intuitive and powerful? Check if it can handle bulk payments, international transfers, and user permissions without causing a headache. A clunky online system can drain hours from your week.

- International Transfer Costs: Look closely at the fees for telegraphic transfers (TT). Banks can have wildly different charges for sending and receiving foreign currencies, and these costs pile up fast if you're an international business.

- Account Maintenance Fees: Does the bank demand a high minimum balance just to waive its monthly fees? For a start-up, having capital tied up to avoid charges is a serious drag on cash flow.

When you choose a bank, you're not just opening an account; you're entering a long-term relationship. Ensure their services, fee structure, and support model are built to help your business grow, not hold it back.

For businesses with significant assets or complex wealth management needs, it’s also worth exploring specialised private banking solutions. These offer a much higher tier of personalised service and investment opportunities.

Comparing Traditional Banks vs Digital Alternatives

The rise of virtual banks and Electronic Money Institutions (EMIs) has given entrepreneurs some exciting new options. These digital-first platforms often provide a faster, more straightforward onboarding experience and much lower fees. They're fantastic for handling simple, multi-currency transactions through slick mobile apps.

Before making a final decision, it helps to see a side-by-side comparison of what each type of institution offers.

Comparing Traditional Banks vs Digital Alternatives

| Feature | Traditional Hong Kong Banks | Digital Banks & EMIs |

|---|---|---|

| Onboarding | In-person meetings often required, extensive paperwork, can take weeks. | Fully online, faster verification, often opened within days. |

| Fees | Higher monthly maintenance, international transfer, and FX fees. | Low or no monthly fees, very competitive transfer and FX rates. |

| Services | Full suite: trade finance, loans, mortgages, wealth management, credit. | Primarily focused on payments, multi-currency accounts, and cards. |

| Support | Dedicated relationship managers (for larger clients), branch access. | Primarily digital support via chat, email, or app; less personal. |

| Credibility | High-level of trust and recognition, established for decades. | Newer to the market, credibility is growing but not yet at the same level. |

| Best For | Established businesses with complex trade, credit, or advisory needs. | Start-ups, freelancers, e-commerce, and SMEs needing fast, low-cost transactions. |

Ultimately, many businesses find that a hybrid approach works best. You might use a major bank for core trade finance and credit facilities, while leveraging a digital account for its speed and cost-effectiveness in everyday transactions. We cover this strategy in more detail in our guide on choosing the right Hong Kong bank for your business needs.

Your Essential Document Checklist for Account Opening

Opening a corporate bank account in Hong Kong isn't just about filling out a few forms. Think of it more like building a case for your business. The bank’s compliance team isn't simply ticking boxes; they have a legal duty to understand precisely who you are, what your business does, and where your money is coming from. This is their first line of defence against financial crime, and your job is to give them a clear, compelling story that makes saying "yes" an easy decision.

Imagine a French entrepreneur, Sophie. She's launching a sustainable fashion brand and has set up a Hong Kong company to manage her sourcing from Vietnam and sales across Europe. To open her bank account in Hong Kong, she can't just walk in with her passport. She needs to present a complete, coherent file that’s backed up by official documents.

Let’s break down exactly what she—and you—will need to assemble. Each document answers a specific question for the bank's Know Your Customer (KYC) and Anti-Money Laundering (AML) teams.

Core Corporate Documents: Proving Your Company Is Real

First things first, you have to prove your company legally exists and is in good standing. This is the absolute foundation of your application. The bank needs official confirmation that your business is a legitimate entity, properly registered with the Hong Kong government.

These are the non-negotiables:

- Certificate of Incorporation (CI): This is your company's birth certificate. It’s the official document proving the company was legally formed under Hong Kong's Companies Ordinance.

- Business Registration Certificate (BRC): Issued by the Inland Revenue Department, this shows your company is registered to do business and pay taxes. Make sure it's current and valid.

- Articles of Association (A&A): This is the company’s internal rulebook. It lays out how the business is run, the powers of the directors, and the rights of shareholders.

Without these three documents, the conversation is over before it even starts. They are the bedrock of your corporate identity.

Documents for Directors and Shareholders: The People Behind the Paperwork

Next, the bank needs to know who is really running the show. They are required to identify every single person with significant control over the company. This includes every director, any major shareholder (the typical threshold is 10% ownership), and the ultimate beneficial owners (UBOs). Transparency is everything here.

For each of these key individuals, you’ll need to provide:

- Valid Passport or HKID: A crystal-clear, certified copy. Don't submit a blurry photo.

- Proof of Residential Address: This must be a recent document, usually from the last three months, like a utility bill or bank statement. It has to show their name and home address, not a business or PO box address.

The bank’s goal is to pierce the corporate veil and see the real people behind the business. Anonymous or hard-to-trace ownership is the biggest red flag in banking compliance today.

This is a common stumbling block. A director who provides an old phone bill or an address that doesn’t match their other ID documents can grind the whole process to a halt. Consistency across all your paperwork is absolutely crucial for a smooth approval.

Business Substance Documents: Showing You're a Genuine Operation

Finally, and this is arguably the most critical part, you have to prove your business is a real commercial enterprise—not just a paper company. This is where you bring your business to life and demonstrate that your future transactions will be legitimate.

This is what you'll need to show them:

- A Detailed Business Plan: It needs to clearly explain your business model, who your customers are, where you source your products, and your financial projections. For Sophie, this means naming her key suppliers in Vietnam and her target retailers in France. Be specific.

- Proof of Business: Show, don't just tell. This could be signed contracts with suppliers, invoices sent to your first few customers, or even a professionally built website and marketing materials. You need to provide tangible evidence of real business activity.

- Source of Funds Declaration: A straightforward statement explaining where the initial investment capital for the business came from.

This is your chance to paint a picture of a credible, low-risk client. A vague business plan or a lack of operational proof sends a clear signal to the bank that you might be high-risk, and that often leads to a swift rejection. By preparing these documents thoroughly, you're not just checking a box—you're building trust with your new financial partner from day one.

Navigating the Bank Onboarding Process

Submitting your application is really just the first step. For many business owners, especially those outside Hong Kong, the bank onboarding process can feel like a complete black box—a string of mysterious steps with no clear end in sight. Knowing what's coming is the key to managing your own expectations and setting yourself up for a win.

The journey looks very different depending on who you are. A local Hong Kong resident director will almost always find the path much smoother. For a foreign entrepreneur, however, the bank's due diligence digs a whole lot deeper. Don't take it personally; it’s a direct result of global anti-money laundering (AML) rules that force banks to be absolutely certain about who they're getting into business with.

The Resident vs. Non-Resident Experience

For a local director, the bank can quickly verify identity and address using established Hong Kong systems. They are a known entity. But for a non-resident, the bank is essentially building a profile of you and your business from the ground up, which means more scrutiny and a longer list of requirements.

Here’s what a foreign entrepreneur should realistically expect:

- The In-Person Interview is (Usually) Non-Negotiable: Most major banks will insist that at least one director flies to Hong Kong for a face-to-face meeting. This is a make-or-break moment where the relationship manager sizes up the credibility of both your business and you.

- A Deeper Dive into Your Background: The bank will want to know more about your business history, your professional track record, and where your initial funds are coming from. They're looking for a clear, logical story that connects all the dots.

- Longer Timelines are the Norm: Because of all these extra checks, the whole process just takes longer for non-residents. Patience isn't just a virtue here; it's a necessity.

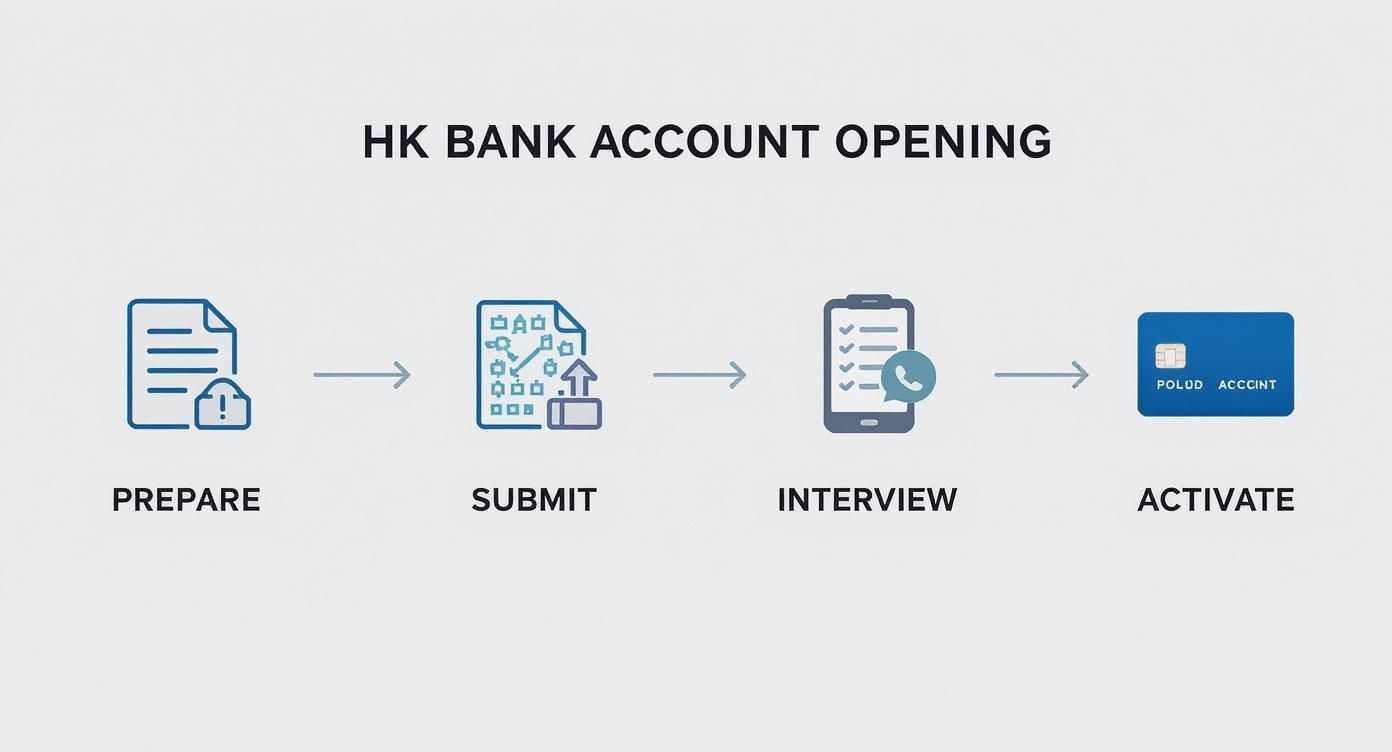

This infographic lays out the typical stages you'll go through when opening your bank account in Hong Kong.

As you can see, the process moves from preparation to the all-important interview and final account activation. But remember, the time spent in each stage can vary wildly.

A Realistic Onboarding Timeline

So, how long does this all actually take? While some of the newer digital banks can be pretty quick, you should realistically set aside anywhere from four weeks to three months for a traditional corporate bank account. In more complex situations, it can easily stretch beyond that. It's a marathon, not a sprint.

Generally, the process unfolds like this:

- Initial Application Review (1–2 weeks): The bank’s front-line team does a basic check to see if your paperwork is complete. If you’ve missed anything, this is where the first delays will hit.

- Compliance and Due Diligence (2–8 weeks): This is the longest and most opaque part of the whole affair. Your file gets passed to the back-office compliance team, who run thorough checks on your company, its directors, and your business model.

- The Interview (Scheduled during the process): The bank will reach out to schedule the in-person meeting. How you perform here—your ability to clearly and confidently explain your business—is absolutely critical.

- Final Approval and Account Activation (1–2 weeks): Once compliance gives the green light, the account is officially approved. You'll then get your account details, security tokens, and online banking login credentials sent out to you.

A vague business description is one of the fastest ways to get your application tossed in the "no" pile. Saying you're in "general trading" is a massive red flag. You need to be specific: "We source artisanal ceramics from Jingdezhen and sell them to boutique home décor stores in the UK."

This whole process might seem a bit intimidating, but just understanding the roadmap is half the battle. Many of the core principles, like proving your identity and the legitimacy of your business, are pretty universal in corporate banking. While we’re focused on Hong Kong here, you'll see similar requirements in guides on how to set up a business bank account in the UK, which just goes to show how global standards shape local banking practices.

Knowing these hurdles are coming and preparing a bulletproof application from day one can dramatically cut down your waiting time and boost your chances of success. To help you get ready for these challenges, our team has put together an in-depth guide. You can find out more by checking out The Bank Onboarding Risk Playbook 2025, which is packed with strategies for navigating compliance and avoiding common pitfalls.

Getting to Grips with Banking Fees and Modern Alternatives

Once your Hong Kong bank account is up and running, it’s a powerful engine for your business. But like any professional service, it comes with costs. Getting a clear handle on these fees is non-negotiable for managing your cash flow and avoiding nasty surprises that can silently chip away at your profits.

Think of it as a subscription for your company's financial backbone—you need to know exactly what you're paying for. Traditional banks in Hong Kong have a fairly standard menu of charges, and while the exact figures differ, you’ll want to budget for a few key ones right from the start.

Breaking Down the Common Bank Fees

The most common costs aren't always printed in bold. You need to dig past the glossy marketing brochures and get into the fine print to see what maintaining the account will really cost you.

- Initial Setup Fee: Most banks will charge a one-off fee to get your corporate account set up. This can be anything from a few hundred to several thousand Hong Kong dollars.

- Minimum Balance Requirement: This is a big one. The major banks often insist you keep a hefty minimum balance—think HKD 50,000 or more—just to avoid a monthly "fall-below" penalty. That's your working capital sitting idle.

- Monthly Service Charges: Even if you maintain the minimum balance, you’ll likely face a standard monthly fee for account maintenance and the services included.

- International Transfer Fees: If you're doing business with overseas clients or suppliers, the cost of telegraphic transfers (TTs) adds up fast. These can be surprisingly high, and you often get hit with fees on both the sending and receiving ends.

"Banking fees aren't just line items on a statement; they reveal a bank's target client. High fees for basic services often signal a focus on large, established corporations. Lower, transaction-based fees are usually a better fit for a lean, modern SME."

The New Players: Digital Banks and EMIs

This traditional fee model has created a huge opening for a new breed of financial technology. Digital banks and Electronic Money Institutions (EMIs) have stepped in as compelling alternatives, especially for startups and small-to-medium-sized businesses. They run on a completely different cost structure, often ditching the hefty maintenance fees for a more flexible, user-friendly experience.

The attraction is clear. These platforms often promise faster, fully remote account opening, slick mobile apps for managing your money, and much cheaper international payments. For a business that just needs to send and receive funds across borders without needing complex trade finance, they can be a perfect match.

The overall banking system in Hong Kong remains incredibly strong, with total deposits jumping by 10.2% over the past year. As the Hong Kong Monetary Authority pointed out, local Hong Kong dollar deposits also grew by a healthy 4.1%, showing just how much confidence people have in the system. This fierce competition between old and new players is great for business owners. You can dive into the full HKMA statistics on deposits to see these trends yourself.

Of course, it’s not a silver bullet. Digital providers don't typically offer the same deep suite of services you'd find at a traditional bank.

Weighing Your Options

Choosing between a household name and a modern fintech doesn't have to be a one-or-the-other decision. In fact, the smartest strategy is often a hybrid one, using the best of both worlds.

- Use a traditional bank for: Core credibility, getting trade finance like letters of credit, securing business loans, and having a human relationship manager to call.

- Use a digital alternative for: Low-cost daily international payments, holding different currencies without high fees, and managing company spending with corporate cards.

By understanding the fee landscape and what each type of provider does best, you can build a banking strategy that’s both cost-effective and perfectly suited to how your business actually operates. This stops you from overpaying for services you don’t need while making sure you have the financial tools to grow.

Common Mistakes That Lead to Account Freezes

Getting your bank account in Hong Kong open is a massive win, but it’s definitely not the end of the road. The real challenge is keeping it healthy and active for the long haul. A sudden account freeze is more than just an inconvenience; it can bring your entire business to a grinding halt, cutting you off from your own money when you need it most.

The best defence is a good offence. You need to understand what makes a bank’s compliance department nervous. Banks are under constant pressure from regulators to fight money laundering and terrorism financing, so their automated monitoring systems are incredibly sensitive. Your goal is to make sure your company's financial activity never gives them a reason to look twice.

Transactions That Raise Red Flags

One of the fastest ways to get on a bank's radar is through financial activity that looks unusual or doesn't have a clear explanation.

Let’s say you told the bank you're running a software consultancy. Then, out of the blue, your account gets a large, six-figure wire transfer from a general trading company based in a high-risk country. To a compliance officer, that just doesn't compute. It’s a complete mismatch with the business profile you provided, and it immediately sets off alarm bells.

The key to staying off their radar is simple: keep your activity consistent and predictable, perfectly matching the business plan you gave them.

Here are a few classic transaction mistakes that trigger alerts:

- Receiving Unexplained Large Payments: A sudden influx of cash that's way outside your normal transaction size or frequency is a huge red flag.

- Transactions with High-Risk Countries: Constantly moving money to or from jurisdictions on international watchlists will guarantee you get extra scrutiny.

- Using Complex Payment Chains: If you're routing money through multiple third-party companies or obscure payment processors for no good reason, it can look like you’re trying to hide where the funds came from or where they're going.

Mismatched Business Activities

Another common trap is letting your business evolve without telling the bank. Maybe you started out selling products online but have since branched into cryptocurrency arbitrage. If the bank is still under the impression you're an e-commerce business, your new transaction patterns will look bizarre and suspicious.

This creates a serious credibility gap. The bank approved your account based on one risk profile, and now they're seeing transactions from an entirely different—and in their eyes, much riskier—industry.

Keeping an open line of communication with your bank isn't just polite; it's a core part of managing your risk. A quick email to your relationship manager about a big upcoming transaction or a shift in your business model can prevent a simple misunderstanding from escalating into a full-blown account freeze.

How to Proactively Protect Your Account

Your best protection is building a strong, transparent relationship with your bank. Don't think of them as an adversary; treat them like a partner who needs to be kept in the loop.

Here are a few practical steps to keep your account safe and sound:

- Keep Your Information Updated: Has your business address changed? New directors on board? Shifted your core services? Tell the bank right away.

- Provide Clear Invoices: Make sure every single payment you receive is backed up by a proper invoice that clearly states what goods or services were sold. This creates a clean paper trail.

- Communicate in Advance: If you're about to receive a significant investment or a large payment for a major project, give your relationship manager a heads-up. Providing context before the money arrives is far better than explaining it after the fact.

At the end of the day, banks freeze accounts because of uncertainty. When they can't understand what you're doing, they assume the worst. By operating transparently and keeping your records immaculate, you remove that uncertainty and prove that you're the kind of low-risk, trustworthy client they want to keep.

Your Top Questions Answered

When it comes to Hong Kong banking, especially for those new to the city, a lot of the same questions pop up. Let's tackle some of the most common ones we hear from entrepreneurs trying to set up their business finances here.

Can I Really Open a Hong Kong Bank Account from Overseas?

This is the big one, and the honest answer is: it's tough, but not completely off the table. A few years ago, it was much more common, but these days, nearly every major bank will insist on at least one director flying in for a face-to-face meeting. It’s a core part of their "Know Your Customer" (KYC) checks.

That said, there are still a few avenues for remote opening. Some private banking divisions or the newer digital banks might be more flexible, but this often comes with a catch—like a much higher initial deposit. Your best shot at a remote opening is working through a trusted local partner, like us at Lion Business Co. We can help package your application so perfectly that the bank feels comfortable, significantly improving your chances.

What’s the Minimum Deposit I Should Expect for a Business Account?

This can be a real point of contrast, and the amount varies wildly depending on where you go.

- The Big Traditional Banks: For institutions like HSBC or Standard Chartered, you're often looking at an initial deposit somewhere between HKD 50,000 and HKD 200,000, sometimes even more. They also usually require you to maintain a hefty balance to avoid getting hit with monthly service fees.

- Digital Banks & Fintechs: This is where things get interesting for startups. Many of the modern alternatives have no minimum deposit at all. For new businesses that need every dollar to be working for them, this is a massive advantage.

How Long Does It Actually Take to Get an Account Open?

Patience is key here. You should budget for anywhere from 4 weeks to 3 months. For more complicated applications, especially with international ownership structures, it can definitely stretch out longer. This timeframe isn't just waiting around; it covers the bank's internal due diligence, deep-dive compliance checks, and finding a slot for the director's interview.

From our experience, the biggest hold-ups almost always boil down to the same three issues: paperwork that's incomplete or has conflicting details, a complex ownership web spanning multiple countries, or providing vague answers that just make the compliance officer ask for more information. If you're a non-resident, expect your application to be on the longer end of that timeline.

Feeling like this is a mountain of paperwork and a maze of rules? You don't have to climb it alone. Think of Lion Business Co. as your private financial manager in Hong Kong. We make sure your application is flawless from the start and connect you with the right bank for your actual business needs. Our job is to get your account open securely and help you avoid the common pitfalls that lead to frustrating freezes.